Wall Street Predicts Strong Q3 Earnings for Entegris, Analysts Expect $0.79 Per Share

October 31, 2024

☀️Trending News

ENTEGRIS ($NASDAQ:ENTG) is a leading provider of materials and solutions for the microelectronics industry. The company supplies critical products and services to the semiconductor, display, and other high-tech industries, helping customers improve efficiency and reliability in their manufacturing processes. With a strong focus on innovation and customer satisfaction, Entegris has established itself as a key player in the global microelectronics market. Wall Street analysts have high expectations for Entegris’ upcoming Q3 earnings report. According to the latest predictions, the company is expected to report a profit of $0.79 per share, showcasing a growth compared to the previous year. This comes as no surprise, as Entegris has consistently delivered strong financial results in recent years. One key factor contributing to the positive outlook for Entegris is the ongoing growth in demand for microelectronics. As technology continues to advance and consumers’ reliance on electronic devices increases, the demand for semiconductors and other high-tech components is on the rise. This bodes well for Entegris, as the company is well-positioned to capitalize on this trend with its top-of-the-line products and services. Another key driver for Entegris’ success is its commitment to research and development. The company invests heavily in innovation and constantly develops new and improved products to meet the evolving needs of its customers. This dedication to staying at the forefront of technology has allowed Entegris to maintain a competitive edge in the market.

Additionally, Entegris has a strong track record of customer satisfaction, which has helped it build long-term relationships with some of the biggest names in the microelectronics industry. This has not only contributed to the company’s revenue growth but also solidifies its position as a trusted and reliable partner in the industry. With its strong market position, focus on innovation, and commitment to customer satisfaction, the company is well-positioned for continued success in the rapidly-growing microelectronics industry. Investors and stakeholders should keep a close eye on Entegris as it continues to showcase its strength and potential in the upcoming earnings report.

Share Price

According to analysts on Wall Street, Entegris is expected to report strong third quarter earnings, with an estimated earnings per share of $0.79. This prediction has caused a surge in the company’s stock price, as it opened at $103.86 on Friday and closed at $105.01, representing a 1.3% increase from the previous day’s closing price of $103.66. The positive forecast for Entegris’ earnings is reflective of the company’s recent performance and growth in the semiconductor industry. As a leading provider of advanced materials and process solutions, Entegris has been well-positioned to benefit from the growing demand for microchips and other high-tech products. One of the key drivers of Entegris’ success has been its strong customer relationships and partnerships with major semiconductor companies. This has allowed the company to expand its market share and increase its revenue, particularly in the advanced packaging and memory markets. In addition, Entegris’ focus on innovation and development of new technologies has also played a significant role in its success. The company has made strategic investments in research and development, allowing it to continuously improve and introduce new products that meet the changing needs of its customers. With the strong Q3 earnings forecast, investors are showing confidence in Entegris’ growth prospects and future performance.

However, it is important to note that there may be potential risks and uncertainties that could impact the company’s actual earnings results. Despite this, Entegris remains a solid player in the semiconductor industry and is well-positioned to continue its growth trajectory. As the demand for high-tech products continues to rise, analysts believe that Entegris will continue to be a strong performer in the market, making it a company to watch closely in the coming months. Live Quote…

About the Company

Income Snapshot

Below shows the total revenue, net income and net margin for Entegris. More…

| Total Revenues | Net Income | Net Margin |

| 3.52k | 180.67 | 5.3% |

Cash Flow Snapshot

Below shows the cash from operations, investing and financing for Entegris. More…

| Operations | Investing | Financing |

| 629.56 | 553.07 | -1.28k |

Balance Sheet Snapshot

Below shows the total assets, liabilities and book value per share for Entegris. More…

