Nordstrom’s Decade of Growth Not Enough to Keep Investors Interested

June 25, 2023

☀️Trending News

Nordstrom ($NYSE:JWN), the American fashion retailer, has enjoyed a decade of immense growth, however, this isn’t enough to keep investors interested. Despite the company’s success in recent years, investors are looking for more. They are now turning to other opportunities in order to diversify their portfolio. It is known for its quality clothing and footwear brands, as well as its friendly customer service. Nordstrom has had a positive track record of success over the past 10 years, with strong sales and profits.

However, due to the current economic climate and stock market volatility, investors are no longer convinced that Nordstrom is the best place to put their money.

Price History

On Wednesday, NORDSTROM stock opened at $16.5 and closed the day at $16.2, representing a 2.4% increase from the previous closing price of $15.8. Despite this growth, investors do not seem to be overly interested in the company’s prospects. This comes after the company has experienced nearly a decade of growth, including a considerable expansion into the retail market. However, recent economic conditions and changing consumer habits have pushed NORDSTROM to face new challenges and investors appear wary of its ability to continue to grow. Nordstroms_Decade_of_Growth_Not_Enough_to_Keep_Investors_Interested”>Live Quote…

About the Company

Income Snapshot

Below shows the total revenue, net income and net margin for Nordstrom. More…

| Total Revenues | Net Income | Net Margin |

| 15.14k | 20 | 0.1% |

Cash Flow Snapshot

Below shows the cash from operations, investing and financing for Nordstrom. More…

| Operations | Investing | Financing |

| 775 | -505 | -171 |

Balance Sheet Snapshot

Below shows the total assets, liabilities and book value per share for Nordstrom. More…

