GROCERY OUTLET HOLDING Corp. Sees Lower Q3 Earnings Estimates from DA Davidson Analysts

November 5, 2024

🌧️Trending News

Grocery Outlet Holding ($NASDAQ:GO) Corp is a publicly traded company that operates a chain of discount grocery stores in the United States. Despite its success in the discount grocery market, Grocery Outlet Holding Corp has recently faced a setback in its projected earnings for the third quarter of 2024. According to analysts at DA Davidson, the company’s earnings per share estimates have been revised from $0.33 to $0.25. This news has caused concern among investors and shareholders, as it signifies a decrease in expected profits for the company’s shares. The reason for this revision in earnings estimates is not yet clear, but it could be attributed to various factors such as increased competition, changes in consumer spending habits, or supply chain issues.

However, this news should not overshadow the overall success of Grocery Outlet Holding Corp. The company has consistently reported strong sales growth and has seen a steady increase in its store count over the years. Furthermore, Grocery Outlet’s business model of offering discounted products has proven to be resilient during economic downturns, making it a reliable choice for investors. The company’s strong financial performance in recent years has also contributed to its positive reputation among customers and industry experts. It remains to be seen how this revision in earnings estimates will affect Grocery Outlet Holding Corp’s stock price and overall financial performance. However, with its established presence in the discount grocery market and a loyal customer base, the company is well-positioned to bounce back from this setback. Investors and shareholders will be closely monitoring the company’s upcoming quarterly earnings report to assess any further impacts on its financials.

Earnings

This comes after the company’s earnings report for the fourth quarter of fiscal year 2023, ending on December 31, 2021, which showed a total revenue of 782.7 million USD and a net income of 6.64 million USD. Compared to the previous year, GO experienced a 15.9% decrease in total revenue and a significant 58.2% decrease in net income. This decline in earnings may be concerning for investors and analysts alike, as it indicates a potential slowdown in growth for the company. The decrease in earnings for GO can be attributed to various factors, including supply chain disruptions, rising costs of goods, and ongoing challenges in the retail industry. These challenges have impacted many companies, and GO is no exception. The company has been focused on expanding its store footprint and increasing its product offerings, but these efforts may have been hindered by the current market conditions.

Despite this recent decrease in earnings, GO has shown significant growth over the past three years. Its total revenue has increased from 782.7 million USD to 989.82 million USD during this period, indicating a strong overall performance for the company. In conclusion, GROCERY OUTLET HOLDING Corp.’s earnings report for the fourth quarter of fiscal year 2023 has shown a decrease in total revenue and net income compared to the previous year. This trend is expected to continue into the third quarter of fiscal year 2023, according to estimates from DA Davidson analysts. Despite this setback, GO has shown significant growth over the past three years, but it remains to be seen how the company will navigate the current challenges and sustain its growth in the future.

About the Company

Income Snapshot

Below shows the total revenue, net income and net margin for GO. More…

| Total Revenues | Net Income | Net Margin |

| 3.97k | 79.44 | 2.1% |

Cash Flow Snapshot

Below shows the cash from operations, investing and financing for GO. More…

| Operations | Investing | Financing |

| 303.45 | -194.16 | -97.02 |

Balance Sheet Snapshot

Below shows the total assets, liabilities and book value per share for GO. More…

| Total Assets | Total Liabilities | Book Value Per Share |

| 2.97k | 1.75k | 12.28 |

Key Ratios Snapshot

Some of the financial key ratios for GO are shown below. More…

| 3Y Rev Growth | 3Y Operating Profit Growth | Operating Margin |

| 8.2% | 5.4% | 3.2% |

| FCF Margin | ROE | ROA |

| 2.8% | 6.6% | 2.7% |

Share Price

This positive movement in the stock price may come as a surprise to some, as analysts are anticipating lower earnings for the company. With many consumers turning to online shopping and delivery services, traditional brick-and-mortar grocery stores have seen a decline in foot traffic. Furthermore, GROCERY OUTLET HOLDING Corp. may also be feeling the effects of increased competition in the discount grocery market. As more and more retailers try to tap into this niche, it can lead to price wars and decreased profits for companies like GROCERY OUTLET HOLDING. Despite these challenges, GROCERY OUTLET HOLDING Corp. has continued to see growth in its business.

