TOAST Stock Plummets Over 20% After Mixed Q4 Results and Soft 2023 Forecast

February 20, 2023

Trending News 🌥️

The company’s fourth quarter results were disappointing, causing its stock to plummet over 20%. Subscription revenue also fell short of expectations, coming in at $95M compared to the consensus estimate of $98M. This news caused a sell-off in the market and investors have been quick to reassess their opinion of the company. As investors digest the news and reassess the future outlook for Toast ($NYSE:TOST), it remains to be seen if this stock will recover from the hit it took today.

Share Price

On Thursday, the company’s stock opened at $21.0 and closed at $20.0, plummeting by 22.8% from its previous closing price of $26.0. Live Quote…

About the Company

Income Snapshot

Below shows the total revenue, net income and net margin for Toast. More…

| Total Revenues | Net Income | Net Margin |

| 2.73k | -275 | -13.5% |

Cash Flow Snapshot

Below shows the cash from operations, investing and financing for Toast. More…

| Operations | Investing | Financing |

| -156 | -98 | 38 |

Balance Sheet Snapshot

Below shows the total assets, liabilities and book value per share for Toast. More…

| Total Assets | Total Liabilities | Book Value Per Share |

| 1.76k | 663 | 2.16 |

Key Ratios Snapshot

Some of the financial key ratios for Toast are shown below. More…

| 3Y Rev Growth | 3Y Operating Profit Growth | Operating Margin |

| 60.1% | – | -14.1% |

| FCF Margin | ROE | ROA |

| -6.9% | -21.7% | -13.6% |

Analysis

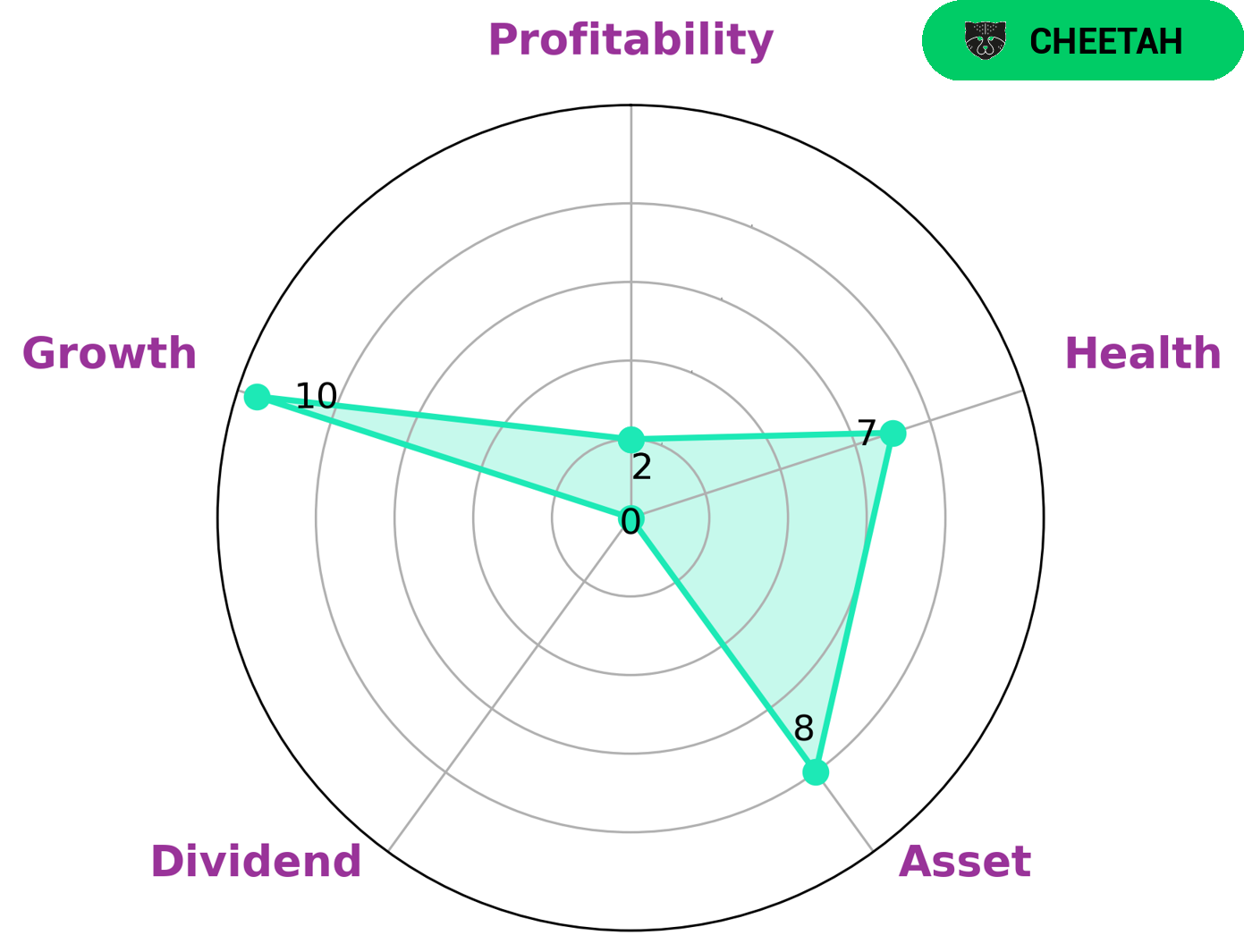

At GoodWhale, we examined TOAST‘s fundamentals and found that the company is classified as a ‘cheetah’, a type of company with high revenue or earnings growth but lower profitability and considered less stable. Looking at their Star Chart, it is evident that TOAST is strong in asset, growth, and weak in dividend and profitability. Furthermore, TOAST has a high health score of 7/10 with regard to its cashflows and debt, indicating that it is capable to safely ride out any crisis without the risk of bankruptcy. Given these characteristics, investors who are looking for high-growth potential and are willing to take on the risks associated with such opportunities may find TOAST’s profile appealing. On the other hand, those seeking long-term stability and consistent returns may prefer to look elsewhere. More…

Peers

In the market for point-of-sale (POS) systems, there is intense competition among a few major players. Toast Inc, GreenBox POS, Rs2 Software PLC, and Hank Payments Corp are all vying for a share of the market. All of these companies offer POS systems that are feature-rich and competitively priced.

– GreenBox POS ($NASDAQ:GBOX)

PLC is a publicly traded company with a market capitalization of 266.3 million as of 2022. It has a return on equity of 6.98%. PLC is engaged in the development, manufacture and sale of software products and services. The company’s products and services are used by businesses and organizations of all sizes, in a variety of industries, including healthcare, financial services, manufacturing, retail, and education.

– Rs2 Software PLC ($LTS:0MVH)

Hank Payments Corp is a publicly traded company that provides mobile payment solutions. The company has a market capitalization of 4.02 million as of 2022. Hank Payments Corp’s primary product is Hanko, a mobile payment application that allows users to make payments using their smartphone. Hanko is available for both Android and iOS devices.

Summary

Despite its promising growth over the past few years, the market reacted negatively to the news, resulting in a more than 20% drop in share price. It is advised that investors exercise caution before considering investing in this stock until more information is available and a clear trend can be identified. Analysts monitoring TOAST should pay attention to any further developments and assess the company’s fundamentals to make an informed decision.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Investing Everyone Can Do.

Investing shouldn’t be exclusive to a select few. We believe everyone should have the opportunity to grow their wealth. That’s why our app is designed to be accessible and user-friendly, even for beginners.