| Total Assets | Total Liabilities | Book Value Per Share |

| 8.83k | 8.28k | 3.41 |

Key Ratios Snapshot

Some of the financial key ratios for Nordstrom are shown below. More…

| 3Y Rev Growth | 3Y Operating Profit Growth | Operating Margin |

| 2.2% | -16.0% | 0.9% |

| FCF Margin | ROE | ROA |

| 1.9% | 13.9% | 1.0% |

Analysis

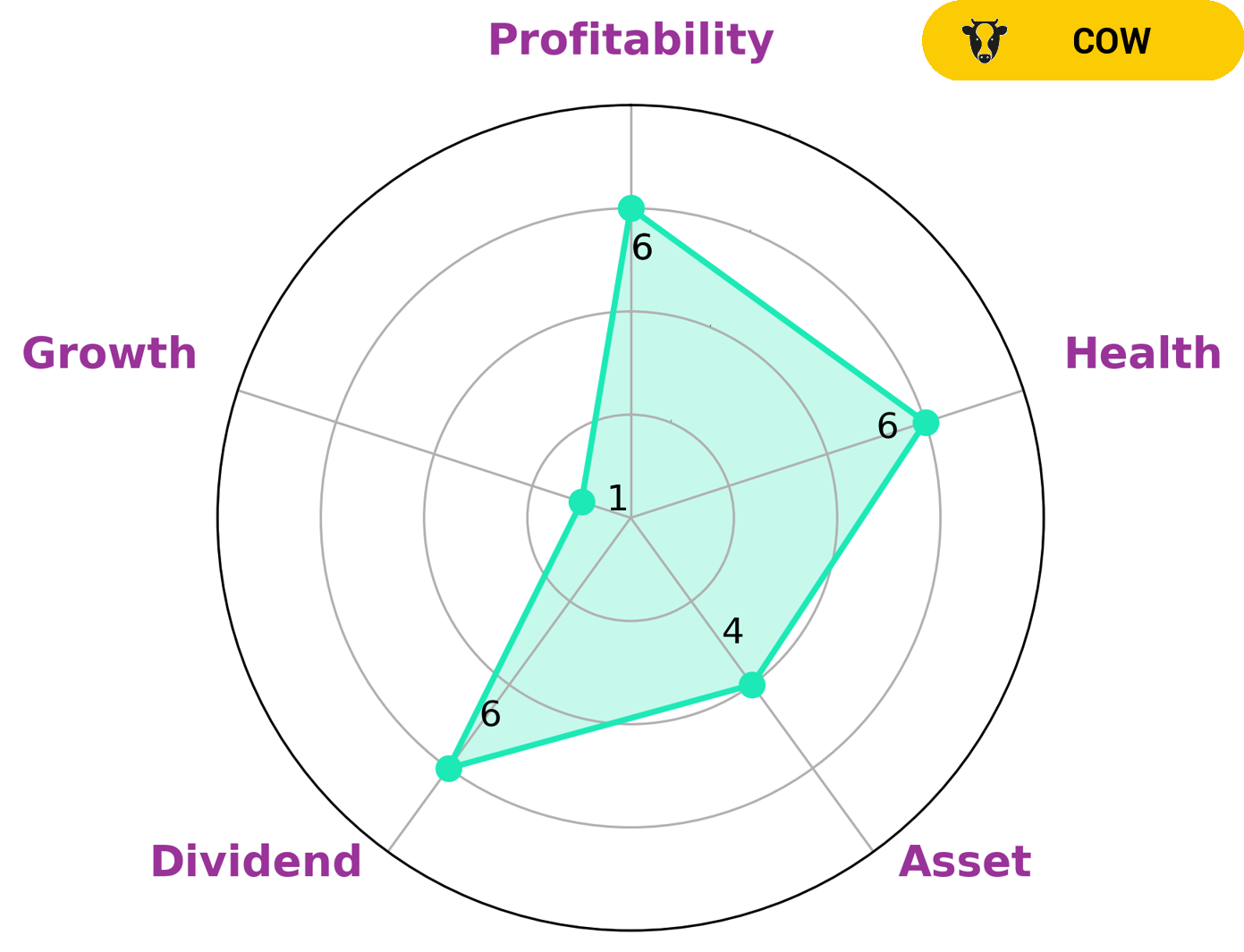

GoodWhale has conducted an analysis of Nordstrom‘s financials and, based on our Star Chart, has determined that the company is strong in profitability, medium in assets and weak in growth and dividends. We rate Nordstrom’s overall health as 6/10, as it appears to have enough cashflow and debt to pay off debt and fund future operations. We have classified Nordstrom as an ‘elephant’, a type of company that is rich in assets after deducting off liabilities. Such a company could be attractive to investors looking for an established company with resources to sustain them in the long term. For instance, investors looking for a steady return and a safe investment may be interested, as well as those who are bullish on the company’s potential for growth. More…

Peers

The retail market is a fiercely competitive one, and nowhere is this more apparent than in the battle between Nordstrom Inc and its rivals Kohl’s Corp, Macy’s Inc, and Chiyoda Co Ltd. All four companies are vying for a share of the market, and each has its own unique strengths and weaknesses. Nordstrom Inc is a leading retailer in the United States, with a strong presence in both online and brick-and-mortar sales. Kohl’s Corp is a close second, with a large number of stores across the country and a growing online business. Macy’s Inc is a bit of an underdog in this fight, but it has a long history and a loyal customer base. Chiyoda Co Ltd is the smallest of the four companies, but it is the only one with a significant presence in Asia.

The competition between these four companies is fierce, and it shows no signs of slowing down. Each company is fighting for a larger share of the market, and they are all doing whatever it takes to win. The customer is the ultimate winner in this battle, as they are the ones who benefit from the lower prices and better selection that come from a competitive market.

– Kohl’s Corp ($NYSE:KSS)

Kohl’s Corp is a large retail company with a market cap of 3.37B as of 2022. The company has a Return on Equity of 16.46%. Kohl’s Corp is a retailer that operates primarily in the United States. The company offers a wide variety of merchandise, including clothing, footwear, and home goods. Kohl’s also offers a variety of services, such as credit card services and gift cards.

– Macy’s Inc ($NYSE:M)

Macy’s Inc is an American department store chain founded in 1858. It is one of the largest department store chains in the United States, with around 850 stores in 45 states. Macy’s Inc has a market cap of $5.14B as of 2022 and a Return on Equity of 40.81%. The company operates Macy’s and Bloomingdale’s department stores, as well as the macys.com and bloomingdales.com websites. Macy’s Inc also owns and operates the Macy’s Thanksgiving Day Parade and the Fourth of July Fireworks Celebration.

– Chiyoda Co Ltd ($TSE:8185)

Chiyoda Co Ltd is a Japanese company that provides engineering, construction, and other services. The company has a market capitalization of 25.03 billion as of 2022 and a return on equity of -2.63%. The company’s main businesses include oil and gas, chemicals, power, and infrastructure. Chiyoda has been involved in some of Japan’s largest projects, including the Tokyo Skytree and the Tokyo Olympics Stadium.

Summary

Nordstrom has seen significant growth in the last decade, but it may be a good time for investors to consider reallocating their funds to other investments. Despite impressive financial gains, Nordstrom’s stocks are now facing concerns over the company’s high debt levels and the looming threat of competition from e-commerce giants. Analysts also point to slowing same-store sales growth, a lack of profitability in their e-commerce segment, and a recent leadership shakeup as potential warning signs. Investors should perform their due diligence to determine whether Nordstrom is still a viable long-term investment.

Related Posts

Recent Posts

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Investing Everyone Can Do.

Investing shouldn’t be exclusive to a select few. We believe everyone should have the opportunity to grow their wealth. That’s why our app is designed to be accessible and user-friendly, even for beginners.