This expansion may help to offset some of the decline in earnings that analysts are predicting. Overall, while DA Davidson’s lower Q3 earnings estimates for GROCERY OUTLET HOLDING Corp. may be cause for concern, it is important to keep in mind the company’s continued growth and expansion plans. Investors will be eagerly awaiting the company’s official earnings report for the quarter to see how they have fared during these challenging times. Live Quote…

Analysis

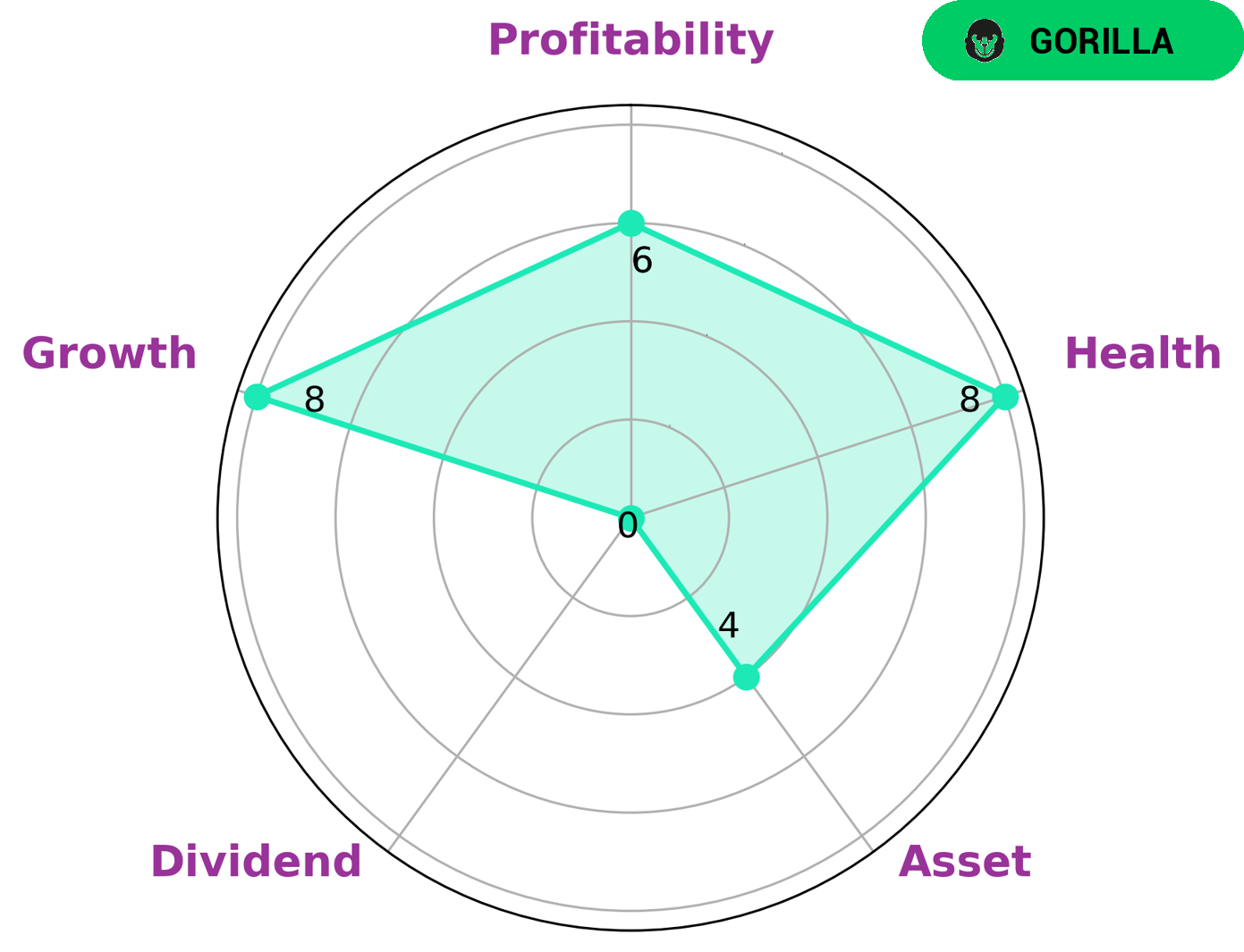

As a financial analyst, I have conducted an in-depth analysis of the financials of GROCERY OUTLET HOLDING. Overall, I can say that this company shows promising growth potential, with some areas of concern. First, let’s take a look at the company’s performance in terms of its star chart. This chart evaluates a company’s financial health based on four key areas: growth, asset, profitability, and dividend. According to the star chart, GROCERY OUTLET HOLDING is strong in growth, indicating that it has been able to increase its revenue and earnings in recent years. However, it is only average in terms of its asset and profitability, which could be improved. On the other hand, it is weak in terms of dividend, meaning that it may not be the best choice for investors seeking regular income from their investments. Moving on to the company’s health score, which takes into account its cash flows and debt, GROCERY OUTLET HOLDING scores an impressive 8 out of 10. This high score indicates that the company is capable of withstanding financial challenges and sustaining its operations even in times of crisis. This is a positive sign for investors as it shows that the company is financially stable and well-managed. Based on our analysis, GROCERY OUTLET HOLDING falls under the category of a “gorilla” company. This means that it has a strong competitive advantage and has achieved stable and high revenue or earning growth. This could be attributed to factors such as its unique business model or market dominance in its industry. Such companies are often considered attractive by investors as they have a proven track record of success and are expected to continue performing well in the future. In conclusion, GROCERY OUTLET HOLDING may be a good choice for investors looking for growth potential and stability. Its strong financial health and competitive advantage make it an attractive investment option. However, investors seeking regular dividends may need to consider other options. As always, it is important to conduct thorough research and consult with a financial advisor before making any investment decisions. More…

Peers

