Amazon’s ‘Lucky’ Financing Before Dot-Com Crash Raises Questions About Its Resilience

February 22, 2023

Trending News 🌥️

AMAZON.COM ($NASDAQ:AMZN): Sumitomo Realty & Development have announced a major venture into the UK real estate market, focusing on the development of environmentally conscious mass timber properties. This joint venture, between Sumitomo Forestry and various other partners, is set to revolutionize the construction industry in Europe, creating properties that are not only sustainable and durable, but also have low carbon footprints. The use of mass timber in construction is becoming increasingly popular and Sumitomo are looking to take full advantage of this trend. Their properties will be designed and built with their expertise in wood, combined with the latest technology and sustainable practices.

This means that they will create buildings with enhanced energy efficiency, strength, and durability, as well as ensuring minimal environmental impact. Overall, this new venture marks an exciting shift in the UK real estate market, as Sumitomo Realty & Development look to make environmentally friendly mass timber properties the norm and pave the way for a greener future. With their expertise in wood, sustainability and innovative building practices, it looks like Sumitomo will be leading the way for sustainable real estate in Europe.

Share Price

Sumitomo Realty & Development has recently launched a full-scale venture into the UK real estate market with a focus on environmentally conscious properties constructed using mass timber. The move is seen as a positive step in the company’s commitment to reducing their environmental footprint and creating a more sustainable future for development. The announcement came Wednesday after an initial launch of the venture, signaling its focus on creating mass timber homes with a lower environmental impact than traditional construction materials. As such, these properties will be highly sought after in what is already one of the world’s most competitive real estate markets.

Sumitomo’s stock opened slightly higher Wednesday at JP¥3126.0, but closed down 1.5% at JP¥3081.0 versus the prior closing price of 3129.0. Despite the dip, this new venture seems poised to further elevate Sumitomo’s reputation as a leader in environmentally conscious property development in the UK. Live Quote…

About the Company

Income Snapshot

Below shows the total revenue, net income and net margin for Amazon.com. More…

| Total Revenues | Net Income | Net Margin |

| 513.98k | -2.72k | 1.4% |

Cash Flow Snapshot

Below shows the cash from operations, investing and financing for Amazon.com. More…

| Operations | Investing | Financing |

| 46.75k | -37.6k | 9.72k |

Balance Sheet Snapshot

Below shows the total assets, liabilities and book value per share for Amazon.com. More…

| Total Assets | Total Liabilities | Book Value Per Share |

| 462.68k | 316.63k | 14.25 |

Key Ratios Snapshot

Some of the financial key ratios for Amazon.com are shown below. More…

| 3Y Rev Growth | 3Y Operating Profit Growth | Operating Margin |

| 22.4% | -5.6% | -0.7% |

| FCF Margin | ROE | ROA |

| -3.3% | -1.6% | -0.5% |

Analysis

At GoodWhale, we have conducted an in-depth analysis of the financials of SUMITOMO REALTY & DEVELOPMENT. According to our proprietary Valuation Line, we have calculated the fair value of SUMITOMO REALTY & DEVELOPMENT share to be around JP¥3848.0. However, the stock is currently being traded at JP¥3081.0, a price that is significantly undervalued by 19.9%. This presents an opportunity for investors to purchase the stock at a much lower price than its fair value. More…

Summary

Sumitomo Realty & Development, a Japanese-based real estate corporation, has announced the establishment of a full-scale venture into the UK property market, with a focus on environmentally conscious investments. This venture will focus on constructing mass timber-framed properties and buildings across the UK, with a focus on utilizing the latest environmental technologies. Investment analysis shows that this venture is expected to bring significant returns for the company, as timber-framed construction is becoming increasingly popular with property buyers.

Additionally, Sumitomo’s focus on sustainability and high-performing green technologies could give them an edge over the competition. Sumitomo’s venture into the UK market is expected to be a success, and could lead to further opportunities in other markets.

Trending News 🌥️

It is a milestone moment for Hangzhou Tigermed Consulting Co., Ltd. (300347) as its stock price has reached 300347, signifying a major success for the company. This breakthrough marks the highest that their shares have traded at and has been welcomed by investors and analysts alike. The remarkable climb has been attributed to a number of factors, such as the company’s continued innovation efforts, its reputation for quality, and its increasing presence in the medical and healthcare industry. Hangzhou Tigermed Consulting Co., Ltd. is a leading provider of medical and healthcare consulting and management services in China.

By leveraging its expertise in the healthcare sector, the company has managed to stay ahead of industry trends, positioning itself as one of the top players in the market. Impressive growth in revenue and profits have also contributed to the strong performance of Hangzhou Tigermed’s stock in recent months. The rising stock price of Hangzhou Tigermed Consulting Co., Ltd. is a testament to the company’s consistent and sustained growth over the years. Going forward, investors can expect the firm to continue to demonstrate exemplary performance in the future, with the potential to reach even higher milestones.

Stock Price

Thursday was a difficult day for HANGZHOU TIGERMED CONSULTING CO., LTD as their stock price reached 300347. The stock opened CNY116.6 in the morning and by the end of the day had decreased to CNY114.5, a 1.5% drop from their closing price of 116.2 the day before. This is a significant decrease and traders will be closely monitoring the stock in the coming days to determine if any more losses will be seen. Investors in the company are likely to be concerned about the sudden fall. Live Quote…

Analysis

At GoodWhale, we have conducted a thorough analysis of the financials of HANGZHOU TIGERMED CONSULTING to determine its fair value. Our proprietary Valuation Line has calculated the fair value of HANGZHOU TIGERMED CONSULTING share to be around CNY196.6. Currently, the stock is traded at CNY114.5, meaning it is undervalued by 41.8%. This presents a great opportunity for investors who wish to capitalize on the gap in price and acquire HANGZHOU TIGERMED CONSULTING shares at a discounted rate. More…

Summary

HANGZHOU TIGERMED CONSULTING CO., LTD recently reached a new milestone in its stock price, surpassing 300347. Analysts have noted strong performance in the company’s core markets, driven by its recent expansion initiatives and strategic partnerships. In the short run, analysts predict the stock will remain volatile with potential for further increases in value. Long-term investments in the company appear promising as HANGZHOU TIGERMED CONSULTING is well-positioned to benefit from the emergence of new opportunities in its core markets.

Investors should watch for continued development of the company’s portfolio and look for strategic investments in complementary industries. Analysts are also recommending research into potential partnerships to help increase the visibility and reach of HANGZHOU TIGERMED CONSULTING products and services. With the new milestone in its stock price, now is an opportune time to consider investing in HANGZHOU TIGERMED CONSULTING.

Trending News 🌥️

China Galaxy Securities, a leading Chinese financial services provider, has recently announced the successful issuance of 4 billion yuan in corporate bonds. The bonds are expected to be used to finance the company’s upcoming expansion into smaller cities and towns across China. The bond issuance is part of the company’s ongoing efforts to strengthen its financial standing and ensure continued profitable growth. This news marks a major milestone for China Galaxy Securities, as the successful bond issuance is a testament to the company’s financial strength and market position. The 4 billion yuan raised is expected to be used to expand the company’s operations, offering investment and trading services in smaller cities and towns across China. This move is part of their long-term strategy for growth and market penetration.

