Yelp Set to Exceed Earnings Expectations in Q3 Release, Despite Anticipated Year-Over-Year Decline

November 6, 2024

🌥️Trending News

YELP INC ($NYSE:YELP), the popular online platform for business reviews and recommendations, is set to release its third quarter financial results on November 1st. While analysts are predicting a slight decrease in earnings compared to last year, there is anticipation that Yelp will still exceed earnings expectations due to an increase in revenue. Despite the expected year-over-year decline in earnings, Yelp has been experiencing steady growth in revenue. This can be attributed to the company’s continued efforts to expand its services and improve its user experience. One of the key factors contributing to Yelp’s revenue growth is its advertising business. The company offers a variety of advertising options for businesses, including local ads, targeted display ads, and sponsored search results. With an increasing number of businesses recognizing the value of online advertising, Yelp has been able to attract more advertisers to its platform. This has not only resulted in an increase in revenue but has also helped businesses reach a wider audience on Yelp.

In addition to its advertising business, Yelp’s partnership with Grubhub has also been a significant source of revenue for the company. The partnership allows users to order food directly from restaurants listed on Yelp, with Grubhub handling the delivery. This service has become increasingly popular, especially during the pandemic when more people turned to online food ordering. As a result, Grubhub has reported an increase in orders through Yelp, contributing to Yelp’s revenue growth. Overall, despite the anticipated decline in earnings compared to last year, Yelp’s expected increase in revenue for the third quarter is a positive sign for the company. With its continued efforts to improve its platform and attract more advertisers and users, Yelp is well-positioned to exceed earnings expectations and continue its growth trajectory. Investors will be eagerly awaiting the company’s Q3 release to see if Yelp can maintain its upward trend and deliver strong financial results once again.

Earnings

Despite an anticipated year-over-year decline, the company’s latest earnings report for FY2023 Q4, ending December 31, 2021, shows a total revenue of 273.4M USD and a net income of 23.19M USD. Compared to the previous year, Yelp Inc has seen a decrease of 11.5% in total revenue.

However, there has been a significant increase of 15.1% in net income. This is a promising sign for the company as it shows a continued focus on profitability. In the last three years, Yelp Inc’s total revenue has steadily increased from 273.4M USD to 342.38M USD. This is a testament to the company’s strong business model and ability to adapt to changing market conditions. This is a positive sign for investors and stakeholders, indicating a strong financial outlook for the company. Yelp Inc’s success can be attributed to its continuous efforts to improve user experience and expand its services. The platform has evolved from being a simple review site to providing a range of features such as online reservations, food delivery, and appointment booking. These additions have not only increased user engagement but also diversified the company’s revenue streams. In conclusion, while Yelp Inc may face a decline in year-over-year revenue, its net income has shown an upward trend. With a strong track record of growth and continuous efforts to innovate and expand, Yelp Inc is positioned to exceed earnings expectations in its Q3 release. Investors can look forward to a promising financial performance from the company in the upcoming quarter.

About the Company

Income Snapshot

Below shows the total revenue, net income and net margin for Yelp Inc. More…

| Total Revenues | Net Income | Net Margin |

| 1.34k | 99.17 | 7.4% |

Cash Flow Snapshot

Below shows the cash from operations, investing and financing for Yelp Inc. More…

| Operations | Investing | Financing |

| 306.28 | -54.68 | -246.78 |

Balance Sheet Snapshot

Below shows the total assets, liabilities and book value per share for Yelp Inc. More…

| Total Assets | Total Liabilities | Book Value Per Share |

| 1.01k | 265.19 | 10.95 |

Key Ratios Snapshot

Some of the financial key ratios for Yelp Inc are shown below. More…

| 3Y Rev Growth | 3Y Operating Profit Growth | Operating Margin |

| 15.3% | 18.0% | 5.9% |

| FCF Margin | ROE | ROA |

| 20.9% | 6.6% | 4.9% |

Share Price

Despite analysts’ predictions of a year-over-year decline in revenue, the company’s stock opened at $34.1 on Friday and closed at $33.91, down by only 0.67% from the previous day’s closing price of $34.14. This slight dip in stock price may be attributed to the overall volatile market conditions, but it is still a positive sign for Yelp as they head into their third quarter earnings release. The company has consistently outperformed expectations in recent quarters, with strong revenue growth and user engagement. Yelp’s main source of revenue comes from local advertising, and with many businesses facing financial struggles and closures, it is expected that there will be a decrease in advertising spending.

