WPC Intrinsic Value Calculator – Royal Bank of Canada Reduces W. P. Carey Price Target to $79.00

August 10, 2023

🌥️Trending News

W. P. Carey ($NYSE:WPC) Inc. is a publicly-traded real estate investment trust (REIT) that owns and manages a diversified portfolio of long-term net-lease properties. The company’s portfolio consists of single-tenant, mission-critical properties leased to corporate tenants and government entities on a long-term basis. It remains to be seen how this downgrade will affect W. P. Carey’s stock price in the short term, but it is likely that investors will remain cautious in the near future given continued uncertainty surrounding the wider economy and the net-lease sector specifically. For now, W. P. Carey investors should keep an eye on RBC’s price target of $79.00 and monitor the company’s progress over the coming months as it navigates the effects of the pandemic.

Market Price

The W. P. CAREY stock opened at $66.4 and closed at $66.8, up by 0.3% from prior closing price of 66.6. Investors should keep a close eye on the stock’s performance in the coming days as the price target adjustment could have a significant impact on its future prospects. Live Quote…

About the Company

Income Snapshot

Below shows the total revenue, net income and net margin for WPC. More…

| Total Revenues | Net Income | Net Margin |

| 1.67k | 753.47 | – |

Cash Flow Snapshot

Below shows the cash from operations, investing and financing for WPC. More…

| Operations | Investing | Financing |

| 1.05k | -1.05k | 57.89 |

Balance Sheet Snapshot

Below shows the total assets, liabilities and book value per share for WPC. More…