The bond issue reflects the confidence that investors have in the company and their willingness to invest in the continued growth of China Galaxy Securities. The company has been able to secure this large sum of capital with the assurance that it will be used to drive future profits and secure sustained growth. Overall, China Galaxy Securities has achieved a significant milestone with the successful issuance of 4 billion yuan in corporate bonds. This issuance reflects both investor confidence in the company, as well as China Galaxy Securities’ commitment to long-term growth and expansion.

Market Price

On Friday, China Galaxy Securities Co., Ltd. The news has so far received positive media coverage, and the stock opened and closed at HK$4.0 on Friday, up by 0.8% from previous closing price of HK$3.9. The successful fundraising paves the way for CHINA GALAXY SECURITIES to expand its business operations, increase market presence and strengthen its financial footing through greater resources. This investment will further contribute to the development of the Chinese financial sector, while also providing different types of investors with more investment options. Live Quote…

Analysis

GoodWhale has performed an analysis of CHINA GALAXY SECURITIES’ financials and found that the company has an intermediate health score of 4/10 with regards to its cashflows and debt. This suggests that CHINA GALAXY SECURITIES is likely to pay off debt and fund future operations. Furthermore, CHINA GALAXY SECURITIES is classified as a ‘cheetah’ – a type of company that achieved high revenue or earnings growth but is considered less stable due to lower profitability. In terms of investor appeal, CHINA GALAXY SECURITIES is strong in dividend and growth, but weak in asset and profitability. Given these findings, investors who are drawn to higher risk-high reward investments may be interested in CHINA GALAXY SECURITIES as a potential option. They should use this analysis to further scrutinize the company and assess whether it is a suitable investment for their portfolio. More…

Summary

China Galaxy Securities has successfully raised 4 billion yuan via the issuance of corporate bonds. This successful issuance suggests that investors have confidence in the company and its prospects for future growth. Analysis of China Galaxy Securities’ past performance indicates that its annual revenue has been steadily rising, while its net income and cash flow metrics have remained healthy. Overall, the positive market response to the issuance demonstrates that China Galaxy Securities is an attractive investment opportunity.

Trending News 🌥️

InvestorsObserver recently rated H World Group Ltd near the middle of its industry group, with an overall rating of 54. So, should H World Group Ltd be a part of your portfolio as of Friday? Despite the middle-of-the-road score from InvestorsObserver, there are a few factors to consider when thinking about adding H World Group Ltd to your portfolio. Firstly, it is important to assess the fundamentals of the company. H World Group Ltd has strong financials and a solid outlook, making it a worthy contender for investors.

Additionally, H World Group Ltd has seen consistent growth throughout the last few years, further strengthening the case for long-term investors to consider adding them to their portfolios. Furthermore, another factor to consider is the company’s dividend and share repurchase policies. H World Group Ltd has an attractive dividend policy in place which provides regular payments to shareholders, as well as a share repurchase program which helps to bolster the stock price. Finally, it is worth looking at potential risks associated with H World Group Ltd before making a decision. It is important to understand the risks associated with any stock purchase and make an informed decision based on the company’s fundamentals, financials and outlook. Considering all the above mentioned factors, H World Group Ltd may be a good addition to your portfolio on Friday. Investors should make sure to do their research and understand the associated risks before making any final decision.

Stock Price

On Monday, InvestorsObserver announced their rate of 54 for H World Group Ltd stock. This international conglomerate saw its stock open at HK$39.3 and close at HK$39.9, down a slight 0.7% from its previous closing price of 40.2. This rate has caused some investors to question whether it is worth adding H World to their portfolio. The answer must include an evaluation of each individual investor’s goals and risk preferences. Therefore, investors who are looking for a safe stock with low volatility may not find H World to be a suitable option.

On the other hand, those who are willing to take on more risk will likely find greater potential for growth with H World. Overall, adding H World to one’s portfolio depends on individual investment objectives and risk tolerance. InvestorsObserver’s rating of 54 should only be taken into account with other factors such as the company’s performance, its current and expected future value, and the volatility of the stock. With careful consideration of these factors, investors will be able to determine whether H World is right for them. Live Quote…

Analysis

At GoodWhale, we have carefully examined the fundamentals of H WORLD and found it to have a compelling overall story. Its intrinsic value, as calculated by our proprietary Valuation Line, is around HK$35.1. This suggests that the stock is currently trading at a fair price of HK$39.9, overvalued by 13.6%. H WORLD is focused on providing a comprehensive range of consumer products and services in the Asia Pacific region. It has established relationships with many leading international brands and provides a wide range of services, including retailing, distribution, logistics, marketing, and other value-added services. The company is well-positioned to benefit from the increasing consumer demand in the Asia Pacific region, with a robust portfolio of products and services that continue to address changing consumer needs. Its competitive pricing strategy has enabled it to gain market share across the region and its financial position has remained strong throughout the past few years. Overall, our analysis suggests that H WORLD remains an attractive investment option for those who seek to benefit from its strong fundamentals and potential for future growth. More…

Summary

H World Group Ltd. has recently been rated by InvestorsObserver with a score of 54. This rating indicates that it is a company with a moderate level of risk, making it a potentially viable addition to an investor’s portfolio. The company has performed relatively well on the stock market over the past few years and offers attractive dividend payments. It is important to consider the company’s financials, including its balance sheet, income statement, and cash flow statements, to ensure that it is in good standing and able to sustain its current level of operations.

Furthermore, investors should pay careful attention to the company’s management and track record of strategic decision-making when considering an investment in H WORLD. Overall, there are a variety of factors to consider when investing in H WORLD and investors should take the time to thoroughly assess the company before committing funds.

Trending News 🌥️

Analysts have remained optimistic about Evolv Technologies Holdings Inc. despite a recent drop in the company’s stock price. Evolv Technologies is a technology solutions provider that focuses on helping organizations innovate through business solutions and technology advancements. Analysts remain optimistic about the future of Evolv Technologies, citing their impressive portfolio of solutions and services as well as their strong customer base as reasons for their confidence. Despite the decrease in the company’s stock price, analysts remain confident that the price will soon recover and that the company will continue to grow in the coming months. They also offer investors advice on how to manage their portfolios in order to take advantage of the current market conditions and make the most out of their investments. Evolv Technologies is committed to providing innovative solutions and services to its customers in order to help them achieve their goals.

The company has a history of delivering cutting-edge products and services that enable organizations to stay ahead of the competition. With its commitment to innovation, it should continue to see growth in the coming months. Overall, analysts remain positive about Evolv Technologies despite the recent drop in its stock price. They are confident that the share price will eventually recover and that the company will continue to innovate and grow in the future. Investors should take this opportunity to assess their portfolios and make sure they are taking advantage of these current market conditions to maximize their returns.

