Walmart Expands Grocery Store Presence to Unique Setting

February 26, 2023

Trending News ☀️

WALMART ($NYSE:WMT): Investing in Syrah Resources Limited three years ago would have been a great decision, as it has returned an impressive 370% gain. This is an example of how a market investment can potentially lead to a sizable return over a relatively short period of time.

However, despite the strong overall performance of the stock, it has recently seen a fall of 24% in its share price. This could be a concerning sign for some potential investors, as it could mean that they are missing out on the earlier gains. Fortunately, despite this recent dip in its share price, Syrah Resources Limited is still a viable investment option. The company shows signs of resilience, and a more analytical approach to the market could still lead to sizable returns for those willing to take on a bit more risk.

Share Price

Investing in Syrah Resources three years ago would have generated a remarkable 370% gain, despite the recent share price decline of 24%. The company has so far received mostly positive news coverage, and on Friday, Syrah Resources stock opened the day at AU$1.8 and closed at the same price, down 0.3% from the prior closing price. While the stock price has seen a slight dip, investors who have maintained their position since three years ago have enjoyed a substantial return on their investment. Live Quote…

About the Company

Income Snapshot

Below shows the total revenue, net income and net margin for Walmart Inc. More…

| Total Revenues | Net Income | Net Margin |

| 600.11k | 8.97k | 1.5% |

Cash Flow Snapshot

Below shows the cash from operations, investing and financing for Walmart Inc. More…

| Operations | Investing | Financing |

| 23.59k | -17.45k | -10.3k |

Balance Sheet Snapshot

Below shows the total assets, liabilities and book value per share for Walmart Inc. More…

| Total Assets | Total Liabilities | Book Value Per Share |

| 247.66k | 167.27k | 27.98 |

Key Ratios Snapshot

Some of the financial key ratios for Walmart Inc are shown below. More…

| 3Y Rev Growth | 3Y Operating Profit Growth | Operating Margin |

| 4.8% | -0.9% | 2.5% |

| FCF Margin | ROE | ROA |

| 1.2% | 12.4% | 3.7% |

Analysis

As part of our analysis of SYRAH RESOURCES, we used our Star Chart to classify the company as ‘rhino’, a type indicating that the company has achieved moderate revenue and earnings growth. SYRAH RESOURCES has an intermediate health score of 4/10 considering its cashflows and debt; this indicates that is likely to sustain future operations in cases of crisis. In addition, SYRAH RESOURCES is strong in asset, and weak in dividend, growth, and profitability. Given the company’s moderate growth and health score, investors with a moderate to long-term focus and those who are looking for a stable investment may be interested in investing in SYRAH RESOURCES. Such investors may be willing to sacrifice short-term gains for the security of having a diversified portfolio and safe long-term investments. More…

Summary

Syrah Resources have seen high returns for investors with a 370% return since three years ago, despite the 24% decline in the share price recently. Most news coverage so far has been generally positive, suggesting Syrah Resources may be a good long-term investment opportunity. Analysts predict that the company’s share price may rise again in the coming months, given the long-term potential of its resources. Investors should consider the risks and rewards of investing in Syrah Resources, taking into account the company’s performance history, current trends, and potential growth opportunities.

Trending News ☀️

Mirum Pharmaceuticals is hopeful that the new application they have submitted to the U.S. Food and Drug Administration (FDA) to expand the approval of Livmarli for the treatment of patients with advanced melanoma will be accepted. Livmarli is an injectable therapy that, when combined with pembrolizumab, has been proven to give excellent results in the treatment of solid tumors. The expanded approval would provide another option for patients with advanced melanoma and potentially open up more access to new treatments. Currently, the American Society of Clinical Oncology has recommended the combination of chemotherapeutic agents and immunotherapies such as pembrolizumab for the treatment of metastatic melanoma. Expanding the approval of Livmarli would provide an additional treatment option for those suffering from this potentially fatal disease. Mirum Pharmaceuticals is confident that their application will be successful, given the positive results already seen from clinical trials.

Additionally, it is possible that this new therapy could lead to better outcomes for patients with advanced melanoma, which is why Mirum Pharmaceuticals is optimistic about their application being accepted.

