Williams-sonoma Intrinsic Value Calculator – Zacks Research Raises Q4 2025 Earnings Forecast for Williams-Sonoma,

March 29, 2024

🌥️Trending News

WILLIAMS-SONOMA ($NYSE:WSM): Williams-Sonoma, Inc. is a well-known American retail company that specializes in high-end kitchenware and home furnishings. Its products are known for their quality and stylish designs, making it a popular choice among consumers. The recent news of Zacks Research raising Q4 2025 earnings forecast for Williams-Sonoma, Inc. has garnered attention from investors and analysts alike. This research firm is widely respected for its accurate forecasts and is considered a trusted source for financial information. This increase in forecasted earnings can be attributed to several key factors. Firstly, Williams-Sonoma has been able to adapt to the changing retail landscape by investing in its e-commerce platform. With the rise of online shopping, the company has focused on enhancing its online presence and providing a seamless shopping experience for its customers. This has resulted in significant growth in its online sales, which has helped boost its overall revenue.

Additionally, Williams-Sonoma has also expanded its product offerings beyond just kitchenware and home furnishings. It now includes brands like West Elm, Pottery Barn, and Rejuvenation, which cater to a wider range of customers and appeal to different demographics. This diversification has helped the company attract new customers and increase its market share. Furthermore, Williams-Sonoma has a strong financial standing, with consistent revenue growth and profitability. The company has also been able to effectively manage its expenses, resulting in a healthy bottom line. This financial stability has allowed them to invest in new initiatives and expand their business while still generating profits. With its strong brand reputation, successful e-commerce strategy, and diverse product offerings, Williams-Sonoma is well-positioned to continue its success in the retail industry. Investors can look forward to positive returns from their investment in this company.

Earnings

Zacks Research has recently released an updated earnings forecast for Williams-Sonoma, Inc., a leading retailer of home furnishings and culinary products. The report, which looks at the company’s performance during the fourth quarter of 2025, predicts a positive outlook for the company’s financials. In its earnings report for the third quarter of fiscal year 2024, which ended on October 31st, 2021, Williams-Sonoma reported a total revenue of 2047.54M USD and a net income of 249.52M USD. While this marks a decrease of 6.6% in total revenue and 0.9% in net income compared to the previous year, it is important to note that the company still achieved a significant amount in both categories. WILLIAMS-SONOMA has also shown steady growth in its total revenue over the past three years, with a reported increase from 2047.54M USD to 1853.65M USD.

This steady growth is indicative of the company’s strong performance and ability to adapt to changing market conditions. With this recent update from Zacks Research, it is clear that Williams-Sonoma is poised for continued success in the coming years. The company’s strong financials and consistent growth demonstrate its resilience and position in the retail industry. As such, investors can have confidence in the company’s future performance and forecasted earnings, making it a promising investment opportunity.

About the Company

Income Snapshot

Below shows the total revenue, net income and net margin for Williams-sonoma. Williams-Sonoma“>More…

| Total Revenues | Net Income | Net Margin |

| 7.92k | 950.32 | 12.0% |

Cash Flow Snapshot

Below shows the cash from operations, investing and financing for Williams-sonoma. Williams-Sonoma“>More…

| Operations | Investing | Financing |

| 1.47k | -254.1 | -630.71 |

Balance Sheet Snapshot

Below shows the total assets, liabilities and book value per share for Williams-sonoma. Williams-Sonoma“>More…

| Total Assets | Total Liabilities | Book Value Per Share |

| 4.88k | 3.07k | 28.27 |

Key Ratios Snapshot

Some of the financial key ratios for Williams-sonoma are shown below. Williams-Sonoma“>More…

| 3Y Rev Growth | 3Y Operating Profit Growth | Operating Margin |

| 7.8% | 20.8% | 15.8% |

| FCF Margin | ROE | ROA |

| 15.3% | 45.7% | 16.1% |

Share Price

Zacks Investment Research has recently raised its fourth quarter 2025 earnings forecast for Williams-Sonoma, Inc. This news has caused a positive impact on the company’s stock, which saw a 1.1% increase in Thursday’s trading session. The stock opened at $316.5 and closed at $317.5, showing a growth of 1.1% from the previous closing price of $314.0. This positive outlook for Williams-Sonoma’s earnings can be attributed to the company’s strong performance in recent quarters and its continued efforts to expand its business. The company has been able to capitalize on the growing demand for home goods and furniture, especially during the pandemic when people have been spending more time at home. In addition to this, Williams-Sonoma has also been investing in its e-commerce platform, which has proven to be highly successful. The company’s online sales have seen a significant increase, and it has been able to reach a wider customer base through its online channels.