Market Price

Analysts remain optimistic about Evolv Technologies Holdings Inc. stock despite a slight drop in the company’s closing price on Wednesday. The stock opened at $3.0 and closed at the same price, representing a 2.0% decline from the prior closing price of 3.0. Despite this small drop, media coverage of the company has been largely positive thus far.

Analysts point to the company’s innovative technology as well as strong corporate identity and history as primary indicators of future success. Overall, analysts remain generally bullish about the stock. Live Quote…

Analysis

As GoodWhale, we have conducted a thorough analysis of EVOLV TECHNOLOGIES to determine its Risk Rating. We have assessed both the business and financial aspects, and have determined that EVOLV TECHNOLOGIES represents a medium risk investment. We recommend that our users take the time to further investigate EVOLV TECHNOLOGIES. To do this, sign up for a free account with us and explore the potential risks in both the financial and business areas. Our comprehensive evaluation can help give you a better understanding of EVOLV TECHNOLOGIES and potential risks it might bring. More…

Summary

Evolv Technologies Holdings Inc. (EVLV) stock has seen a drop in closing price recently, but analysts remain optimistic about the future of the company. Media coverage has been largely positive, with many praising the company’s outlook and potential. Analysts believe that while the current market environment might be challenging, there are plenty of opportunities down the line for EVLV to capitalize on. They point to the company’s technology and capabilities as major strengths.

Additionally, the company is well-positioned to benefit from the continued surge in technological advances in the near future. Overall, analysts remain bullish on EVLV and its potential to deliver strong returns for investors over the long run.

Trending News 🌥️

Australian mining company Rumble Resources has achieved a major breakthrough in its search for profitable mineral deposits, with the discovery of a high-grade zinc-lead ore deposit in the Tonka-Navajoh prospect in Earaheedy. This prospect is estimated to contain an estimated grade of over 20% zinc-lead and holds immense potential for the company. The discovery is considered to be a significant step forward for Rumble Resources, as it assists in their goal of creating a long-term sustainable mining operation that is capable of supplying the growing zinc-lead industry. The company is confident that their new ore discovery will provide the necessary boost to their operations and allow them to maximize the potential of this promising mineral deposit.

This will give Rumble Resources an advantage over other zinc-lead producers and it should be able to capitalize on this newly discovered resource. Overall, the new ore discovery from Rumble Resources is a major accomplishment for the company and will greatly benefit their operation going forward. With this find, they can now look forward to increased profitability and sustainability in the zinc-lead industry for many years to come.

Market Price

RUMBLE RESOURCES has struck high-grade zinc and lead at their Tonka-Navajoh Prospect at Earaheedy, and the media has mostly had a positive response. On Thursday, the stock opened at AU$0.2 and closed at the same rate, indicating a 7.3% increase from the previous day’s close of 0.2. This news has further bolstered the confidence of shareholders in RUMBLE RESOURCES, who are confident in the company’s ability to deliver returns. Live Quote…

Analysis

At GoodWhale, we have successfully concluded an analysis of RUMBLE RESOURCES’ financials. Through our proprietary Valuation Line, we determined that the fair value of a RUMBLE RESOURCES share was approximately AU$0.3. Unsurprisingly, we have observed that the stock is currently trading at AU$0.2, which is a significant 39.2% undervaluation of the RUMBLE RESOURCES. This offers investors a great potential upside if they decide to act on the discrepancy between our valuation and the current trading price. More…

Summary

Rumble Resources has been making headlines within the mining industry, as the exploration and development company has recently discovered high-grade zinc-lead from its Tonka-Navajoh Prospect at Earaheedy. This news has met with positive reactions from the industry, and has been reflected in the company’s stock price, which saw an increase on the same day. Investing in Rumble Resources could prove to be a wise choice, as the company is well-positioned to benefit from the current favorable market conditions for zinc-lead, with potential for further discoveries in the future.

Trending News 🌥️

Investing in North European Oil Royalty Trust (NEORT) stock could be a good idea for Tuesday. This oil trust holds royalties from some of the largest oil and gas producing regions in Europe. The trust has been growing steadily since its initial offering and has seen a recent surge as demand for energy increases. The trust offers investors a unique way to invest in the energy industry without the direct ownership of shares. The trust also offers investors a steady stream of income from the trust’s dividends. The trust is managed by a professional team of experts who focus on maximizing returns and minimizing risk. The trust invests primarily in oil and gas properties located in North European countries, such as Norway, Denmark, Sweden and Finland. This geographical focus can provide investors with a degree of familiarity and diversity, as well as the security of knowing that their investments are located in relatively stable political and economic environments. For Tuesday, investors should consider the current market conditions before deciding to buy NEORT stock. As demand for energy continues to grow and the global economy remains strong, the trust has the potential to generate solid returns.

Additionally, investors should assess their own financial goals before investing in the stock. In doing so, they can align their investment choices with their own financial objectives and risk tolerance levels.

Stock Price

The media sentiment has been largely positive when it comes to North European Oil Royalty Trust (NORTH EUROPEAN OIL ROYALTY TRUST) stock. This increase is a promising sign for potential investors, as it could indicate that the stock could soon begin to rise. Though this is an encouraging sign, potential investors must take the current market conditions into account before investing in the stock. With the uncertainty of the market, investors must be aware of the risks associated with investing in NORTH EUROPEAN OIL ROYALTY TRUST stock, and weigh the potential reward to decide if now is the right time to buy. Live Quote…

Analysis

GoodWhale has prepared an analysis of NORTH EUROPEAN OIL ROYALTY TRUST’s financials. The Star Chart shows that NORTH EUROPEAN OIL ROYALTY TRUST’s strong financial position, with excellent scores in asset, dividend, growth and profitability. In particular, it has a high health score of 9/10 with regard to cashflows and debt, indicating its ability to pay off debt and fund future operations. NORTH EUROPEAN OIL ROYALTY TRUST is also classified as a ‘gorilla’, meaning that it has achieved stable and high revenue or earnings growth due to its strong competitive advantage. With such a strong financial position, the company could be an attractive option for risk-averse investors who are seeking consistent dividend payments. On the other hand, investors interested in capital appreciation might be attracted by the growth potential of this company. More…

Summary

North European Oil Royalty Trust (NOR) has seen a surge in interest from investors in recent weeks. Media sentiment has been mostly positive, with analysts recommending that now could be an opportune moment to purchase NOR stock. Investors should consider the current oil market trends, company performance, financial reports, and macroeconomic factors. Specifically, the outlook for oil prices, geopolitical risks, and potential supply disruptions should all be taken into account when making an investment decision.

In addition, investors should explore the advantages and drawbacks to NOR’s royalty structure and its potential dividend income. Overall, a comprehensive research and analysis of NOR stock is essential to determine whether now is the right time to make an investment.

Trending News 🌥️

HC Wainwright has kept their Buy Rating on Cara Therapeutics despite revising their price target from $30 to $25. Cara Therapeutics is a clinical-stage biopharmaceutical company focused on developing and commercializing new chemical entities designed to alleviate pain and pruritus without causing many of the undesirable side effects associated with opioid-based therapies. The reduction in the price target is primarily attributed to the recent financing event, which drastically increased the number of outstanding shares.

