Q2 Performance Stumbles for J.B. Hunt Transport Services Amid Freight Recession

July 20, 2023

🌧️Trending News

Unfortunately, the company experienced a decline in its second quarter performance, as the freight recession had taken its toll. A freight recession occurs when demand for transportation services slows down, reducing the number of shipments for companies like J.B. ($NASDAQ:JBHT) Hunt Transport Services. This reduction in demand meant that J.B. Hunt Transport Services was unable to maintain the same levels of revenue and profitability as during previous quarters, resulting in a stumble for the company. Despite this setback, the company is confident that it will be able to recover by taking proactive measures to address the impact of the freight recession and continuing to focus on cost efficiency and customer service.

Price History

Despite the setback, their stock opened at $195.0 and closed at $195.2, up by 3.8% from its previous closing price of 188.2. This suggests that investors are optimistic about the company’s recovery in the future. However, J.B. Hunt remains confident in its ability to weather the challenging economic environment and focus on finding solutions to improve their overall performance. Through cost-cutting initiatives and aggressive expansion strategies, J.B. Hunt hopes to return to profitable growth in the near future. Live Quote…

About the Company

Income Snapshot

Below shows the total revenue, net income and net margin for JBHT. More…

| Total Revenues | Net Income | Net Margin |

| 13.85k | 858 | 6.2% |

Cash Flow Snapshot

Below shows the cash from operations, investing and financing for JBHT. More…

| Operations | Investing | Financing |

| 2.09k | -1.55k | -530.43 |

Balance Sheet Snapshot

Below shows the total assets, liabilities and book value per share for JBHT. More…