This has helped Williams-Sonoma stay ahead of its competitors and maintain a strong position in the market. Moreover, the company has been introducing new and innovative products to cater to the changing needs and preferences of its customers. This has not only helped Williams-Sonoma stay relevant but has also attracted new customers and boosted sales. With Zacks Investment Research raising its earnings forecast for Williams-Sonoma, it is evident that the company is on the right track towards sustained growth and profitability. Its strong financial performance and strategic initiatives make it a promising investment option for investors looking for long-term growth potential. Live Quote…

Analysis – Williams-sonoma Intrinsic Value Calculator

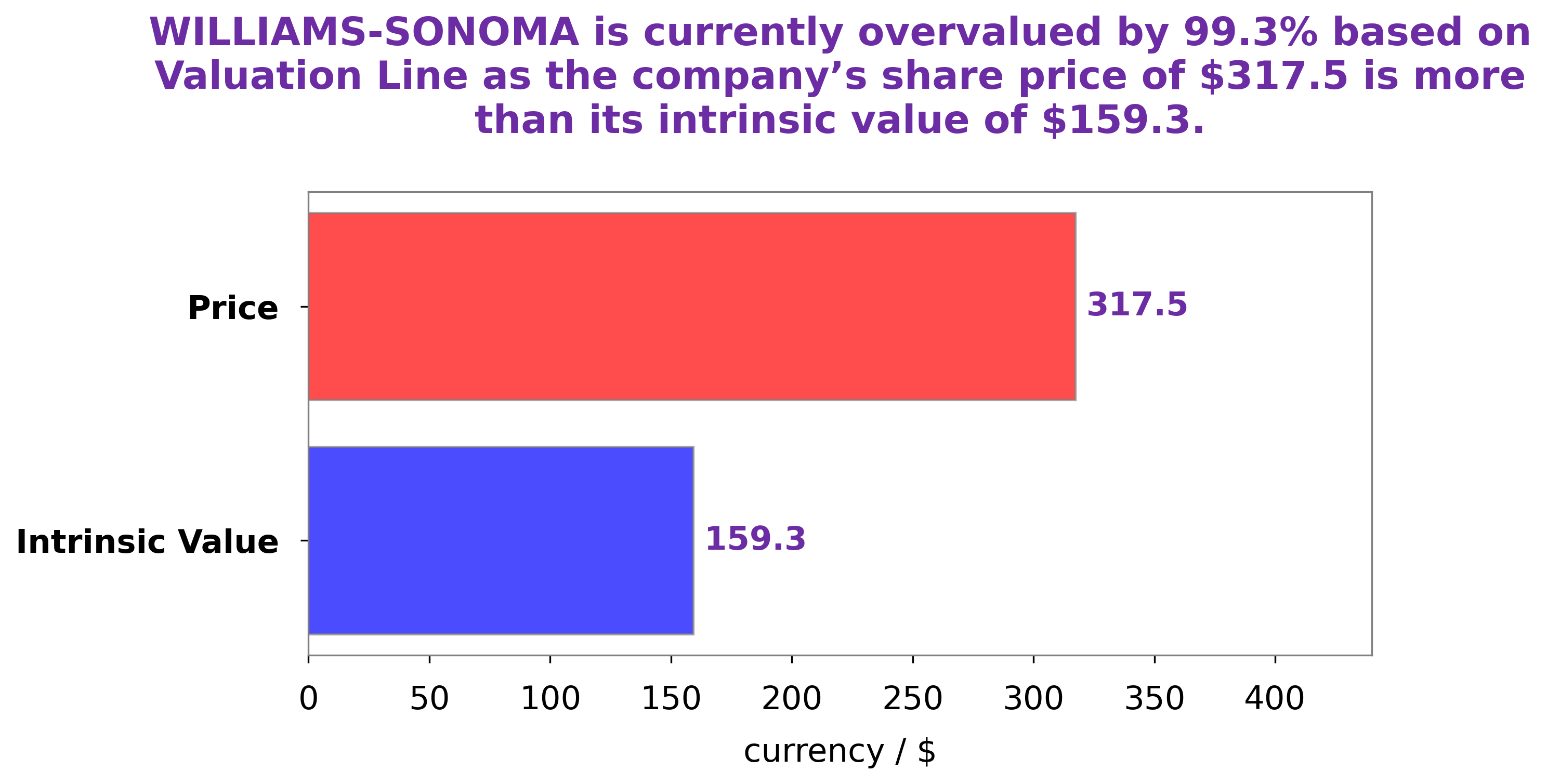

After conducting a thorough analysis of WILLIAMS-SONOMA’s financial standing and overall state of wellbeing, it is clear that the company is currently overvalued. Our team at GoodWhale has utilized our proprietary Valuation Line to determine a fair value for WILLIAMS-SONOMA’s shares, which we have calculated to be approximately $159.3. At the time of this analysis, WILLIAMS-SONOMA’s stock is being traded at a much higher price of $317.5. This reflects an overvaluation of 99.3%, meaning that the current market price of the stock is nearly double what we believe it should be. This significant difference in value suggests that investors may be paying too much for WILLIAMS-SONOMA’s shares. Our Valuation Line takes into consideration numerous factors, including the company’s financial performance, industry trends, and overall market conditions. Based on these metrics, our analysis indicates that WILLIAMS-SONOMA’s stock is currently being overvalued by a considerable margin. Investors should be cautious when considering purchasing WILLIAMS-SONOMA shares at their current price, as it may not accurately reflect the company’s true value. It is always important to conduct thorough research and analysis before making any investment decisions, and our findings suggest that caution should be exercised when it comes to WILLIAMS-SONOMA stock. We will continue to monitor the company’s performance and provide updated insights as needed. Williams-Sonoma“>More…

Peers