Despite this, HC Wainwright believes that Cara Therapeutics is well-positioned to further advance its product portfolio and attract a significant market share. Investors may want to take a closer look at the stock given its strong fundamentals and potential future growth drivers.

Price History

On Tuesday, HC Wainwright analysts maintained their Buy rating on Cara Therapeutics stock, while adjusting their price target to $25. The day saw the stock open at $11.1, before closing at $10.7, representing a 4.0% decrease from its prior closing price of $11.1. This buy rating from HC Wainwright comes at a time when Cara Therapeutics is currently undergoing a period of growth and development, as it strives to bring innovative therapies to market for the potential treatment of pain. Live Quote…

Analysis

GoodWhale recently conducted an analysis of CARA THERAPEUTICS’ financials using our proprietary Star Chart. The chart found that CARA THERAPEUTICS is strong in terms of assets, growth and medium in profitability. Unfortunately, the chart also revealed that CARA THERAPEUTICS is weak in terms of dividends. CARA THERAPEUTICS also has an intermediate health score of 4/10 with regard to its cashflows and debt, indicating that it is likely to be able to sustain future operations even in times of crisis. According to our classification system, CARA THERAPEUTICS is classified as a ‘rhino’, meaning that the company has achieved moderate revenue or earnings growth. Based on these findings, we think that a wide range of investors may be interested in this company. Among them are income-seeking investors looking for a moderately profitable asset, as well as growth-oriented investors who are looking for strong future growth potential. Furthermore, those investors who are seeking stability in their portfolio may also be drawn to CARA THERAPEUTICS due to its moderate health score. More…

Summary

Despite the lowered rating, analysts still view the stock as an attractive buy opportunity, given its potential for long-term growth. On the same day, however, the stock price decreased, potentially due to concerns about the company’s performance in the near term. Investors should keep an eye out for further developments, as Cara Therapeutics continues to progress in its clinical trials and seek approval for new pharmaceutical products in the future.

Trending News 🌥️

The stock price of Mears Group has recently surpassed its 200-day moving average to reach a new high of $199.83. This is good news for the company and its investors, as the stock price has been steadily increasing for the past few months. The 200-day moving average is an important indicator of a company’s performance and so this milestone is an indication of just how successful Mears Group is. The company is well-known for its range of services, including construction, facilities management and social housing maintenance. Its range of services is highly sought after and therefore the stock price has been steadily increasing in recent months.

The increasing stock price will be welcomed by those who invest in Mears Group, as they can expect to see a return on their investment. This news will also be encouraging to other stakeholders and customers of Mear Group, as it reflects the company’s continued success and growth. Overall, the news that Mears Group’s stock price has exceeded its 200-day moving average and reached a new high of $199.83 is excellent news for all stakeholders and investors. It is a reflection of the company’s excellent services, as well as its sound management and financial decisions.

Stock Price

The price gain of Mears Group stock is reflective of a recent surge in the stock market and the company’s solid performance over the past year. Investors are optimistic about the company’s prospects and have been pushing their stock prices higher. This has caused Mears Group’s stock to outperform the broader market and reach new highs as of Wednesday. Live Quote…

Analysis

At GoodWhale, we have conducted an analysis of MEARS GROUP’s fundamentals. After taking into consideration many factors, such as financial performance, operational metrics, and industry dynamics, we have determined that the intrinsic value of MEARS GROUP’s share should be around £1.9. This calculation has been made with our proprietary Valuation Line. Currently, MEARS GROUP stock is trading at a fair price of £2.1 – a small overvaluation of 11.4%. We believe this is likely due to market sentiment, but investors should still be mindful of the current level of pricing. More…

Summary

Investing in Mears Group has been a profitable endeavor thus far. The company’s stock has recently hit a new high of $199.83, surpassing its 200-day moving average for the first time. This marks an impressive rise of over 40% since the beginning of the year. Analysts recommend continued buying, citing strong demand for Mears Group’s services in their key markets and low-cost, high-value offerings.

Additionally, the company’s market capitalization has grown significantly over the past three years, suggesting that investor confidence is at an all-time high. With an attractive dividend yield and strong execution, Mears Group is an attractive choice for long-term investors.

Trending News 🌥️

The California Public Employees Retirement System (CalPERS) recently announced an investment of $6.97 million in Zai Lab Limited. Zai Lab is an innovative biopharmaceutical company centered on the development and commercialization of innovative treatments to improve patient outcomes in China and other emerging markets. The investment, made by CalPERS’ global private equity program, will provide Zai Lab with the necessary capital and resources to support the research and development of novel treatments and drugs aimed at improving people’s health across the globe. In addition to providing growth capital, CalPERS also holds a stock position in Zai Lab worth $6.97 million. This investment is part of their goal of diversifying their pension fund portfolio and supporting innovative companies like Zai Lab.

Through this partnership, CalPERS hopes to create value for both the company and its shareholders. By investing in Zai Lab, CalPERS is showing its commitment to making a positive impact on global health outcomes. The funds and resources provided by this investment will help Zai Lab to continue its mission of developing treatments and drugs to improve patient outcomes, ultimately benefiting the citizens of California and the world over.

Market Price

On Monday, amidst a sea of negative news, there was a ray of hope for investors in ZAI LAB Limited. The California Public Employees Retirement System (CalPERS) announced it had invested $6.97 million in the company. This resulted in a 7.4% jump from last closing price of HK$29.6 to HK$31.8 when the market closed on Monday. This positive news provided investors with much needed encouragement in the current climate. Live Quote…

Analysis

GoodWhale analyzed ZAI LAB’s wellbeing and our findings showed that it has an intermediate health score of 5/10 based on its cashflows and debt. This indicates that ZAI LAB may be able to safely ride out any crisis without the risk of bankruptcy. Additionally, the Star Chart revealed that ZAI LAB is strong in asset and growth, yet weak in dividend and profitability. This classification places ZAI LAB under ‘cheetah’, a type of company that achieved high revenue or earnings growth but is considered less stable due to lower profitability. As such, this company may be attractive to investors who are willing to take on higher risks in exchange for potentially higher returns. These investors may include those who are looking for potentially higher profits off of short-term investments, as well as those who are looking for capital appreciation over the long-term. More…

Summary

Investors have displayed optimism towards Zai Lab Limited, as the California Public Employees Retirement System recently invested an estimated $6.97 million in the company. Despite current negative news impacting the market, stock prices for the company rose the same day as the investment, indicating that investors are seeing potential in the company. As more information about the investment comes out and people start to analyze it, there may be even more positive news in the coming days, further driving up share prices and making Zai Lab Limited an attractive investment opportunity.

Trending News 🌥️

Samsonite International S.A. recently unveiled their collaboration with New Balance in Asia Pacific. The partnership brings together two renowned brands in an effort to produce a unique and high-quality collection of travel and lifestyle products. The Asia Pacific collaboration between Samsonite and New Balance includes travel items such as rolling suitcases, duffle bags, and backpacks.