| Total Assets | Total Liabilities | Book Value Per Share |

| 8.81k | 5.4k | 22.67 |

Key Ratios Snapshot

Some of the financial key ratios for Entegris are shown below. More…

| 3Y Rev Growth | 3Y Operating Profit Growth | Operating Margin |

| 23.8% | 7.0% | 13.8% |

| FCF Margin | ROE | ROA |

| 4.9% | 8.9% | 3.4% |

Analysis

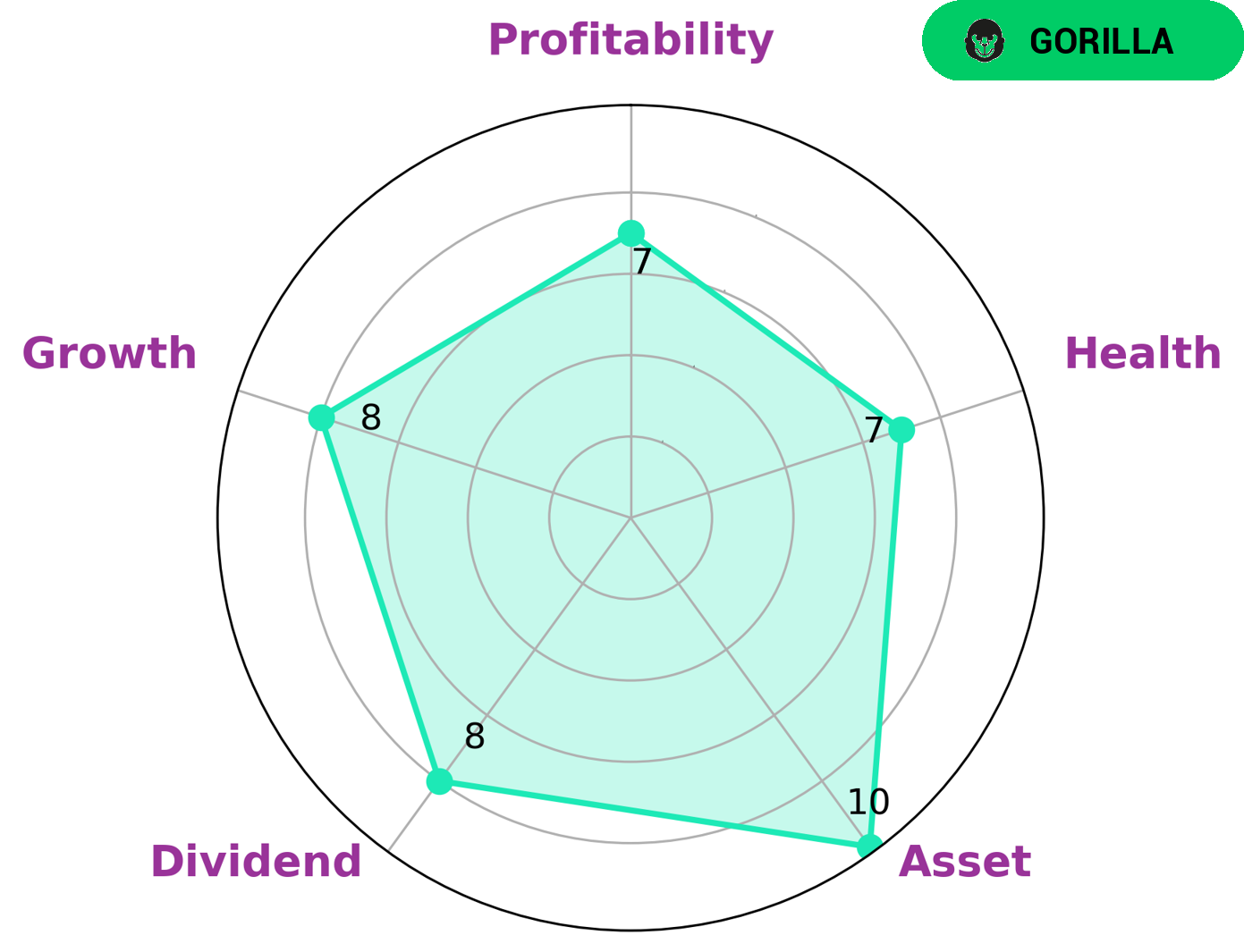

After carefully analyzing the financials of ENTEGRIS, I can confidently say that this company has a strong financial standing. In fact, according to our Star Chart, ENTEGRIS is excelling in areas such as assets, dividends, growth, and profitability. This is a promising sign for potential investors, as it indicates that the company is performing well and has the potential for future growth. One of the main factors contributing to ENTEGRIS’ strong financials is its high health score of 7/10. This takes into consideration the company’s cash flows and debt, and suggests that ENTEGRIS is capable of paying off its debts and funding future operations. This is an important aspect for investors to consider, as it shows that the company is financially stable and has the potential to continue growing in the long term. This is a desirable classification for investors, as it indicates that ENTEGRIS has a strong business model and competitive edge in its industry. In terms of the type of investors who may be interested in ENTEGRIS, I would say that it would appeal to those looking for a stable and potentially growing investment opportunity. The company’s strong financials and classification as a ‘gorilla’ make it an attractive option for both long-term and short-term investors. Additionally, those interested in the technology or materials industries may also find ENTEGRIS an appealing investment opportunity due to its strong performance in these areas. More…

Peers

Entegris, Inc. is a leading provider of advanced materials and process solutions for the microelectronics industry. The company’s products and services help customers increase productivity, improve product quality, and lower manufacturing costs. Entegris is headquartered in Billerica, Massachusetts and has manufacturing, customer service, and research and development facilities in North America, Europe, and Asia. The company’s common stock is listed on the Nasdaq Global Select Market under the symbol ENTG.

Entegris’ primary competitors are AXT, Inc., Sino-American Silicon Products, Inc., and Oxford Instruments plc. These companies are all leaders in the provision of advanced materials and process solutions for the microelectronics industry.

– AXT Inc ($NASDAQ:AXTI)

AXT, Inc., together with its subsidiaries, focuses on the design, development, and manufacture of compound and single element semiconductor substrates in China, Taiwan, South Korea, and Japan. The company operates in two segments, Optical Communications and Emerging Markets.

– Sino-American Silicon Products Inc ($TPEX:5483)

Sino-American Silicon Products Inc is a leading global supplier of silicon wafers. The company has a market cap of 71.23B as of 2022 and a ROE of 30.39%. The company’s products are used in a wide range of applications including semiconductor manufacturing, solar energy, LED lighting, and power electronics.

– Oxford Instruments PLC ($LSE:OXIG)

Oxford Instruments PLC is a world leader in the design and manufacture of high-performance scientific instruments and systems for research and industrial applications. Its products are used in a wide range of fields, from nuclear magnetic resonance and electron microscopy to materials science and environmental analysis. The company has a market capitalization of 1.08 billion as of 2022 and a return on equity of 13.3%. Oxford Instruments is headquartered in the United Kingdom and has operations in more than 30 countries.

Summary

Wall Street analysts are closely monitoring Entegris as it prepares to release its third quarter earnings report. The company is expected to post earnings of $0.79 per share, signaling a year-over-year improvement. This suggests that Entegris is performing well and could potentially be a lucrative investment opportunity.

Investors may also be looking at other key metrics, such as revenue and profit margins, to gain a better understanding of the company’s financial health. These projections from analysts could provide valuable insights into Entegris’ performance and help investors make informed decisions about their investments in the company.

Related Posts

Recent Posts

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Investing Everyone Can Do.

Investing shouldn’t be exclusive to a select few. We believe everyone should have the opportunity to grow their wealth. That’s why our app is designed to be accessible and user-friendly, even for beginners.