Analysts Recommend ‘Moderate Buy’ for Booz Allen Hamilton Holding Co.

November 16, 2023

☀️Trending News

Analysts have recently given Booz Allen Hamilton ($NYSE:BAH) Holding Co. an average recommendation of “Moderate Buy”. This assessment is based on the company’s strong financial position, resilient business model, and impressive track record in the market. As one of the largest management consulting firms in the world, Booz Allen Hamilton has a long history of helping businesses and organizations solve complex problems and solve strategic challenges. They provide a wide range of services and solutions to both public and private sector clients in the areas of defense and national security, health, energy, economic development, and technology. Over the years, it has consistently achieved positive returns, even during times of market volatility.

With an experienced management team and a well-defined growth strategy, analysts believe that the company is in a strong position to continue delivering value to its shareholders. Given these positive factors and its strong financial position, analysts believe that BOOZ ALLEN HAMILTON HOLDING Co. is a sound investment for long-term gains. They recommend a ‘Moderate Buy’ rating on the stock for investors looking for steady returns. The company’s current share price offers an attractive entry point for new investors, and with the right level of diversification, could provide long-term value.

Price History

On Wednesday, the stock opened at $129.1 and closed at $126.8, a drop of 2.0% from the previous closing price of 129.3. This follows the holding company’s positive earnings report last quarter and subsequent announcement of dividend payments and share repurchases in the upcoming period. Analysts believe that the stock’s current price offers a good entry point and there is potential for upside in the short to medium term.

They also highlighted the company’s strong balance sheet and experienced management team. Overall, analysts are bullish on the long-term prospects of BOOZ and have graded it a ‘moderate buy’. Live Quote…

About the Company

Income Snapshot

Below shows the total revenue, net income and net margin for BAH. More…

| Total Revenues | Net Income | Net Margin |

| 10.03k | 294.68 | 2.9% |

Cash Flow Snapshot

Below shows the cash from operations, investing and financing for BAH. More…

| Operations | Investing | Financing |

| 256.81 | -519.35 | 63.31 |

Balance Sheet Snapshot

Below shows the total assets, liabilities and book value per share for BAH. More…

