RealReal Maintains Buy Rating Despite Tough Economic Climate, Expands Customer Base

June 15, 2023

☀️Trending News

REALREAL ($NASDAQ:REAL): The RealReal is a unique online marketplace that offers customers authenticated luxury consignment items. They strive to provide customers with access to brands they know and love, while also offering them the opportunity to buy and sell pre-loved items. The company has been a leader in the industry since its inception, and recently received a ‘Buy’ rating from a financial analyst. Despite a tough economic climate, The RealReal continues to expand its customer base. This is largely attributed to their expansive selection of luxury brands, as well as an effort to increase their global reach. Additionally, the company has implemented several initiatives designed to enhance customer experience. These include improved delivery times, a loyalty program, and increased customer service. The RealReal has also identified opportunities to expand in other areas. For instance, they have launched a new personal styling service, as well as an interior design consultation program.

In addition, they have improved their online presence, which has allowed them to reach an even wider audience. Overall, The RealReal’s resilient customer base and proactive strategy make it a great investment opportunity for those looking to diversify their portfolios.

Share Price

On Wednesday, the stock opened at $1.8 and closed at $1.8, up by 1.2% from its previous closing price of $1.7. This is a testament to the company’s strong performance and its ability to expand its customer base even in uncertain times. REALREAL has been successful in retaining and growing its customer base by adapting to the changing market conditions. This can be attributed to their innovative strategies that focus on customer service, convenience, and affordability.

In addition, they have also focused on developing new products and services to keep their customers engaged. This has allowed them to remain competitive and ensure they remain profitable in the face of tough economic conditions. RealReal_Maintains_Buy_Rating_Despite_Tough_Economic_Climate_Expands_Customer_Base”>Live Quote…

About the Company

Income Snapshot

Below shows the total revenue, net income and net margin for Realreal. RealReal_Maintains_Buy_Rating_Despite_Tough_Economic_Climate_Expands_Customer_Base”>More…

| Total Revenues | Net Income | Net Margin |

| 598.7 | -221.53 | -33.3% |

Cash Flow Snapshot

Below shows the cash from operations, investing and financing for Realreal. RealReal_Maintains_Buy_Rating_Despite_Tough_Economic_Climate_Expands_Customer_Base”>More…

| Operations | Investing | Financing |

| -72.64 | -44.4 | 3.17 |

Balance Sheet Snapshot

Below shows the total assets, liabilities and book value per share for Realreal. RealReal_Maintains_Buy_Rating_Despite_Tough_Economic_Climate_Expands_Customer_Base”>More…

| Total Assets | Total Liabilities | Book Value Per Share |

| 511.75 | 755.27 | -2.43 |

Key Ratios Snapshot

Some of the financial key ratios for Realreal are shown below. RealReal_Maintains_Buy_Rating_Despite_Tough_Economic_Climate_Expands_Customer_Base”>More…