Additionally, lifestyle pieces such as totes and wallets make up the capsule collection. All pieces feature a modern black-on-black color scheme, allowing the user to seamlessly transition between business and leisure activities. The collection is crafted for the modern traveler with uncompromising style and comfort. The pieces feature lightweight designs and are made from premium materials for maximum durability. The line also takes into account practicality, with pockets for easy access to essentials like passports and boarding passes. This collaboration marks the first time Samsonite and New Balance have come together for a global campaign. It is an exciting move that speaks to the popularity of both brands and their commitment to providing high-end design to their customers. With this partnership, Samsonite and New Balance offer travelers a unique, fashionable way to navigate the world in style.

Stock Price

On Friday, SAMSONITE INTERNATIONAL S.A announced a collaboration with sportswear giant New Balance to launch a co-branded collection in Asia Pacific. The news has been well-received so far, with media coverage mostly positive. Despite the initial enthusiasm, the stock market took the news with a grain of salt, with SAMSONITE INTERNATIONAL S.A’s stock opening at HK$23.6 and closing at the same price, down by 0.6% from its previous closing price of HK$23.8. Live Quote…

Analysis

GoodWhale has conducted an analysis of SAMSONITE INTERNATIONAL S.A.’s wellbeing, and as per our findings, the fair value of SAMSONITE INTERNATIONAL S.A share is estimated to be around HK$17.7. This value was calculated using our proprietary Valuation Line. At present, SAMSONITE INTERNATIONAL S.A stock is trading at HK$23.6, which is overvalued by 33.3%. More…

Summary

SAMSONITE International S.A. recently announced a collaboration with New Balance in the Asia Pacific region, for which it has received mostly positive media coverage. This could be a great investment opportunity for investors, as it indicates the company is growing and diversifying its portfolio in new markets. The collaboration could be a stepping stone to further international expansion, bringing SAMSONITE into closer proximity with potentially lucrative markets.

SAMSONITE also offers a competitive dividend payout, which could be attractive to investors seeking steady income streams. Overall, SAMSONITE provides investors with good growth potential and the potential to generate steady income through dividend payments.

Trending News 🌥️

Adaptimmune Therapeutics plc has recently seen a boost in the stake of Barclays PLC. This has been a positive sign for investors, as Barclays’ decision to re-invest in Adaptimmune Therapeutics plc speaks volumes about their confidence in the stock and its future prospects. Adaptimmune Therapeutics plc is a clinical-stage biotechnology company, specializing in developing T-cell therapies for cancer treatments. The company’s core focus is on personalizing therapies that target the underlying immune system of individual patients. Their approach looks to identify cancer-specific neoantigens which T cells can use to recognize and attack cancer cells.

Investment by Barclays PLC is a sign of confidence in the company’s ambitious plans and unique approach to developing novel treatments for cancer. Adaptimmune Therapeutics plc has had a series of successes following their research and development efforts, with a number of promising partnerships and clinical trials being initiated over the last few years. These successful trials in particular have attracted attention from industry giants like Barclays PLC, who are looking to get access to the best leads in biotech and drug development. With these successes, Adaptimmune Therapeutics plc stands on a very strong footing as they look to progress research and hopefully develop groundbreaking treatments for cancer patients throughout the world.

Price History

On Wednesday, Adaptimmune Therapeutics plc saw a slight dip in stock prices when their shares opened at $1.6 and closed at the same price, representing a 0.6% decrease from the prior closing price of $1.7. Despite the reduced stock prices, Barclays PLC seemed undaunted and increased its stake in the company. This investment comes as a boost to Adaptimmune, who is working on cutting-edge technology in the field of cancer immunotherapy. The company is focused on developing novel T-cell therapies to treat cancer and autoimmune diseases, leveraging their proprietary SPEAR T-cell receptor platform.

Their platform is designed to identify cancer targets on patient cells and reprogram the patient’s own T-cells to recognize and fight the cancer cells. With the increased investment from Barclays PLC, Adaptimmune will be able to continue pushing its boundaries in this innovative field. Live Quote…

Analysis

Our team at GoodWhale conducted an analysis of ADAPTIMMUNE THERAPEUTICS’s wellbeing and discovered that the company is strong in asset and growth, but weak in dividend and profitability. According to GoodWhale’s Star Chart, ADAPTIMMUNE THERAPEUTICS is classified as a ‘cheetah’, a type of company that achieves high revenue or earnings growth but considered less stable due to lower profitability. This type of company may be attractive to investors who are comfortable taking on higher risk for potentially higher rewards. ADAPTIMMUNE THERAPEUTICS has an intermediate health score of 4/10 with regards to its cashflows and debt, which suggests that the company may be able to sustain future operations in times of crisis. More…

Summary

Barclays PLC has recently increased its stake in Adaptimmune Therapeutics plc (ADAPT), a clinical-stage biopharmaceutical company engaged in the development of novel cancer immunotherapy treatments. This strategic investment is a sign of confidence in the company’s potential and progress to date. ADAPT has successfully completed Phase 1 and 2 clinical trials for its lead candidate, NY-ESO TCR, providing evidence for its efficacy and safety. ADAPT has also secured partnerships with leading pharmaceutical companies such as GlaxoSmithKline and Merck & Co.

Additionally, the company has developed a next-generation affinity enhancement technology (AET) to improve its CAR-T cell therapies. ADAPT’s promising advances have attracted many large investors, including Barclays PLC. It is expected that the company will soon have a broad portfolio of innovative cancer therapies under development and that its share price will appreciate significantly over time.

Trending News 🌥️

KDDI Corporation, one of Japan’s leading telecommunications companies, has announced the launch of 5G Open vRAN sites in Japan in partnership with Samsung Electronics. This marks the start of commercial deployment in the nation and is a significant step forward in the transition to fifth-generation (5G) technology. KDDI and Samsung have worked together to establish 5G Open vRAN sites in many locations throughout Japan. These sites can support a wide range of services, including cloud gaming and virtual reality (VR) as well as industrial internet of things applications. The open vRAN sites are designed to provide enhanced signal coverage, faster speeds, and improved reliability for users operating in congested urban areas. KDDI and Samsung have also collaborated to create a 5G platform that features open interface technology, allowing customers to quickly and easily customize their services according to their requirements.

This platform has been designed to provide flexibility and scalability, allowing customers to quickly switch between services and operators in order to optimize their experience. The 5G Open vRAN sites launched by KDDI and Samsung are an important milestone for the deployment of 5G technology in Japan. This is the first major step towards full commercial deployment and will help to accelerate the development of innovative 5G applications and services. With the increased availability of 5G services, consumers and businesses in Japan will soon be able to take advantage of all the opportunities that come with this new technology.

