J&J Hopes for EPS Growth in 2024 to Reverse Losses, Talc Litigation in Focus

December 28, 2023

☀️Trending News

JOHNSON & JOHNSON ($NYSE:JNJ) (JNJ) is one of the most iconic companies in the world. A healthcare giant, JNJ is the largest producer of medical products and services, ranging from baby products to life-saving pharmaceuticals. The company’s stock has been hit hard in recent years, with JNJ’s earnings per share (EPS) falling significantly over the last three years. With this in mind, JNJ is hoping to reverse their losses in 2024, with an increased focus on EPS growth. The talc litigation has been a major factor in the decreased EPS for JNJ. They are currently facing thousands of lawsuits related to the use of talc in their products. These lawsuits have caused JNJ to suffer financial losses and have called into question the safety of their products. As such, JNJ must take action to resolve these legal issues before they can focus on improving their EPS in 2024. Ultimately, the question remains: Will JNJ be able to recover their losses in 2024 through increased EPS, with a focus on talc litigation? With a clear plan of action and an eye towards the future, JNJ could turn things around and become profitable once more.

However, it remains to be seen if their strategies will succeed in reversing their losses and allowing for EPS growth in 2024.

Earnings

JOHNSON & JOHNSON recently reported their FY2023 Q3 earnings as of September 30 2023. Total revenue for the quarter was 21.35B USD, with a net income of 26.03B USD. This marks a 0.0% decrease in total revenue from the previous year, as well as a 0.0% decrease in net income. Over the last 3 years, total revenue for J&J has stayed constant, at 21.35B USD. In light of the recent losses, JOHNSON & JOHNSON is hoping to see an increase in earnings per share (EPS) by the end of 2024.

Much of this projected growth will depend on the outcome of ongoing talc litigation. J&J has faced accusations from customers linking their talcum powder products to a number of health issues, including cancer. If successful, these cases could drastically reduce the company’s net income and total revenue, and threaten its ability to reach its desired EPS growth in 2024.

About the Company

Income Snapshot

Below shows the total revenue, net income and net margin for JNJ. More…

| Total Revenues | Net Income | Net Margin |

| 98.66k | 34.62k | 13.3% |

Cash Flow Snapshot

Below shows the cash from operations, investing and financing for JNJ. More…

| Operations | Investing | Financing |

| 23.42k | -6.19k | -18.02k |

Balance Sheet Snapshot

Below shows the total assets, liabilities and book value per share for JNJ. More…

| Total Assets | Total Liabilities | Book Value Per Share |

| 179.23k | 108.96k | 29.19 |

Key Ratios Snapshot

Some of the financial key ratios for JNJ are shown below. More…

| 3Y Rev Growth | 3Y Operating Profit Growth | Operating Margin |

| 6.9% | 7.9% | 24.4% |

| FCF Margin | ROE | ROA |

| 24.3% | 21.4% | 8.4% |

Price History

JOHNSON & JOHNSON (J&J) is looking for a rebound in their earnings per share (EPS) in 2024, after a series of losses in the past few years. On Wednesday, J&J opened at $155.5 and closed at $156.4, representing a 0.1% increase from the previous day’s closing price of 156.1. Despite the stock’s slight increase, the company must focus on the ongoing talc litigation cases as well as their strategies to regain profitability. J&J is currently facing multiple lawsuits alleging that their baby powder products caused cancerous diseases such as ovarian, mesothelioma, and other forms of cancer. These cases have cost the company billions of dollars in settlements and judgments. In order to reverse this trend, J&J must look to strengthen their product portfolio and find ways to reduce costs in order to boost their margins.

In addition to finding ways to reduce costs, J&J must also find ways to increase revenues. This could include looking for new markets to enter, expanding existing product lines, or introducing new products. The company must also focus on their strategic partnerships with other healthcare companies and vendors to create innovative solutions and products that could drive additional revenue growth. Overall, JOHNSON & JOHNSON is hoping for a turnaround in 2024 as they work to address the talc litigation cases and create strategies for increased profitability. The company has made moves to reduce costs and expand their product offering, and it remains to be seen if these efforts will reap the benefits they are hoping for in the near future. Live Quote…