| 3Y Rev Growth | 3Y Operating Profit Growth | Operating Margin |

| 22.5% | – | -35.2% |

| FCF Margin | ROE | ROA |

| -19.5% | 63.7% | -25.7% |

Analysis

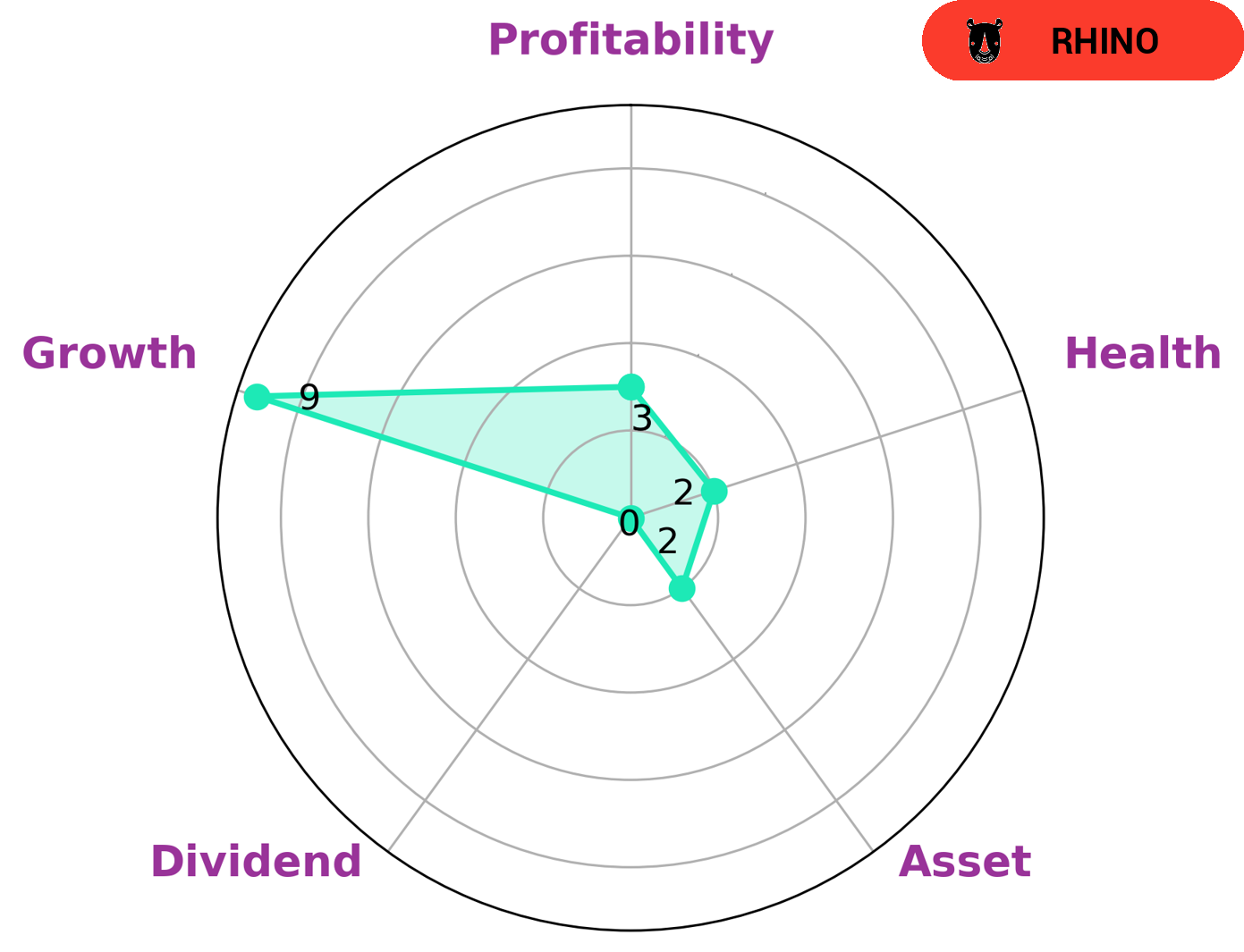

At GoodWhale, we completed an analysis of REALREAL’s fundamentals. Our Star Chart classified REALREAL as a ‘cheetah’; a type of company that achieved high revenue or earnings growth but is considered less stable due to lower profitability. We suspect that investors who prioritize growth and are willing to accept the greater risk associated with such companies would be interested in REALREAL. The analysis also highlighted that REALREAL is strong in growth and weak in asset, dividend, and profitability. Additionally, its health score of 2/10 with regard to cashflows and debt indicates that it is less likely to pay off debt and fund future operations. RealReal_Maintains_Buy_Rating_Despite_Tough_Economic_Climate_Expands_Customer_Base”>More…

Peers

The RealReal Inc is a luxury consignment company that sells pre-owned designer items. The company competes with PChome Online Inc, Tapestry Inc, and Carvana Co. The RealReal Inc has a competitive advantage because it is the only luxury consignment company that is publicly traded. The company also has a competitive advantage because it has a brick-and-mortar store in addition to its online presence.

– PChome Online Inc ($TPEX:8044)

PChome Online Inc is a Taiwanese company that provides an online marketplace for consumers in Taiwan. The company has a market cap of 5.88B as of 2022 and a Return on Equity of 3.34%. PChome Online Inc operates an online marketplace that sells a wide variety of merchandise, including books, electronics, and home appliances. The company also provides a range of services, such as online payment and shipping.

– Tapestry Inc ($NYSE:TPR)

Tapestry, Inc., is an American luxury fashion holding company based in New York City. It was founded in 2016 as a result of the merger of Coach, Inc. and Kate Spade & Company. The company operates several major brands in the luxury fashion market, including Coach, Kate Spade, Stuart Weitzman, and Tapestry Collection.

Tapestry’s market capitalization is $7.57 billion as of 2022. The company’s return on equity is 28.67%. Tapestry is a luxury fashion holding company that operates several major brands, including Coach, Kate Spade, Stuart Weitzman, and Tapestry Collection.

– Carvana Co ($NYSE:CVNA)

Carvana Co is a company that operates an e-commerce platform for selling used cars. The company has a market cap of 1.94B as of 2022 and a return on equity of -183.76%. Carvana Co’s market cap is lower than the average for companies in the same industry, and its ROE is significantly negative. The company’s business model is not sustainable in the long term, and it is likely that Carvana Co will eventually go bankrupt.

Summary

It boasts an expanding customer base, offering authenticated items from top designer brands. Its success is also driven by a strong focus on sustainable practices. The RealReal‘s long-term prospects are promising, and analysts are currently recommending it a ‘Buy’ due to its resilient and expanding customer base. The company has a strong balance sheet with a healthy cash position and low debt, making it well-positioned to capitalize on the growing resale market.

Related Posts

Recent Posts

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Investing Everyone Can Do.

Investing shouldn’t be exclusive to a select few. We believe everyone should have the opportunity to grow their wealth. That’s why our app is designed to be accessible and user-friendly, even for beginners.