| Total Assets | Total Liabilities | Book Value Per Share |

| 8.25k | 4.34k | 35.38 |

Key Ratios Snapshot

Some of the financial key ratios for JBHT are shown below. More…

| 3Y Rev Growth | 3Y Operating Profit Growth | Operating Margin |

| 14.4% | 19.3% | 8.6% |

| FCF Margin | ROE | ROA |

| 8.8% | 20.3% | 9.0% |

Analysis

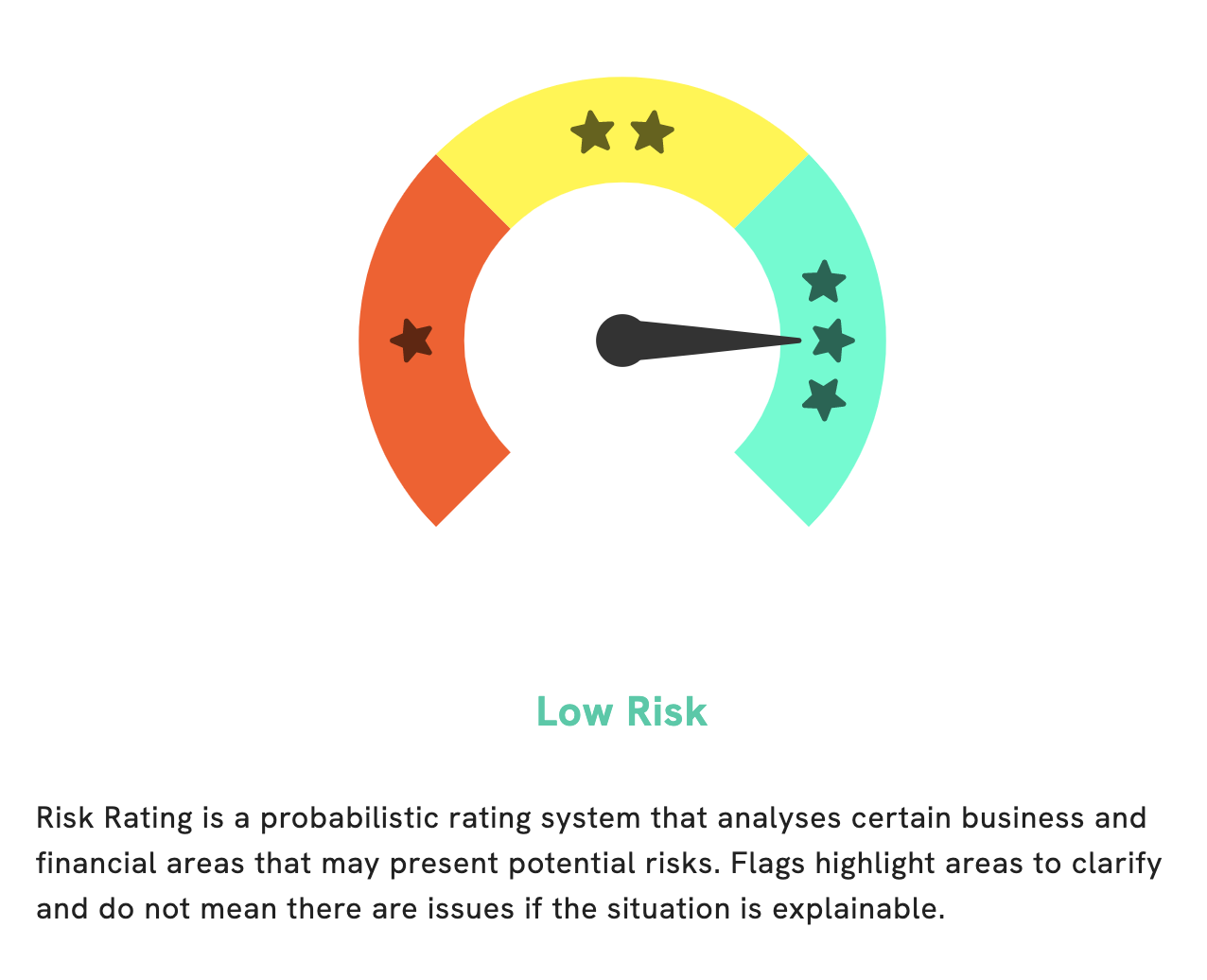

At GoodWhale, we have conducted a comprehensive analysis of J.B. HUNT TRANSPORT SERVICES’ fundamentals to determine its level of risk. Our Risk Rating has concluded that it is a low risk investment with regards to financial and business aspects. We have also identified one risk warning in the company’s balance sheet, which can be further explored by registering with GoodWhale. With our help, you can make an informed decision about investing in J.B. HUNT TRANSPORT SERVICES. More…

Peers

JB Hunt Transport Services Inc is a leading transportation provider in North America. The company operates in four segments: Intermodal (JBHT), Dedicated Contract Services (DCS), Integrated Capacity Solutions (ICS), and Truck (JBT). The company has a fleet of over 16,000 trucks and more than 48,000 trailers. JBHT offers a wide range of transportation services including intermodal, dedicated contract, and truckload. The company has a strong market position in the United States and Canada.

JBHT competes with Hub Group Inc, Yang Ming Marine Transport Corp, Rinko Corp, and other transportation companies in the United States and Canada. The company has a strong market position and a large fleet of trucks and trailers. JBHT offers a wide range of transportation services. The company has a strong financial position and is expected to grow at a fast pace in the coming years.

– Hub Group Inc ($NASDAQ:HUBG)

Hub Group is a transportation management company that provides intermodal, truck brokerage and logistics services. Hub Group’s intermodal services include rail-to-truck and truck-to-rail transloading, as well as drayage service. The company’s truck brokerage services provide full truckload, less-than-truckload and dedicated contract carriage. Hub Group’s logistics services include supply chain management and warehouse management.

As of 2022, Hub Group’s market cap is $2.59 billion. The company’s return on equity is 21.81%. Hub Group is a transportation management company that provides intermodal, truck brokerage and logistics services. The company’s intermodal services include rail-to-truck and truck-to-rail transloading, as well as drayage service. The company’s truck brokerage services provide full truckload, less-than-truckload and dedicated contract carriage. Hub Group’s logistics services include supply chain management and warehouse management.

– Yang Ming Marine Transport Corp ($TWSE:2609)

As of 2022, Yang Ming Marine Transport Corp has a market cap of 220B and a Return on Equity of 62.35%. The company is a leading provider of international ocean transportation services. It operates a modern fleet of container vessels and provides integrated logistics services. The company has a strong market position in the Far East, Europe, and the Middle East.

– Rinko Corp ($TSE:9355)

Rinko Corp is a Japanese company that manufactures and sells construction materials. The company has a market cap of 3.82B as of 2022 and a return on equity of 4.29%. Rinko Corp is a well-established company with a strong financial position. The company’s products are in high demand, and its products are used in a wide variety of applications. Rinko Corp has a strong market presence and is a market leader in its industry.

Summary

Despite this, the company’s stock price moved up the same day. Investors have taken a cautiously optimistic outlook on the company despite the weak performance, as J.B. Hunt continues to remain one of the largest transportation service providers in North America. With the strong management team and extensive network of terminals and resources, the company is well-positioned for long-term success, and may be a smart investment for those looking to capitalize on an upturn in the freight market.

Related Posts

Recent Posts

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}