Singapore Post Investors Face Unprofitable Last Five Years

December 18, 2023

🌥️Trending News

Singapore Post ($SGX:S08), commonly known as SingPost, is one of the largest postal companies in Southeast Asia.

However, for investors of Singapore Post, the past five years have not been profitable. This is largely the result of a series of costly acquisitions that led to a sharp increase in debt. This debt has continued to drag down SingPost’s profitability and created a difficult environment for the company’s shareholders. In addition to this, SingPost has been faced with other challenges such as an increasingly competitive market and rising operating costs. These challenges have further weighed down on its profitability and made it difficult for investors to realize any returns from their investments. All in all, the last five years have been a difficult time for Singapore Post investors. With declining share prices and an uncertain future, investors are left with few options. However, with the right financial strategy and a commitment to turning the business around, there may still be hope for those invested in this company.

Share Price

On Wednesday, SINGAPORE POST stock opened at SG$0.4 and closed at SG$0.4. This is testament to the fact that the company has not been able to turn a profit for investors in the past five years. Despite the continuous losses, the company remains committed to finding ways to make the business more successful. With the current market challenges, SINGAPORE POST has had to make significant changes to their operations in order to stay afloat.

They have been focusing on maintaining cost efficiencies, leveraging their digital capabilities, and increasing customer satisfaction. Going forward, SINGAPORE POST will continue to work tirelessly to improve its financial performance and deliver value for its investors. Live Quote…

About the Company

Income Snapshot

Below shows the total revenue, net income and net margin for Singapore Post. More…

| Total Revenues | Net Income | Net Margin |

| 1.74k | 35.16 | 2.9% |

Cash Flow Snapshot

Below shows the cash from operations, investing and financing for Singapore Post. More…

| Operations | Investing | Financing |

| 117.88 | -24.55 | -79.68 |

Balance Sheet Snapshot

Below shows the total assets, liabilities and book value per share for Singapore Post. More…

