Ferroglobe Plc Intrinsic Value – Ferroglobe PLC: An Undervalued Opportunity to Benefit From

May 20, 2023

Trending News ☀️

Ferroglobe ($NASDAQ:GSM) PLC is an undervalued opportunity to benefit from. It also produces manganese alloys for the production of aluminum and steel. The company’s valuation is too attractive to pass up, making it an ideal investment choice for those looking to benefit from a potential upside. Ferroglobe PLC‘s stock has been overlooked by most analysts in recent months due to its relatively low price compared to its peers in the industry, however, this presents investors with a unique opportunity to purchase shares at a discount. The company’s operations are focused on the manufacturing of its products and its key markets are North America, Europe and Asia.

Ferroglobe PLC also has a strong balance sheet that should allow it to withstand any potential downturns in the markets. With its strong fundamentals and potential for growth, Ferroglobe PLC is an undervalued opportunity that savvy investors should not overlook. Investing in the company could provide investors with both short-term profits and long-term gains, helping them realize their financial goals.

Price History

On Friday, FERROGLOBE PLC stock opened at $4.6 and closed at $4.6, representing a 2.2% increase from its last closing price. This signifies that investors are paying increasing attention to the potential growth in this sector. FERROGLOBE PLC is one of the largest producers of speciality materials and ferroalloys in the world with a presence in Europe, North America, and Asia. It primarily produces manganese-based alloys, silicon-based alloys, and other ferroalloys.

It also produces steel and other alloy products. Its products are used in various industries, including automotive, energy, infrastructure, and telecommunications. Given its strong balance sheet, integrated operations, and global reach, FERROGLOBE PLC is well-positioned to benefit from the growth of the steel and specialty metals industry. Live Quote…

About the Company

Income Snapshot

Below shows the total revenue, net income and net margin for Ferroglobe Plc. More…

| Total Revenues | Net Income | Net Margin |

| 2.28k | 310.14 | 15.6% |

Cash Flow Snapshot

Below shows the cash from operations, investing and financing for Ferroglobe Plc. More…

| Operations | Investing | Financing |

| 473.89 | -59.94 | -239.27 |

Balance Sheet Snapshot

Below shows the total assets, liabilities and book value per share for Ferroglobe Plc. More…