However, Yelp has taken steps to mitigate the effects of the pandemic on their business.

In addition, Yelp has also implemented cost-cutting measures to improve their financial position. Despite the challenges presented by the pandemic, Yelp’s core business model remains strong. Overall, while Yelp may experience a decline in revenue for the third quarter, the company is well-positioned to weather the challenges brought on by the pandemic. With a strong user base and efforts to support small businesses, Yelp is expected to exceed earnings expectations in their upcoming release. Investors will be keeping a close eye on the company’s performance and guidance for the future. Live Quote…

Analysis

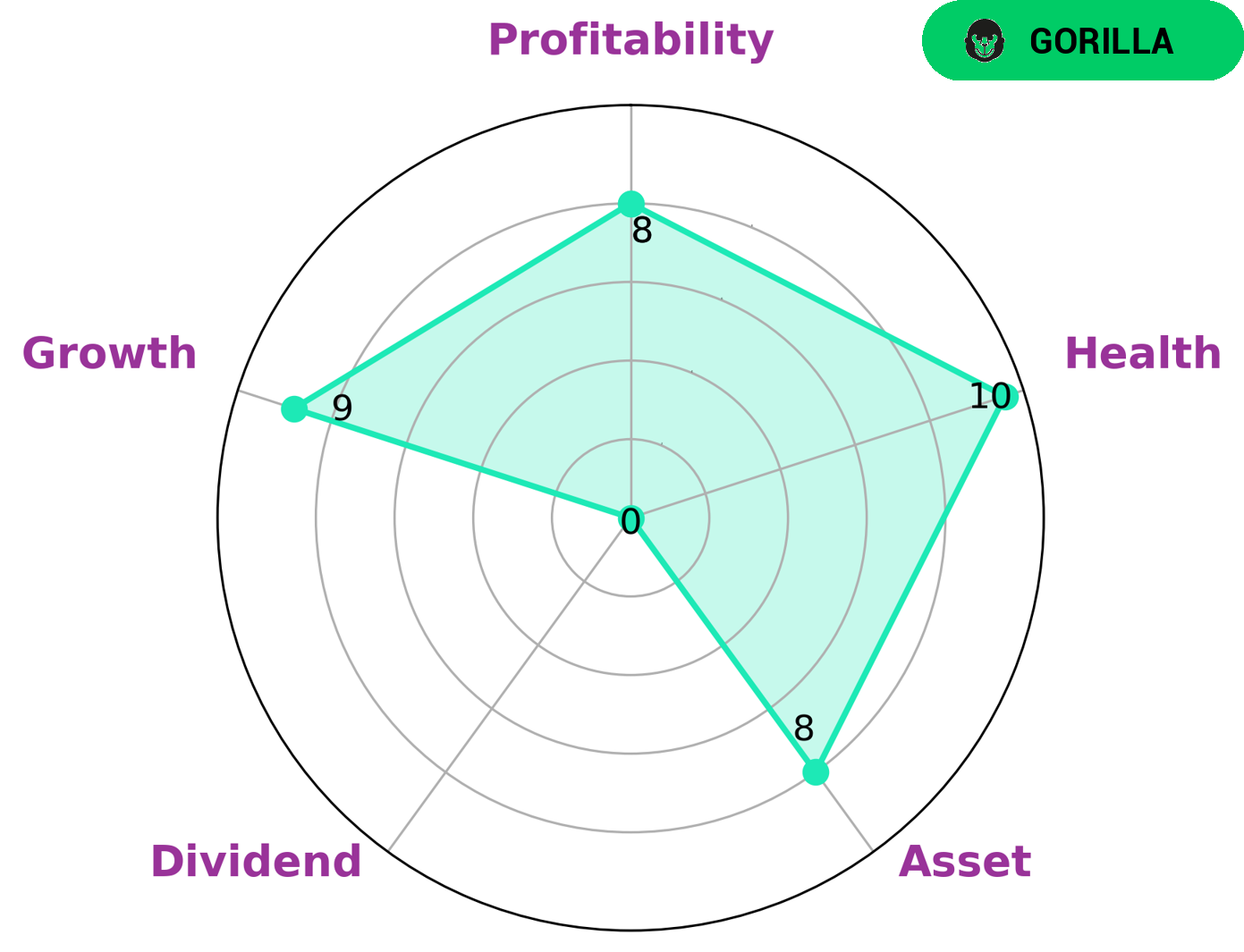

As GoodWhale, I have conducted a thorough analysis of the fundamentals of YELP INC, and the results are quite impressive. After reviewing its financial data, I have concluded that YELP INC is a company with a strong competitive advantage, placing it in the category of ‘gorilla’ companies. This type of company is known for achieving stable and high revenue or earning growth, which is a clear indication of YELP INC’s success in the market. One of the key factors that contribute to this high growth and stability is YELP INC’s strong fundamentals in terms of assets, growth, and profitability. Its strong asset base provides a solid foundation for future growth, while its consistently high profitability marks its ability to generate strong returns for its investors. This, coupled with its strong growth trajectory, makes YELP INC an attractive option for investors looking for long-term growth potential. However, it is worth noting that YELP INC does have a weak point in terms of dividends. This means that while investors may not receive regular dividend payments from the company, they can still benefit from its overall growth and profitability. In terms of risk management, I am pleased to report that YELP INC has a high health score of 10/10. This means that the company’s cashflows and debt levels are strong enough to withstand any potential crisis, reducing the risk of bankruptcy. As such, YELP INC is a safe bet for investors looking for a stable and secure investment option. Overall, YELP INC is a strong and attractive company for investors who are interested in long-term growth potential. Its solid fundamentals, coupled with its strong risk management capabilities, make it a promising option for those looking to invest in a ‘gorilla’ company. I would highly recommend keeping an eye on YELP INC and considering it as an addition to any investment portfolio. More…

