Singapore Post Struggles To Navigate Allocation Of Capital

June 14, 2023

🌧️Trending News

Singapore Post ($SGX:S08), better known as SingPost, is a leading provider of postal, ecommerce and logistics services in Singapore.

However, the company is currently facing difficulty with the allocation of capital. The company has seen its profits decline in recent years due to increased competition in the postal and logistics services market. As a result, it has become increasingly difficult for SingPost to determine how to use its capital. The company has attempted to diversify its business by investing in new technology such as automated sorting machines, but this has not yet been profitable.

Additionally, SingPost has faced challenges with rapidly changing customer needs and preferences. In order to navigate these challenges, SingPost is attempting to focus on core competencies such as providing reliable delivery services and expanding its ecommerce capabilities. The company is also investing in new initiatives such as blockchain technology to stay ahead of the competition. Despite these efforts, it remains to be seen whether SingPost will be able to successfully allocate its capital in order to remain profitable in the long-term.

Price History

On Thursday, Singapore Post (SingPost) stock opened at SG$0.4 and closed at SG$0.4, up 3.5% from its last closing price of SG$0.4. This marks the first time in months that SingPost has seen a positive change to its share price, providing some hope to investors as the company struggles to navigate the process of allocating capital. SingPost currently faces a myriad of challenges, both internally and externally, that contribute to the difficulty of allocating capital. Finance experts say that it is difficult to determine in which areas capital should be invested in order to properly grow the company without incurring too much risk.

Additionally, the heightened economic uncertainty caused by the pandemic has made it difficult for the business to identify what will be successful investments. As a result of these challenges, SingPost has to carefully consider each potential investment before committing any resources. In the short-term, this could mean a period of stagnation as the company takes its time to analyse potential investments and create a comprehensive strategy for allocating capital. In the long-term, however, a more calculated approach could lead to more profitable investments and a renewed confidence in the company’s stock. Live Quote…

About the Company

Income Snapshot

Below shows the total revenue, net income and net margin for Singapore Post. More…

| Total Revenues | Net Income | Net Margin |

| 1.89k | 26.66 | 2.9% |

Cash Flow Snapshot

Below shows the cash from operations, investing and financing for Singapore Post. More…

| Operations | Investing | Financing |

| 70.93 | -56.24 | -58.22 |

Balance Sheet Snapshot

Below shows the total assets, liabilities and book value per share for Singapore Post. More…