| Total Assets | Total Liabilities | Book Value Per Share |

| 1.91k | 1.25k | 3.47 |

Key Ratios Snapshot

Some of the financial key ratios for Ferroglobe Plc are shown below. More…

| 3Y Rev Growth | 3Y Operating Profit Growth | Operating Margin |

| 15.6% | -39.1% | 21.2% |

| FCF Margin | ROE | ROA |

| 18.0% | 46.4% | 15.8% |

Analysis – Ferroglobe Plc Intrinsic Value

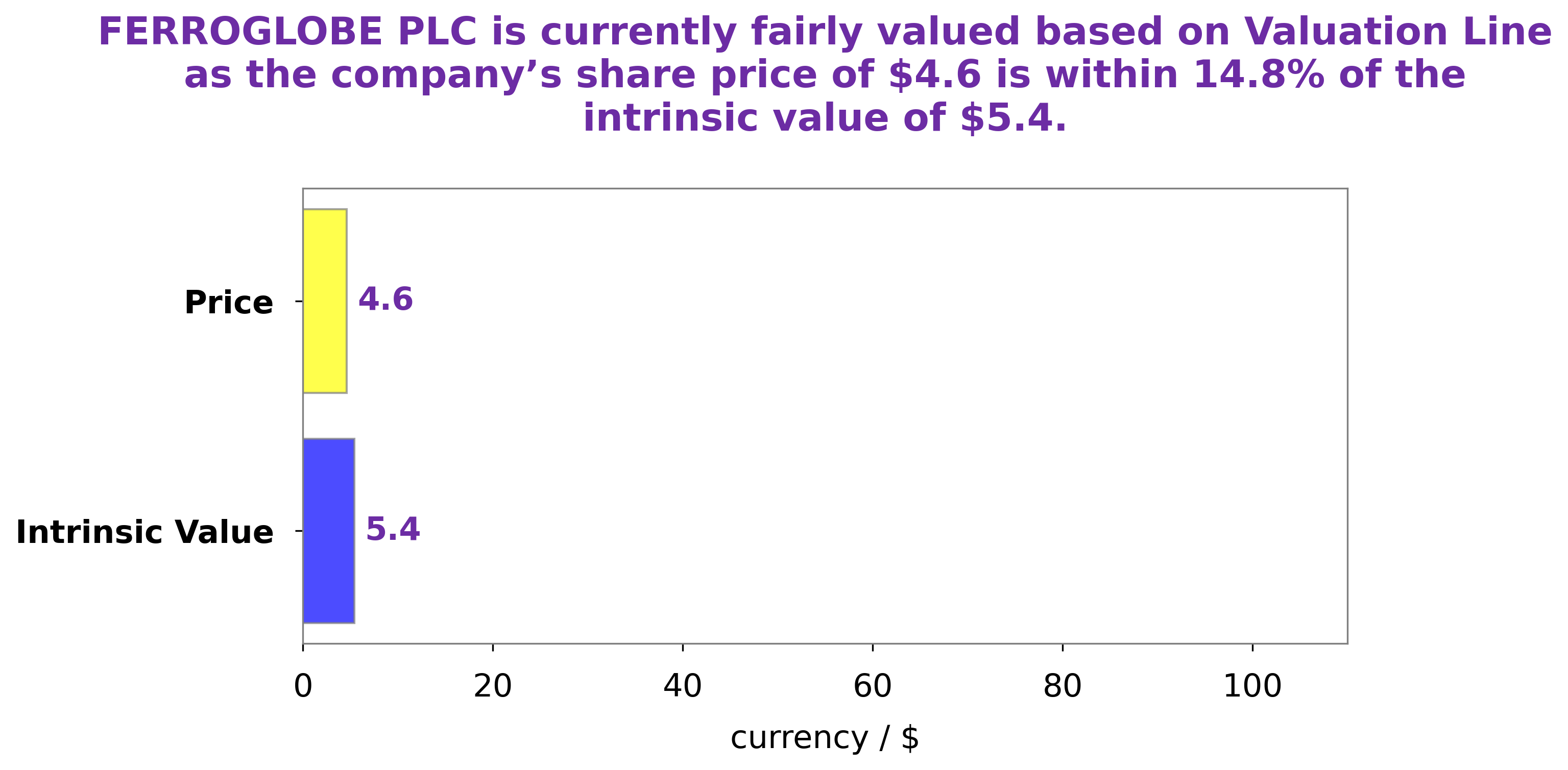

At GoodWhale, we have taken an in-depth look at the fundamentals of FERROGLOBE PLC and our proprietary Valuation Line has determined that the fair value of the company’s share is around $5.4. Currently, FERROGLOBE PLC shares are trading at $4.6, which means the stock is undervalued by 14.3%. As such, we believe that FERROGLOBE PLC represents a strong investment opportunity for those looking to capitalize on an undervalued stock. More…

Peers

Ferroglobe PLC is one of the leading players in the ferroalloys industry, facing stiff competition from established players such as Eramet SA, Hangzhou Yitong New Material Co Ltd, and Sichuan Hongda Co Ltd. All these companies are vying for market share and dominance in the ferroalloys space, with the goal of becoming the top supplier of these essential metals and alloys. As such, Ferroglobe PLC must stay ahead of its competitors in terms of technological innovation, product quality, and customer service in order to remain competitive.

– Eramet SA ($LTS:0MGV)

Eramet SA is a French mining and metallurgical company with interests in the extraction, production and processing of manganese and nickel ore. The company has a market capitalization of 2.69 billion Euros as of 2023 and a Return on Equity of 80.99%. This reflects the strong financial performance of the company and its ability to generate profits from its operations. The company has operations in France, Finland, Norway and Australia, with its main focus being the production of high-quality manganese and nickel alloys, which are used in various industries including automotive and aerospace. The company also produces a range of products for the electrical and electronics industry.

– Hangzhou Yitong New Material Co Ltd ($SZSE:300930)

Hangzhou Yitong New Material Co Ltd is a Chinese industrial enterprise that specializes in the production of polymer materials. The company has a market capitalization of 3.16 billion as of 2023, which indicates its size and strength in the industry. Furthermore, its return on equity (ROE) stands at 7.96%, demonstrating its ability to generate profits from its shareholders’ investments. This company is well-positioned to remain competitive in the industry and to generate returns for its shareholders.

– Sichuan Hongda Co Ltd ($SHSE:600331)

S i c h u a n H o n g d a C o L t d i s a C h i n e s e c h e m i c a l c o m p a n y f o c u s e d o n t h e p r o d u c t i o n a n d s a l e o f c h e m i c a l p r o d u c t s , i n c l u d i n g a m m o n i u m s u l f a t e , c a l c i u m c h l o r i d e , a n d m a g n e s i u m h y d r o x i d e . T h e c o m p a n y h a s a m a r k e t c a p o f 7 . 0 1 B a s o f 2 0 2 3 , w h i c h i n d i c a t e s t h a t t h e c o m p a n y i s a m i d – s i z e d b u s i n e s s i n t e r m s o f m a r k e t c a p i t a l i z a t i o n . A d d i t i o n a l l y , t h e c o m p a n y h a s a n i m p r e s s i v e R e t u r n o n E q u i t y o f 2 4 . 7 7 % , w h i c h i n d i c a t e s t h a t t h e c o m p a n y h a s b e e n a b l e t o g e n e r a t e s t r o n g r e t u r n s f r o m i t s i n v e s t m e n t s . T h i s s u g g e s t s t h a t S i c h u a n H o n g d a C o L t d i s a s u c c e s s f u l a n d w e l l – m a n a g e d b u s i n e s s

Summary

FERROGLOBE PLC is an international producer of silicon-based and specialty metals with a focus on the electric arc furnace market. The company’s current valuation is well below its intrinsic value, presenting a compelling buying opportunity for investors. With a strong balance sheet, solid cash flow, and a track record of delivering shareholder value, the stock appears to be undervalued. Furthermore, a growing demand for electric arc furnace products, improved production efficiencies, and cost-reduction measures should result in improved margins for the company.

Additionally, FERROGLOBE has a diversified customer base and an experienced management team that should ensure long-term growth. With its attractive valuation, FERROGLOBE appears to be an attractive investment for those looking for a solid return on investment.

Related Posts

Recent Posts

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Investing Everyone Can Do.

Investing shouldn’t be exclusive to a select few. We believe everyone should have the opportunity to grow their wealth. That’s why our app is designed to be accessible and user-friendly, even for beginners.