| Total Assets | Total Liabilities | Book Value Per Share |

| 7.16k | 6.09k | 8.22 |

Key Ratios Snapshot

Some of the financial key ratios for BAH are shown below. More…

| 3Y Rev Growth | 3Y Operating Profit Growth | Operating Margin |

| 8.8% | -10.3% | 5.5% |

| FCF Margin | ROE | ROA |

| 1.8% | 32.8% | 4.8% |

Analysis

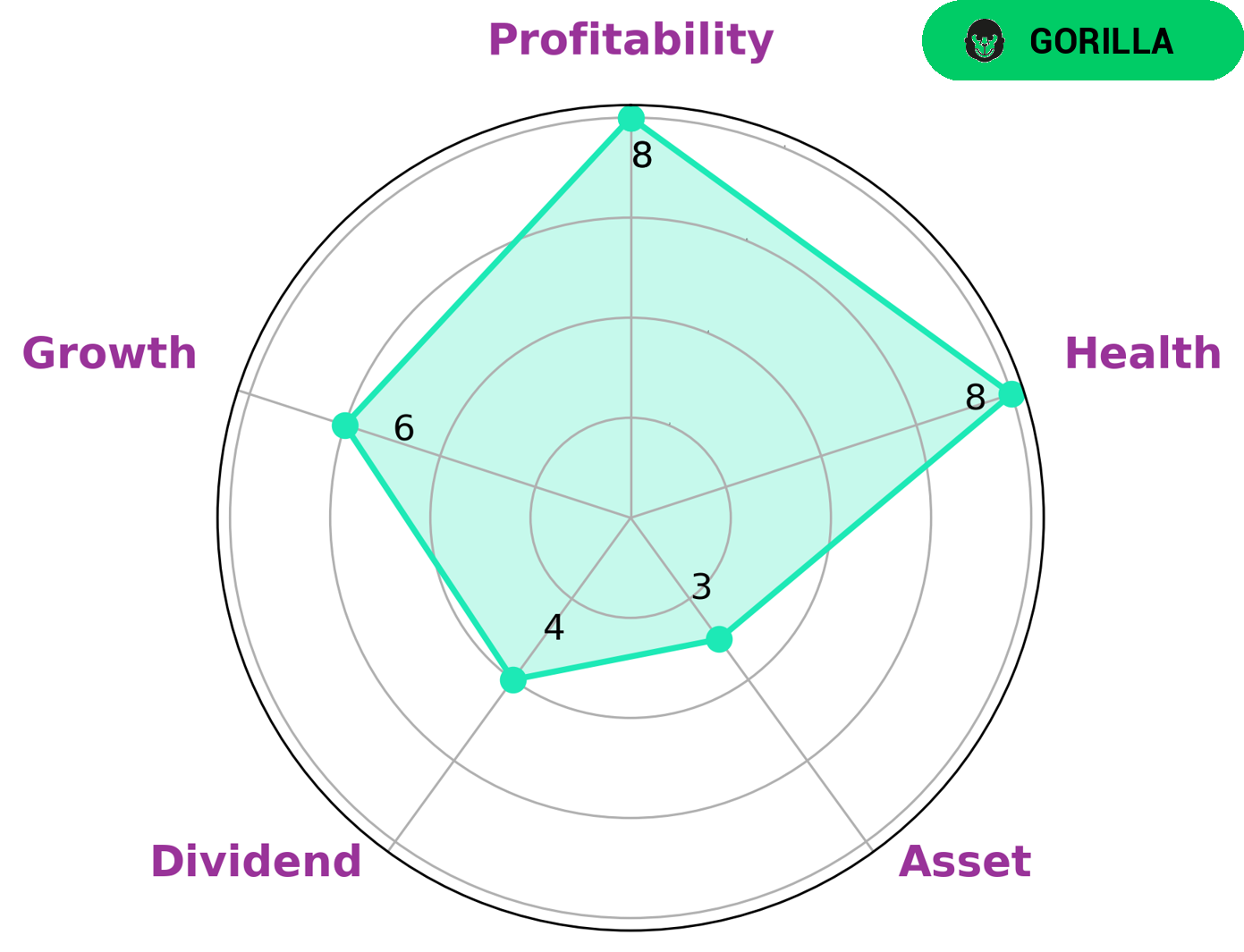

GoodWhale’s analysis of BOOZ ALLEN HAMILTON HOLDING’s financials shows a very healthy score of 8/10 on its Star Chart. This indicates that the company is in a strong position to handle any crisis or future operations. BOOZ ALLEN HAMILTON HOLDING is classified as a ‘rhino’, which means that it has achieved moderate revenue or earnings growth. Investors who are interested in this type of company may consider BOOZ ALLEN HAMILTON HOLDING for its strong profitability, medium dividend growth, and weak asset. The company’s current financials indicate that it is very capable of handling future operations and should be able to weather any crisis. Additionally, with its moderate growth, it could be an attractive option for many investors. More…

Peers

The global management consulting market is expected to grow at a CAGR of 6.2% from 2019 to 2026. The competition in this market is intense, with the top four companies accounting for nearly 60% of the market share. Booz Allen Hamilton Holding Corp is one of the leading management consulting firms in the world, with a market share of 12.4%. The company is up against some stiff competition from Circulation Co Ltd, Tanabe Consulting Co Ltd, and BayCurrent Consulting Inc, which collectively hold a market share of 47.6%.

– Circulation Co Ltd ($TSE:7379)

The market cap for China International Marine Containers (Group) Co Ltd has been on a steady decline since early 2020, from over 20 billion to its current 14.08 billion. However, the company’s ROE has remained relatively stable at 14.03%. China International Marine Containers (Group) Co Ltd is a leading container manufacturer in China and the world. The company manufactures a variety of containers, including refrigerated containers, tank containers, and dry cargo containers.

– Tanabe Consulting Co Ltd ($TSE:9644)

As of 2022, Tanabe Consulting Co Ltd has a market cap of 10.48B and a Return on Equity of 5.99%. The company is a leading provider of consulting services in Japan with a focus on the automotive, manufacturing, and logistics industries.

– BayCurrent Consulting Inc ($TSE:6532)

BayCurrent Consulting Inc has a market cap of 646.59B as of 2022, a Return on Equity of 34.97%. The company is a provider of consulting services. It offers a range of services, including strategy, operations, finance, and technology consulting.

Summary

Analysts have released an average recommendation of “Moderate Buy” for Booz Allen Hamilton Holding Co. Investors are advised to consider the risks and potential rewards of investing in the company. The current market sentiment has been moderate, with analysts expecting the stock to perform well in the short-term. The company has a strong financial position and is seen as a good option for conservative investors.

Analyst forecasts suggest strong revenue and earnings growth for the company in the coming years, with some believing it is undervalued relative to its peers. Investors are encouraged to review all the available information before making an investment decision.

Related Posts

Recent Posts

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}