| Total Assets | Total Liabilities | Book Value Per Share |

| 2.75k | 1.39k | 0.61 |

Key Ratios Snapshot

Some of the financial key ratios for Singapore Post are shown below. More…

| 3Y Rev Growth | 3Y Operating Profit Growth | Operating Margin |

| 8.2% | -7.6% | 5.9% |

| FCF Margin | ROE | ROA |

| 4.6% | 4.7% | 2.3% |

Analysis

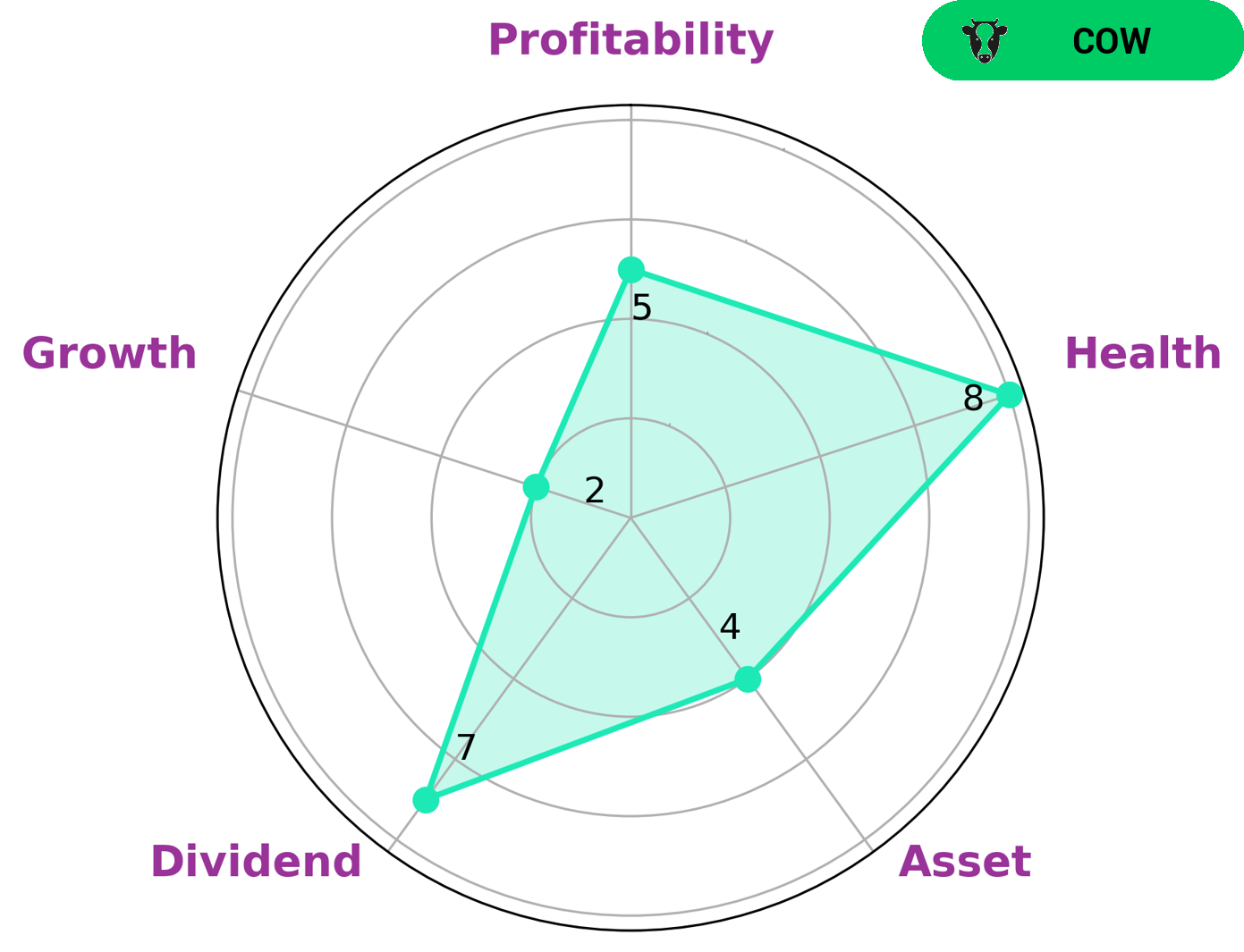

At GoodWhale, we have conducted an analysis of Singapore Post‘s fundamentals. The Star Chart assigned Singapore Post a health score of 8/10, indicating that the company has healthy cash flows and debt, and is capable of paying off debt and funding future operations. We classify Singapore Post as a ‘cow’, which is a company that has the track record of consistently paying out dividends. Given Singapore Post’s strong dividend, medium asset, profitability, and weak growth metrics, investors who are looking for a steady source of dividend income may be interested in investing in this company. Furthermore, value investors who are not looking for high growth opportunities may also be interested in investing in Singapore Post. More…

Peers

The competition between Singapore Post Ltd and its competitors, GDEX Bhd, Tiong Nam Logistics Holdings Bhd, and CTI Logistics Ltd, is fierce. All four companies are working hard to provide the best delivery services and customer experience, with each vying for a larger share of the market. With their diverse offerings and innovative approaches, customers have a lot of choice when it comes to selecting a provider.

– GDEX Bhd ($KLSE:0078)

GDEX Bhd is a Malaysian-based logistics and courier service provider that offers a range of delivery services for both domestic and international customers. With a market capitalization of 835.27 million as of 2022, GDEX Bhd is one of the largest logistics and courier service companies in the region. Its return on equity (ROE) stands at 8.41%, which indicates that the company is able to generate a return that is above the industry average. This suggests that the company’s management has been able to make the best use of its resources and investments, resulting in higher returns for shareholders.

– Tiong Nam Logistics Holdings Bhd ($KLSE:8397)

Tiong Nam Logistics Holdings Bhd is a Malaysian-based logistics and transport services provider. The company has a market capitalization of 408.67M as of 2022, representing the total value of the company’s outstanding shares. Additionally, it has a Return on Equity (ROE) of 4.51%, which measures how much profit the company produces relative to the amount of shareholder equity. The company provides a wide range of services including freight forwarding, warehousing, and transportation services. It also provides supply chain management solutions to its customers. Tiong Nam Logistics Holdings Bhd is one of the leading players in the logistics and transport industry in Malaysia.

– CTI Logistics Ltd ($ASX:CLX)

CTI Logistics Ltd is a leading provider of supply chain and logistics solutions. The company provides services such as freight forwarding, customs clearance, warehousing and distribution, and other services related to international trade. Its market capitalization of 122.67 million as of 2022 reflects the company’s immense growth, making it one of the leading players in the industry. Its Return on Equity (ROE) of 16.49% indicates the company’s strong financial performance and indicates CTI Logistics Ltd’s ability to efficiently utilize its assets and generate returns.

Summary

Investing in Singapore Post over the past five years has been a poor decision for investors. Over the same period, the Singapore Postal Savings Bank also posted losses. Analysts suggest that Singapore Post’s declining performance may be linked to the rapid growth of e-commerce companies, which have taken over a lot of the post office’s traditional business.

Additionally, the company has not pursued any major new business initiatives which may help it succeed in this increasingly competitive market. Investors should proceed with caution before investing in Singapore Post and consider other options in the rapidly changing postal landscape.

Related Posts

Recent Posts

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}