The company was founded in 1946 and is headquartered in Emeryville, California. Grocery Outlet Holding Corp operates through two segments: Grocery Outlet and Bargain Market. The Grocery Outlet segment offers a variety of food and household products at discounts of up to 50% off traditional grocery store prices. The Bargain Market segment offers a selection of closeout, overstocked, and irregular merchandise at discounts of up to 70% off traditional retail prices. The company competes with Veroni Brands Corp, The Kroger Co, and Ollie’s Bargain Outlet Holdings Inc.

– Veroni Brands Corp ($OTCPK:VONI)

As of 2022, Veroni Brands Corp has a market cap of 47.4M. The company’s return on equity is 98.41%. Veroni Brands Corp is a food and beverage company that manufactures and markets a variety of food and beverage products. The company’s products include pasta, sauces, snacks, and desserts. Veroni Brands Corp is headquartered in New York, New York.

– The Kroger Co ($NYSE:KR)

The Kroger Co has a market cap of 33.33B as of 2022, a Return on Equity of 23.61%. The company is a leading grocery store chain in the United States with over 2,800 stores in 35 states. The company offers a wide variety of products and services including grocery, health and beauty, and general merchandise. Kroger also has a strong online presence with a website and mobile app that offer convenient shopping options for customers.

– Ollie’s Bargain Outlet Holdings Inc ($NASDAQ:OLLI)

Ollie’s Bargain Outlet Holdings Inc is a publicly traded company with a market cap of 3.37B as of 2022. The company operates a chain of closeout retail stores in the United States. As of February 2021, the company operated 259 stores in 27 states. The company was founded in 1982 and is headquartered in Harrisburg, Pennsylvania.

Summary

Grocery Outlet Holding Corp. (GO) saw a decrease in their Q3 2024 earnings per share estimates, according to research analysts at DA Davidson. Despite this decrease, the stock price for GO actually increased on the same day. This suggests that investors may have confidence in the company’s long-term growth potential, even if there may be short-term challenges. Overall, it is important for investors to closely monitor earnings estimates and the stock price movement of GO to make informed decisions about their investments.

Related Posts

Recent Posts

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Investing Everyone Can Do.

Investing shouldn’t be exclusive to a select few. We believe everyone should have the opportunity to grow their wealth. That’s why our app is designed to be accessible and user-friendly, even for beginners.