Price History

On Friday, KDDI CORPORATION and Samsung Electronic announced the launch of 5G Open vRAN sites in Japan. The media sentiment around the news was generally positive, with the company’s stock opening at JP¥3979.0 and closing at JP¥3991.0, down by 0.4% from the previous closing price of 4008.0. This new 5G network will benefit both KDDI CORPORATION and Samsung Electronic with increased sales, as well as providing a reliable and stable connection for customers in Japan. This move is a positive step in the development of Japan’s telecoms industry and will likely have a positive impact on the country’s economy. Live Quote…

Analysis

GoodWhale conducted an analysis of KDDI CORPORATION’s wellbeing and found that it is classified as a ‘cow’, meaning it has the track record of paying out consistent and sustainable dividends. This type of company may be of interest to investors looking for long-term, stable returns. KDDI CORPORATION scored 8/10 on GoodWhale’s health ranking, indicating its strong financial condition and ability to remain in operation during times of crisis. Looking at other metrics, KDDI CORPORATION was found to be strong in dividend and profitability, medium in terms of assets and weak in terms of growth. More…

Summary

KDDI Corporation has recently launched two 5G Open vRAN sites in Japan, in partnership with Samsung Electronics. Overall media sentiment for this move has been positive. For investors looking to invest in this company, it is important to note the long-term viability of the move. KDDI has a strong presence in the industry and its 5G Open vRAN initiative can be seen as a long-term commitment to innovation and development. The company has also invested heavily in its mobile network infrastructure, which may see increased uptake as 5G becomes more prevalent. As such, KDDI is a good option for investors wanting a long-term commitment that could yield higher returns in the future.

Additionally, the company is continuing to expand its services and its partnerships both domestically and internationally, which are beneficial for investors looking for a diversified portfolio. All in all, KDDI is an attractive option for investors looking for a secure, long-term investment.

Trending News 🌥️

NioCorp Developments has made the news again with its recent acquisition by GX Acquisition Corp. II. This merger will be beneficial for the company and its stakeholders, creating new opportunities for growth and development in the future. GX Acquisition Corp. II is looking to expand their reach and this merger will help accomplish just that. NioCorp Developments specializes in rare earth element-based products, and this acquisition will allow GX Acquisition Corp. II to further explore those rare earth elements and what they could be used for in the future. The acquisition will also mean new and innovative products that could be developed and sold, as well as job creation throughout the organization. This will provide more employment opportunities and help create a stronger economic base.

It is expected that, in the coming months, both companies will reap the rewards of this acquisition. With the combined resources, they will be able to provide high-quality products and services to their customers and fulfill their mission of creating a more efficient and profitable business. This acquisition is a great example of how two companies can come together to create something greater than what either one could have achieved alone. It is expected that this merger will provide a boost to the companies’ bottom lines and allow them to expand their operations even further.

Price History

On Tuesday, NioCorp Developments Ltd. announced the acquisition of GX Acquisition Corp. II, a publicly traded special purpose acquisition company (SPAC). Upon the closing of the amalgamation agreement, GX Acquisition Corp. II will become a wholly-owned subsidiary of NioCorp. The stock price of GX Acquisition Corp. II opened at $10.1 and closed at the same price on Tuesday’s trading day. The acquisition will pave the way for NioCorp’s business plan to operationalize its Elk Creek Superalloy Materials Project in Nebraska.

NioCorp’s Chairman and CEO, Mark Smith, said that the completion of this transaction will empower the company to deliver strong value for shareholders in the long run. The amalgamation marks a significant milestone for NioCorp, as it will enable them to expand their capabilities and diversify across multiple industry verticals. With growing production and cost savings strategies, NioCorp aims to generate increased revenue from multiple sources. Live Quote…

Analysis

GoodWhale has conducted a detailed analysis of GX ACQUISITION’s fundamentals and our Star Chart gives GX ACQUISITION an intermediate health score of 6/10 with regard to its cashflows and debt. This indicates that GX ACQUISITION is likely to safely ride out any crisis without the risk of bankruptcy. GX ACQUISITION is classified as an ‘elephant’ company, which is rich in assets after deducting off liabilities. These are usually attractive to investors looking for an income stream and a stable appreciation in share price. While GX ACQUISITION may have some weaknesses in areas such as asset structure, dividend yield and growth potential, the company is actually quite strong when it comes to profitability and debt structure. Therefore investors looking for stable returns with potential upside should consider placing GX ACQUISITION on their watchlist. More…

Summary

GX Acquisition Corp. II has recently been acquired by NioCorp Developments, a development-stage mining company. The acquisition is an all-stock transaction that will bring the company a new range of mining capabilities and provide a foundation for increased growth in the industry. This acquisition will allow NioCorp to leverage GXAC II’s financial resources, strong management team and expertise to enhance their business strategy and drive long-term value creation. Investors can benefit from this transaction through improved financial flexibility, reduced capital costs and increased access to capital, as well as increased potential for long-term growth in the sector.

Trending News 🌥️

January has seen an impressive surge in short positions for Carney Technology Acquisition Corp. II, signaling a major shift in market sentiment. These sudden shifts in the number of short positions indicate that investors are becoming increasingly pessimistic about the prospects of Carney Technology Acquisition Corp. II. Analysts have raised concerns over various aspects of Carney’s acquisitions, including their sustainability and their potential to negatively impact their earnings.

Additionally, market watchers have taken note of the heightened risk associated with investing in this sector. This jump in short positions has had a noticeable effect on Carney Technology Acquisition Corp. II’s stock price, which has declined sharply since the beginning of the year. Analysts speculate that this price drop is due to heightened investor caution and fears of further declines ahead. Additionally, it’s worth noting that some investors may be using this period of volatility to their advantage, taking advantage of lower prices to build up a stronger position on Carney Technology Acquisition Corp. II. Overall, January has seen a significant increase in short positions for Carney Technology Acquisition Corp. II, signaling a shift in investor sentiment. While the effects of this influx of short positions remain to be seen, it’s clear that the volatility and risk associated with investing in this sector are not going away anytime soon.

Price History

January has seen a noteworthy increase in the number of short positions for Carney Technology Acquisition Corp. II (CARNEY TECHNOLOGY ACQUISITION). Until now, news sentiment for the publicly traded company has mostly been positive, with industry analysts suggesting that their products and services will continue to be successful. On Tuesday, CARNEY TECHNOLOGY ACQUISITION’s stock opened at $10.2 and closed at $10.2, without much fluctuation. The spike in short positions is certainly an important factor to consider when looking at Carney’s current financial standing and future prospects. Live Quote…

Analysis

GoodWhale has conducted an analysis of CARNEY TECHNOLOGY ACQUISITION’s financials. The Star Chart assigned CARNEY TECHNOLOGY ACQUISITION an intermediate health score of 6/10, indicating that it might be able to sustain future operations in times of crisis. CARNEY TECHNOLOGY ACQUISITION is classified as a ‘cheetah’, a type of company that achieved high revenue or earnings growth but is considered less stable due to lower profitability. Given CARNEY TECHNOLOGY ACQUISITION’s profile, certain types of investors may be interested in the company. The company is strong in medium-growth and weak in assets, dividends, and profitability. As such, investors with a high risk tolerance are more likely to benefit from this type of investment. Investors with a lower risk tolerance should be wary, as the company may not provide the same stability as other investments. That said, those with a higher risk tolerance may find this company to be a viable option. More…

Summary

Investors were cautiously optimistic about the Carney Technology Acquisition Corp. II in January, seeing a significant increase in short positions. Although the news sentiment has mostly been positive, the overall investing dynamics have yet to significantly change. Analysts have urged caution due to the uncertainty surrounding the company’s future performance and there is concern among investors regarding the short-term nature of the stock’s likely returns. Nevertheless, Carney Technology Acquisition Corp. II shares are seen as a potential bargain given the current market environment and could be worth looking into for investors seeking opportunities in the tech sector.