Peers

It operates in the United States, Canada, Australia, New Zealand, the United Kingdom, and Ireland. Yelp Inc has a market capitalization of $26.92 billion as of 2020. Its competitors are Personas Social Incorporated, Mdf Commerce Inc, and Qutoutiao Inc.

– Personas Social Incorporated ($TSXV:PRSN)

Personas Social Incorporated is a social media company with a market cap of 8.2M as of 2022. The company has a Return on Equity of 49.94%. Personas Social Incorporated operates a social media platform that allows users to connect with friends and family, share photos and videos, and stay up-to-date on news and current events.

– Mdf Commerce Inc ($TSX:MDF)

Mdf Commerce Inc is a publicly traded company with a market capitalization of 147.3 million as of 2022. The company has a negative return on equity of 5.27%. Mdf Commerce Inc is a provider of online marketplace services for buyers and sellers of goods and services. The company operates in North America, Europe, Asia, and South America.

– Qutoutiao Inc ($NASDAQ:QTT)

As of 2022, Qutoutiao Inc has a market cap of 11.39M and a ROE of 33.26%. The company is an online content platform that provides users with personalized content recommendations. The company was founded in 2016 and is headquartered in Shanghai, China.

Summary

Yelp Inc is expected to report an increase in revenue but a decline in earnings when it announces its Q3 results. Investors are closely watching Yelp’s performance as a key indicator of the economic recovery from the pandemic. Analysts believe that Yelp’s strong online presence and focus on local businesses will help the company weather the current economic climate. Overall, Yelp’s upcoming earnings release is anticipated to be positive for investors.

Related Posts

Recent Posts

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Investing Everyone Can Do.

Investing shouldn’t be exclusive to a select few. We believe everyone should have the opportunity to grow their wealth. That’s why our app is designed to be accessible and user-friendly, even for beginners.