Analysis

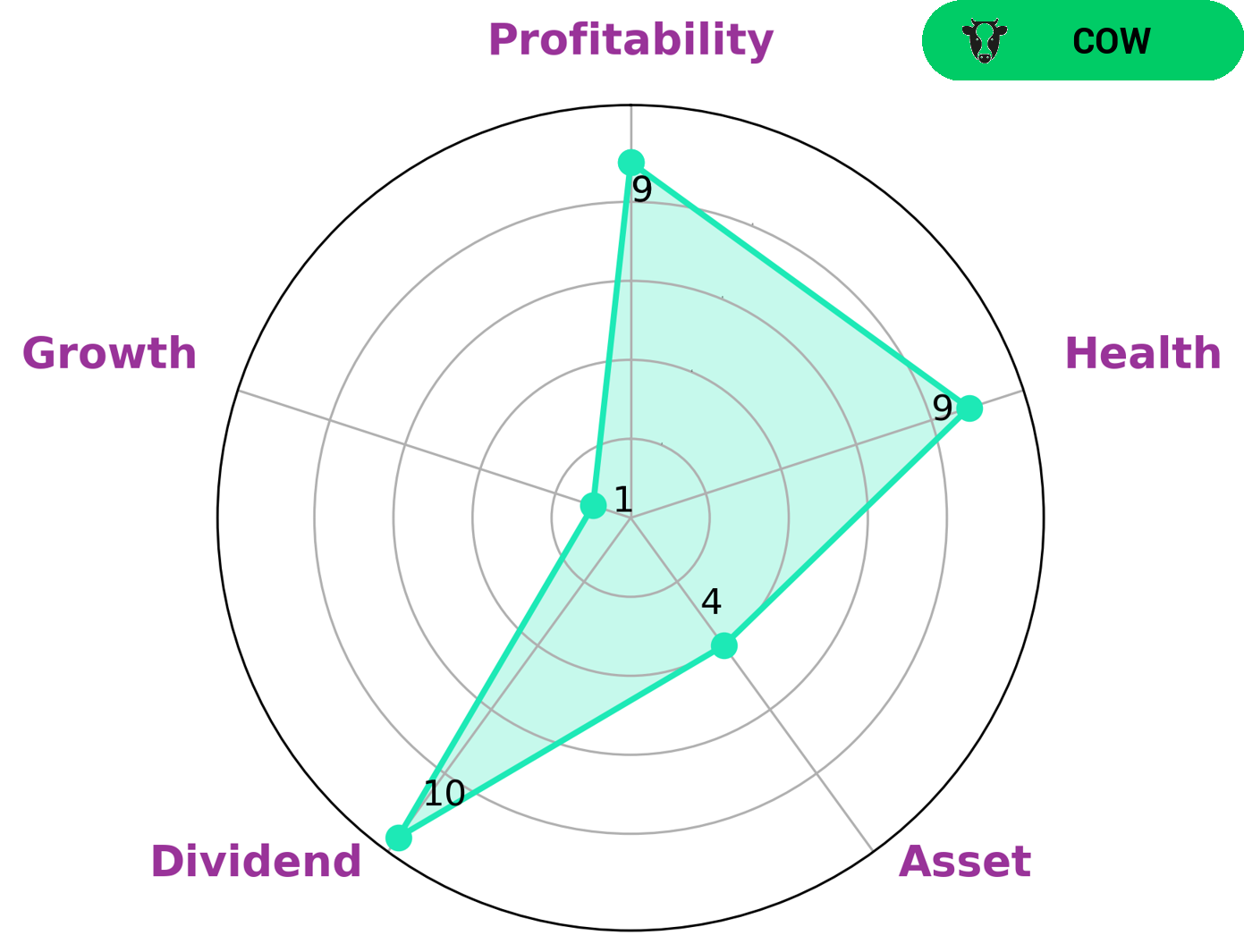

At GoodWhale, we have conducted a deep dive analysis of the fundamentals of JOHNSON & JOHNSON. Our star chart indicates that the company is strong in dividend, profitability, and medium in asset. However, it is weak in growth. After evaluating the company’s fundamentals, we have concluded that it is a ‘cow’, a type of company that has the track record of paying out consistent and sustainable dividends. Investors who are looking for high dividend yields and stable investments may be interested in JOHNSON & JOHNSON. The company also scores 9/10 in the health score with regard to its cashflows and debt. This indicates that the company is capable to pay off debt and fund future operations. As such, JOHNSON & JOHNSON is an ideal investment option for long-term investors who are seeking for consistent income. More…

Peers

The competition between Johnson & Johnson and its competitors is fierce. AstraZeneca PLC, Pfizer Inc, and BioNTech SE are all major players in the pharmaceutical industry, and they are all vying for a piece of the pie. Johnson & Johnson is a well-established company with a long history of success, but its competitors are not to be underestimated. They are all large, well-funded companies with a lot to lose if they don’t win the competition.

– AstraZeneca PLC ($LSE:AZN)

AstraZeneca PLC is a biopharmaceutical company with a market cap of 152.13B as of 2022. The company focuses on the discovery, development, and commercialization of small molecule drugs in the areas of oncology, cardiovascular, and renal & metabolism. The company’s ROE for the year ended December 31, 2020 was -0.94%.

– Pfizer Inc ($NYSE:PFE)

Pfizer Inc is a pharmaceutical company with a market cap of 240.55B as of 2022. The company has a return on equity of 24.63%. Pfizer Inc is a research-based, global pharmaceutical company that discovers, develops, manufactures, and markets medicines for humans and animals. The company’s products include prescription and over-the-counter medicines, vaccines, and biologic therapies.

– BioNTech SE ($NASDAQ:BNTX)

BioNTech SE is a German biotech company founded in 2008 that focuses on the development of Innovation therapies against cancer and other serious diseases. The company has a market cap of 32.91B as of 2022 and a Return on Equity of 71.82%. BioNTech’s mission is to revolutionize the treatment of cancer and other serious diseases by leveraging the power of the immune system. The company is developing a portfolio of immunotherapy products based on its proprietary mRNA technology platform.

Summary

Investors interested in Johnson & Johnson should watch closely for updates on talc litigation, as this could have a significant impact on the company’s bottom line. Analysts believe that, in order to reverse the loss expected on earnings per share (EPS) growth in 2024, JNJ must address the issue of talc litigation. Possible outcomes include large financial settlements, stronger safety measures, or a combination of both.

While JNJ has managed to remain a leader in the healthcare and consumer products industries, these legal proceedings could have a serious effect on the company’s near-term outlook. Investors should keep a close eye on how JNJ responds to the talc litigation in order to gain a better understanding of their possible returns over the next few years.

Related Posts

Recent Posts

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}