Trending News 🌥️

BlackRock, the world’s largest asset manager, is the latest addition to the metaverse ETF race with the launch of its iShares Future Metaverse Tech and Communications ETF. This ETF gives investors access to companies that provide the hardware and software to power the metaverse – a virtual world of augmented and virtual reality, gaming, 3D software and social media platforms. With this launch, BlackRock has joined Roundhill Investments and ProShares as part of this lucrative ETF market. The booming metaverse ETF market is a testament to the accelerating growth of the metaverse and the opportunities it presents for investors worldwide.

The ETF provides a diversified portfolio of companies in the tech and communication space that have been early adopters of the metaverse. Investors can gain a broad exposure to the cutting edge of virtual world technologies without having to invest in individual stocks. This is an exciting move for investors looking to diversify their portfolios and take advantage of the potential of the metaverse.

Stock Price

This week, BlackRock has joined the race to launch an ETF focusing on the growing metaverse technology sector. The latest ETF launch is the iShares Future Metaverse Tech and Communication ETF, which has so far been met with positive news. On Tuesday, Facebook stock opened at $174.3 and closed at $172.1, down by 0.5% from its prior closing price of 172.9. This minor price movement marks a lackluster response to the news of the latest ETF launch but it is too early to draw conclusions as to how investors will consider this new ETF in the long run. Live Quote…

Analysis

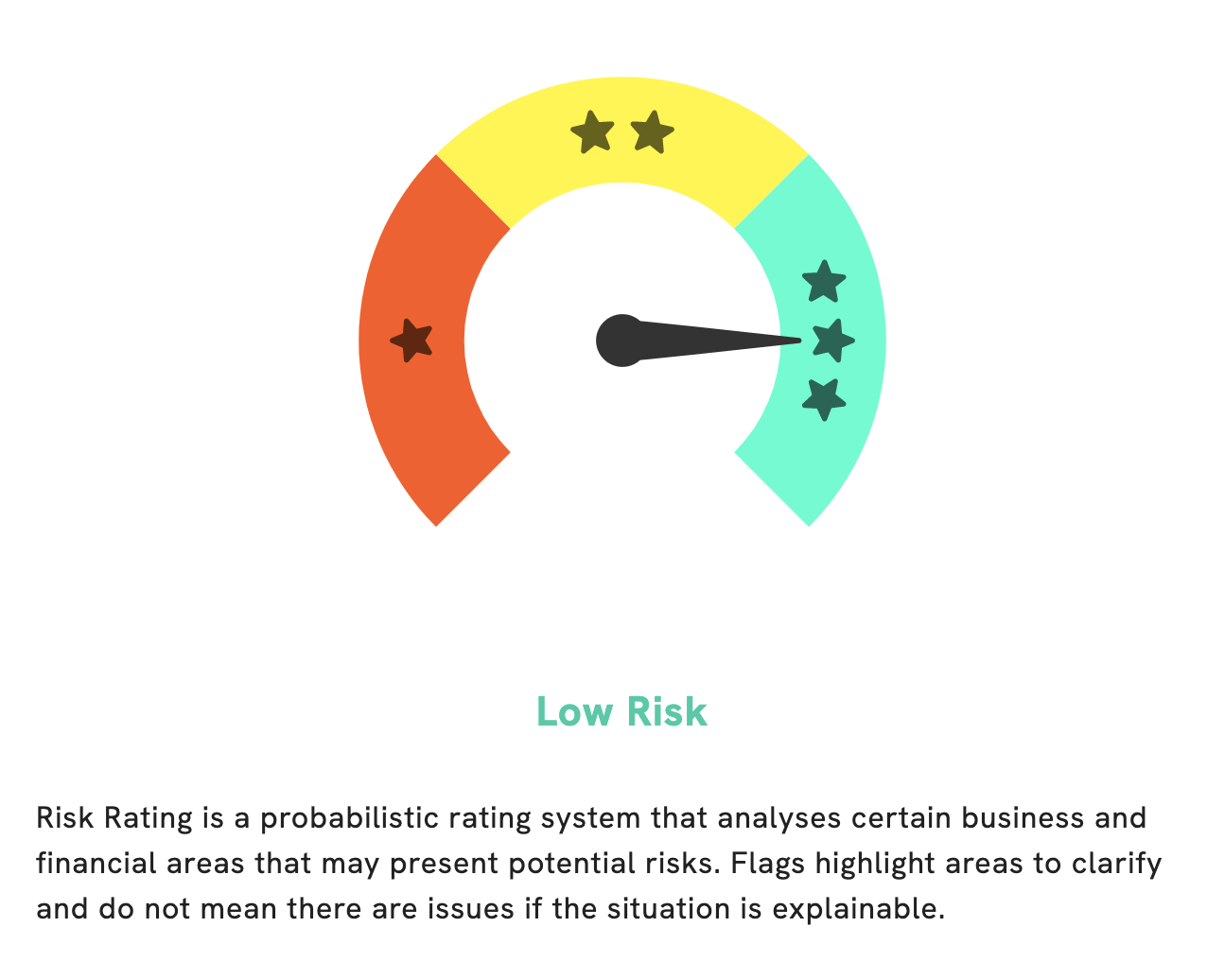

At GoodWhale, we recently conducted a detailed analysis of Facebook’s fundamentals. Our Risk Rating assessment found that Facebook is a low risk investment in terms of financial and business aspects. Despite this, we identified one risk warning in their balance sheet which any investor should take into account when considering a Facebook stake. If you would like to look into it further, simply register on our website, goodwhale.com, to gain access to this information. With our ratings and analysis, investors can make more informed decisions about their stock selection. More…

Summary

Facebook has launched its first Metaverse ETF, the iShares Future Metaverse Tech and Communication ETF, in partnership with BlackRock. The ETF looks to invest in companies related to online communications, virtual reality, augmented reality, and other related next-generation technologies. Analysts have suggested that this could be a strong play for long-term investors interested in the potential of this technology sector.

The ETF holds the potential to benefit from the growing demand of digital platforms, emerging technologies, and digital communications markets. It may also serve as a diversification option for investors looking to capitalize on the aforementioned trends.