| Total Assets | Total Liabilities | Book Value Per Share |

| 2.77k | 1.43k | 0.67 |

Key Ratios Snapshot

Some of the financial key ratios for Singapore Post are shown below. More…

| 3Y Rev Growth | 3Y Operating Profit Growth | Operating Margin |

| 6.6% | -5.6% | 4.5% |

| FCF Margin | ROE | ROA |

| 2.1% | 3.8% | 1.9% |

Analysis

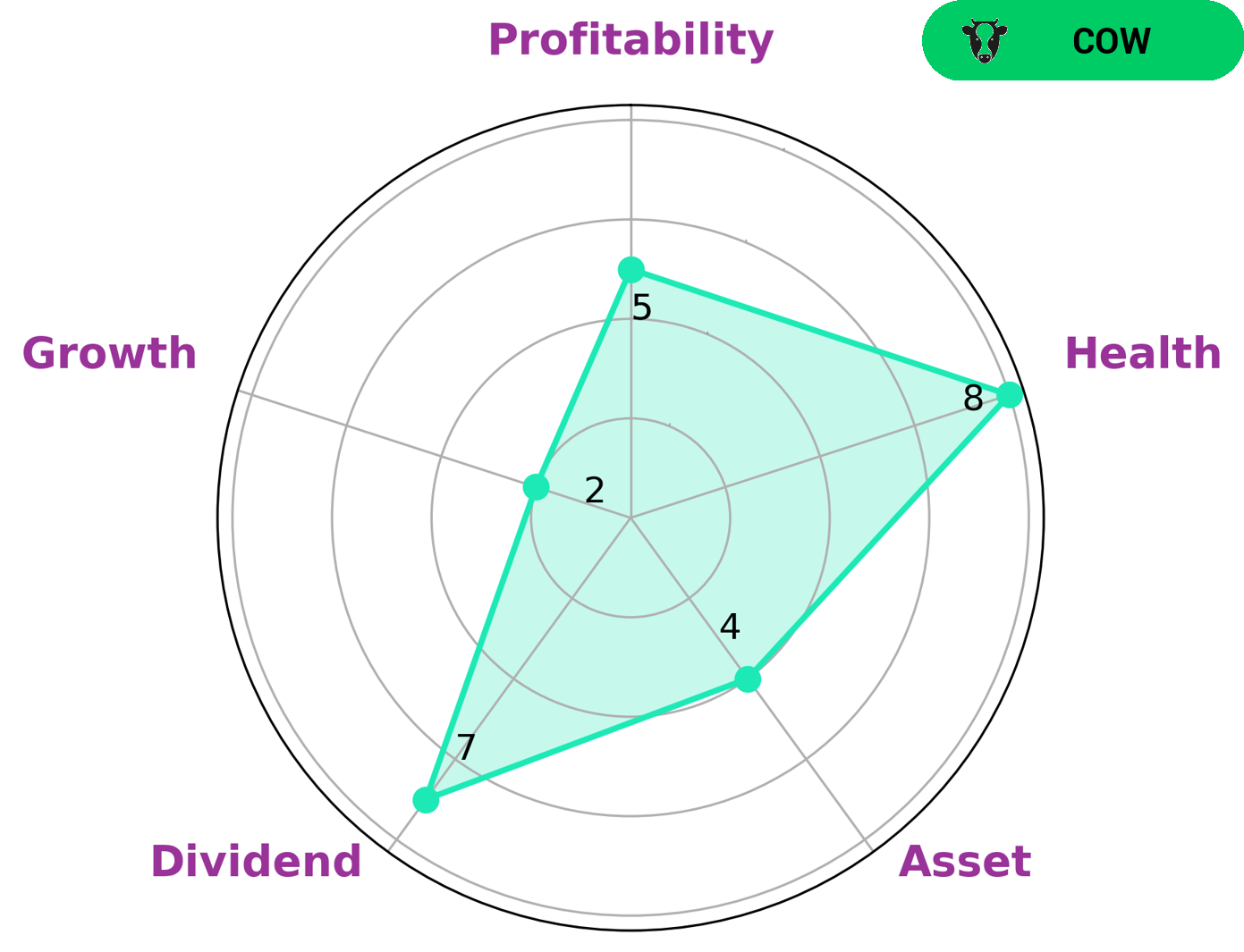

As GoodWhale, we completed an analysis of SINGAPORE POST‘s financials. According to our Star Chart classification, SINGAPORE POST is classified as a ‘rhino’, which implies that the company has achieved moderate revenue or earnings growth. We believe that investors with a long-term investment strategy may be interested in such a company. Furthermore, according to our assessment, SINGAPORE POST has a high health score of 9/10, indicating that it is capable of sustaining future operations even in times of crisis. Additionally, SINGAPORE POST is strong in terms of its cashflows and debt and is medium in asset, dividend, growth, and profitability. More…

Peers

The competition between Singapore Post Ltd and its competitors, GDEX Bhd, Tiong Nam Logistics Holdings Bhd, and CTI Logistics Ltd, is fierce. All four companies are working hard to provide the best delivery services and customer experience, with each vying for a larger share of the market. With their diverse offerings and innovative approaches, customers have a lot of choice when it comes to selecting a provider.

– GDEX Bhd ($KLSE:0078)

GDEX Bhd is a Malaysian-based logistics and courier service provider that offers a range of delivery services for both domestic and international customers. With a market capitalization of 835.27 million as of 2022, GDEX Bhd is one of the largest logistics and courier service companies in the region. Its return on equity (ROE) stands at 8.41%, which indicates that the company is able to generate a return that is above the industry average. This suggests that the company’s management has been able to make the best use of its resources and investments, resulting in higher returns for shareholders.

– Tiong Nam Logistics Holdings Bhd ($KLSE:8397)

Tiong Nam Logistics Holdings Bhd is a Malaysian-based logistics and transport services provider. The company has a market capitalization of 408.67M as of 2022, representing the total value of the company’s outstanding shares. Additionally, it has a Return on Equity (ROE) of 4.51%, which measures how much profit the company produces relative to the amount of shareholder equity. The company provides a wide range of services including freight forwarding, warehousing, and transportation services. It also provides supply chain management solutions to its customers. Tiong Nam Logistics Holdings Bhd is one of the leading players in the logistics and transport industry in Malaysia.

– CTI Logistics Ltd ($ASX:CLX)

CTI Logistics Ltd is a leading provider of supply chain and logistics solutions. The company provides services such as freight forwarding, customs clearance, warehousing and distribution, and other services related to international trade. Its market capitalization of 122.67 million as of 2022 reflects the company’s immense growth, making it one of the leading players in the industry. Its Return on Equity (ROE) of 16.49% indicates the company’s strong financial performance and indicates CTI Logistics Ltd’s ability to efficiently utilize its assets and generate returns.

Summary

Singapore Post, or SingPost, has experienced a mixed performance in recent years. The company’s stock price moved up on the day of the announcement as investors saw an opportunity to capitalize on the company’s capital allocation capabilities. Despite the short-term gain, investors should take a more long-term view when analyzing SingPost. The company’s fundamentals have been weak in recent years, with declining revenue and profits.

However, there are some signs that the company is starting to turn things around. Over the past few years, SingPost has been actively investing in new technologies and services to improve customer experience and strengthen its competitive position. It is also trying to diversify its revenue streams by launching new business models such as its e-commerce marketplace. While it may still be too early to draw conclusions about the success of SingPost’s investments, it is clear that the company is making moves to improve its financial performance in the long run.

Related Posts

Recent Posts

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}