| Total Assets | Total Liabilities | Book Value Per Share |

| 19.08k | 9.83k | 43.15 |

Key Ratios Snapshot

Some of the financial key ratios for WPC are shown below. More…

| 3Y Rev Growth | 3Y Operating Profit Growth | Operating Margin |

| – | – | 46.2% |

| FCF Margin | ROE | ROA |

| – | – | – |

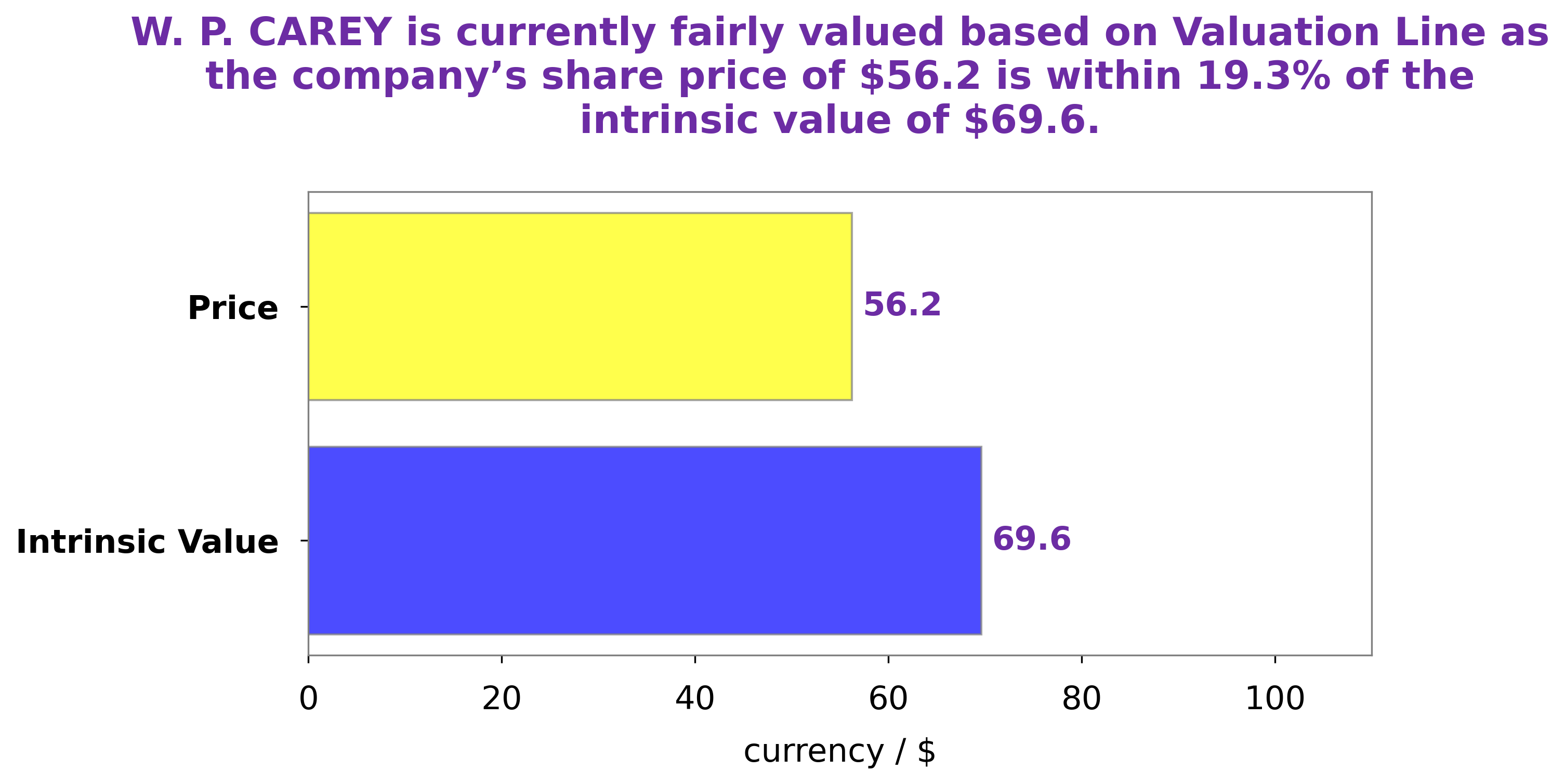

Analysis – WPC Intrinsic Value Calculator

At GoodWhale, we have conducted an analysis to determine the wellbeing of W. P. CAREY. After a thorough assessment of the company and its current market conditions, our proprietary Valuation Line has calculated the fair value of W. P. CAREY share to be around $76.3. This is however lower than the price at which shares of W. P. CAREY are currently being traded, which is at $66.8. This means that W. P. CAREY stock is currently undervalued by 12.5%. More…

Peers

It’s one of the largest owners and operators of single-tenant commercial properties in the U.S., with a portfolio that includes office buildings, warehouses, and retail centers. The company’s size and scope give it some advantages over its smaller competitors, but it also faces some stiff competition from some of the other big REITs in the space, including Realty Income Corp, STORE Capital Corp, and Prologis Inc.

– Realty Income Corp ($NYSE:O)

Realty Income Corporation is a publicly traded real estate investment trust that invests in commercial real estate properties in the United States. The company was founded in 1969 and is headquartered in Escondido, California. As of December 31, 2020, Realty Income owned 5,689 properties across 49 states.

– STORE Capital Corp ($NYSE:STOR)

STORE Capital Corp is a real estate investment trust that focuses on acquiring, financing, and owning net-leased properties. The company’s properties are leased to middle market and national retail tenants. As of December 31, 2020, STORE Capital owned 1,847 properties in 48 states.

– Prologis Inc ($NYSE:PLD)

Prologis Inc is a real estate investment trust that owns, operates, and develops warehouses and distribution centers around the world. As of 2022, it has a market capitalization of $94.6 billion. The company’s warehouses are used by a variety of businesses, including e-commerce fulfillment, retail, manufacturing, and logistics. Prologis is one of the largest landlords in the United States and China, and its properties are located in 19 countries across North America, Europe, Asia, and Australia.

Summary

In particular, RBC noted that WPC’s high-yield exposure, persistent dilution from equity offerings, and the potential for a less favorable rate environment pose risks to the company’s growth prospects. Despite these concerns, RBC remains positive on WPC’s potential for long-term growth and dividend coverage. As such, RBC states that investors should approach WPC with a long-term investment horizon and a buy-on-dips strategy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}