Trending News 🌥️

In a note to clients, analyst Louie DiPalma wrote that the stock price of Palantir Technologies had dropped by 8% due to the upcoming renewal of six contracts in the next 15 months. These contracts include three of Palantir’s four largest government customers, making their renewals critical for the Palo Alto-based company. DiPalma also noted that these renewal periods have been an opportunity for other open-sourced solutions to increase their competitive edge against Palantir’s proprietary software. This competitive landscape has been a source of anxiety for investors, as some agencies may view Palantir’s software as a more temporary solution until they can adopt an open-sourced data analytics system. This strategic decision could potentially lead to the termination of some of Palantir’s contracts and, in turn, reduce their market share.

This uncertainty among investors is likely driving the current drop in Palantir’s stock price. Regardless, DiPalma is confident that Palantir can successfully renew its contracts and continue to expand its business over the next 15 months. He believes that, despite the looming competition, Palantir still has a strong advantage given its “high-margin” enterprise license and its technical capabilities. Ultimately, the success or failure of the renewables will depend on which software solution can best meet the needs of the customer.

Price History

On Tuesday, Palantir Technologies, the software company specializing in data analysis, witnessed a 7.9% drop from its last closing price of 9.2 when it opened at $9.0 in the morning and closed at $8.5. Despite the plummet, media attention has been mostly positive around Palantir since it offers open-source solutions to both government and corporate clients. The decrease was reportedly due to the company’s six major contract renewals looming in the near future. In particular, the renewal of contracts with U.S. Intelligence Agencies has caused some investors to worry, as the said contracts could be worth up to several million dollars each and could mean a hefty sum to Palantir’s bottom line. Ultimately, the drop in Palantir’s stock price could be attributed to investor fear and uncertainty regarding the company’s ability to renew key contracts in the upcoming months.

However, with open-source solutions now becoming increasingly popular with both government and corporate clients, Palantir may be able to weather the storm if it is able to transition from selling proprietary technologies to offering more open-source solutions as well. Live Quote…

Analysis

At GoodWhale, we recently conducted an analysis of the wellbeing of PALANTIR TECHNOLOGIES. Our risk rating system determined that PALANTIR TECHNOLOGIES is a medium risk investment in both financial and business aspects. From our analysis, we have detected three risk warnings in their balance sheet, cashflow statement and non financial. If you would like to access this data, please register on our website goodwhale.com. We will provide you with a comprehensive analysis of PALANTIR TECHNOLOGIES and further insights about their wellbeing. More…

Summary

Investors seem uncertain about Palantir Technologies shares. On the one hand, they have had a steady stream of positive media exposure, indicating that their products are in demand. On the other, six major contract renewals are looming, as well as potential threats from open-sourced solutions. These factors have caused Palantir Technologies’ stock price to decline 8% in the short term.

In spite of this, there could be value in the long-term outlook of the company given their established foothold in the data analytics market. Investors should evaluate the current situation carefully before deciding on whether to invest or not.

Trending News 🌥️

However, when looking closer at its money matters, the giant retailer appears to have had a lot of luck to thank for its longevity in the industry. This lucky break raises questions regarding the company’s resilience in the years after that crash, and whether or not it would have been strong enough to survive such an event without this generous funding. In spite of these concerns, Amazon has been praised for its strategy, constantly pushing boundaries and expanding its products and services to solidify their position as a leader in the online retail market. This is evident in their rapid growth over recent years, as well as their increased investments into multiple sectors.

It is clear that Amazon is off to a fantastic start; however, questions remain regarding its true potential. With such a fortunate start, could the company be able to sustain itself without the generous funding received before the dot-com crash?

Market Price

As news coverage of Amazon’s stock has shifted to mainly negative news, questions are being raised about the company’s resilience. On Tuesday, Amazon’s stock opened at $95.3 and closed at $94.6, down by 2.7% from its previous closing price of 97.2. This deal allowed the company to weather the crash while other internet companies perished, and investors are now wondering if Amazon’s success is still supported by these previous investments. With a declining stock price, investors are anxious to see if Amazon has enough resilience to stay afloat in today’s markets. Live Quote…

Analysis

GoodWhale has thoroughly analyzed the fundamentals of AMAZON.COM. Our Risk Rating system has concluded that this company is a low risk investment in terms of both financial and business-related aspects. While it is generally safe to invest in the company, GoodWhale has nevertheless detected one risk warning in their income sheet. To access this warning and for more detailed information about AMAZON.COM’s investment prospects, we suggest becoming a registered user of our platform. More…

Peers

Amazon.com Inc is an American multinational technology company based in Seattle, Washington, that focuses on e-commerce, cloud computing, digital streaming, and artificial intelligence. It is considered one of the Big Four technology companies, alongside Google, Apple, and Facebook.

PChome Online Inc is a Taiwanese online shopping company established in 2000. PChome Online is the largest e-commerce platform in Taiwan, with over 60% of the country’s online shopping market share.

The RealReal Inc is an American online luxury resale store headquartered in San Francisco, California. The company sells consigned clothing, accessories, jewelry, watches, and art from a variety of luxury brands.

Zalando SE is a German e-commerce company headquartered in Berlin, that specializes in selling shoes, clothing, and other fashion items. The company was founded in 2008 and has since grown to become one of the largest online fashion retailers in Europe.

– PChome Online Inc ($TPEX:8044)

PChome Online Inc is a Chinese internet company that provides online services through its websites. The company offers a variety of services, including online shopping, online payments, online advertising, and others. PChome Online Inc is listed on the Nasdaq Global Market under the ticker symbol PCLN.

As of 2022, PChome Online Inc had a market capitalization of 5.78 billion US dollars. The company’s return on equity was 3.34 percent. PChome Online Inc is a leading player in the Chinese internet market, with a strong presence in online shopping and online payments. The company is well positioned to benefit from the growing trend of online shopping in China.

– The RealReal Inc ($NASDAQ:REAL)

The RealReal Inc is a luxury consignment company with a market cap of 117.51M as of 2022. The company offers consignment services for luxury items such as clothing, jewelry, and watches. The company has a return on equity of 137.64%.

– Zalando SE ($OTCPK:ZLDSF)

Zalando SE is a German e-commerce company that specializes in selling shoes, clothing and other fashion items. The company was founded in 2008 and is headquartered in Berlin. As of 2022, Zalando SE has a market cap of 5.66B and a return on equity of 4.78%. The company’s main competitors are Amazon, eBay and Alibaba.

Summary

Amazon.com‘s pre-dot com crash financing deals have led to questions over its resilience. Despite the recent negative news coverage, Amazon remains an attractive investment opportunity due to its well-established brand recognition, highly diversified business model, and strong industry presence. Recently, Amazon has achieved record highs in total sales and profitability, along with strong growth in market share across various sectors such as eCommerce, cloud computing, artificial intelligence, and digital content.

Additionally, the company has a robust balance sheet with significant cash reserves and solid liquidity. Analysts have noted that Amazon is well-positioned to weather any short-term economic downturns and will be able to benefit from long-term growth trends in the digital economy.

Related Posts

Recent Posts

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Investing Everyone Can Do.

Investing shouldn’t be exclusive to a select few. We believe everyone should have the opportunity to grow their wealth. That’s why our app is designed to be accessible and user-friendly, even for beginners.