The company operates through two segments: Williams-Sonoma and Pottery Barn. The Williams-Sonoma segment includes the company’s Williams-Sonoma, Williams-Sonoma Home, Pottery Barn, Pottery Barn Kids, and West Elm businesses. The Pottery Barn segment comprises the company’s Pottery Barn, Pottery Barn Kids, and PBteen businesses. Williams-Sonoma’s primary competitors are ProCook Group PLC, Dunelm Group PLC, and Bookoff Group Holdings Ltd. All three companies are based in the United Kingdom. ProCook Group PLC is a retailer of kitchenware and cookware. Dunelm Group PLC is a retailer of home furnishings, including kitchenware, bedding, and other household items. Bookoff Group Holdings Ltd is a retailer of used books and media.

– ProCook Group PLC ($LSE:PROC)

ProCook Group PLC is a British cookware company. The company has a market cap of 40.31M as of 2022 and a Return on Equity of 4.17%. ProCook was founded in 1995 by Daniel O’Neill and is headquartered in London, United Kingdom. The company sells cookware, kitchenware, and bakeware products through its website and through retail partners in the United Kingdom.

– Dunelm Group PLC ($LSE:DNLM)

Dunelm Group PLC is a home furnishings retailer in the United Kingdom. The company operates over 170 stores and an online store. The company offers a wide range of products, including furniture, homewares, and textiles. Dunelm Group PLC has a market cap of 1.62B as of 2022, a Return on Equity of 47.66%. The company has been profitable every year since 2010.

– Bookoff Group Holdings Ltd ($TSE:9278)

Bookoff Group Holdings Ltd is a holding company that operates through its subsidiaries in the retail and wholesale of books, music, and other media products in Japan. As of March 31, 2021, the Company operated 524 stores. The company was founded in 1986 and is headquartered in Tokyo, Japan.

Summary

Zacks Research analysts have raised their Q4 2025 earnings per share estimates for Williams-Sonoma, Inc., a home goods and furnishings retailer. This indicates positive sentiment towards the company’s future financial performance. The increase in earnings per share is likely due to expected growth in sales and potential cost-cutting measures.

However, it should be noted that these estimates are subject to change and may not be an accurate reflection of the company’s actual earnings. Overall, this news may be of interest to investors looking to potentially invest in Williams-Sonoma, as it suggests potential for strong financial results in the future.

Related Posts

Recent Posts

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}