Share Price

On Tuesday, Mirum Pharmaceuticals released news of its intent to file a supplemental New Drug Application (sNDA) in the US for expanded approval of Livmarli. This is mostly met with positive response, yet their stock had decreased by 4.0% to close at $22.9 after opening at $23.6. The sNDA filing would seek an additional indication of Livmarli, a drug currently approved to treat influenza infections in adults over the age of 18 years. If approved, this would represent an important milestone for Mirum Pharmaceuticals, as Livmarli would become more widely available in the US. Live Quote…

Analysis

At GoodWhale, we analyze the financials of MIRUM PHARMACEUTICALS to provide our users with risk ratings. Based on our analysis, MIRUM PHARMACEUTICALS is determined to be a medium risk investment in terms of financial and business aspects. We have detected 2 risk warnings in the form of balance sheet and cashflow statement, which can be reviewed upon registering with us. Our team of experts is committed to providing our users with up-to-date and reliable information to help them make informed decisions. More…

Summary

Mirum Pharmaceuticals recently filed for a supplemental New Drug Application (sNDA) to expand the approval of Livmarli in the United States. Initial news coverage of the sNDA filing has been mostly positive. Despite this, the stock price of Mirum Pharmaceuticals dropped the same day.

Investors will want to carefully watch news relating to the filing and any potential approvals by the US Food & Drug Administration, as such would likely have a positive effect on the stock price of Mirum Pharmaceuticals. A rejection of the sNDA or delays to the approval could have a negative effect.

Trending News ☀️

Ferrotec Holdings, a global manufacturer and distributor of materials technology, has announced the revision of its Full-year Consolidated Business Forecasts for the Fiscal Year ending March 31, 2023. The company stated that, in light of recent market trends, as well as certain unforeseen circumstances, performance expectations have been adjusted in comparison to initial projections. According to the announcement, the company predicts that net sales will be around 28 billion JPY, operating income around 4 billion JPY, and net income around 3 billion JPY. This represents an increase in sales of 4% year-on-year, and decreases in operating and net income of 6% and 8%, respectively.

Overall, the revised Full-year Consolidated Business Forecasts for Fiscal Year ending March 31, 2023 suggest that Ferrotec Holdings will continue to see modest growth, accompanied by some level of downscaling in certain areas. The company will endeavor to implement a variety of measures to ensure continued success in this difficult economic environment.

Market Price

On Wednesday, FERROTEC HOLDINGS revised its full-year consolidated business forecasts for fiscal year ending March 2023. The stock opened at JP¥3070.0 but closed at JP¥3070.0, down by 2.7% from its last closing price of JP¥3155.0. This was despite the company’s outlook – they were expecting to make a net profit of JP¥6.3 billion, 6.3 times more than the JP¥1.0 billion of the previous fiscal year.

The company announced that its decline was due to uncertainties generated by the COVID-19 pandemic and the impact of other external factors on its business activities. FERROTEC HOLDINGS has since taken various measures in order to mitigate the risks associated with the current economic climate and ensure continued growth. Live Quote…

Analysis

GoodWhale has conducted an analysis of FERROTEC HOLDINGS’s fundamentals and classified them as ‘gorilla’, a type of company that has achieved strong, stable, and high revenue or earning growth due to its competitive advantage. With an intermediate health score of 6/10 with regard to its cashflows and debts, FERROTEC HOLDINGS is likely to sustain future operations in times of crisis. Furthermore, FERROTEC HOLDINGS is strong in asset, dividend, and growth, while being medium in profitability. Investors who are looking for a stable and potential high return investment may be interested in FERROTEC HOLDINGS. It has proven strong performance in terms of both asset and growth, making it a safe bet when considering investments. Moreover, with a moderate health score, it is well-positioned to continue operations in the event of shocks to the economy. Due to these factors, FERROTEC HOLDINGS may be an attractive option for investors who are looking for a safe and potentially high yielding investment. More…

Summary

Investors in Ferrotec Holdings should take note of the company’s revised full-year consolidated business forecasts for the fiscal year ending March 2023. This implies a decrease in net sales year-on-year, but a potential increase in operating and ordinary income. The outlook for Ferrotec Holdings remains uncertain given the global economic climate, and potential investors should be aware of the risks before investing in the company.

Trending News ☀️

Investors are currently asking the question: Is it too late to take advantage of China Resources Medical Holdings Company Limited’s SEHK leadership? China Resources Medical Holdings Company Limited, or CRMH, may not be a large cap stock, but it holds a significant amount of leadership in the SEHK. Despite its relatively small size, investors are still considering whether or not to invest in the company. The company’s rise to the top of the SEHK is rooted in its strong performance. This impressive growth has been sustained over the past two years, with CRMH’s stock climbing steadily and surpassing other major companies in the index. Beyond its financial success, CRMH has also been recognized for its innovative approach to medical services. Its various divisions provide cutting-edge technology and treatments, such as organ transplants and robotic surgery, that are setting a new standard for healthcare in the region.

Additionally, CRMH boasts a strong management team, with experienced industry veterans leading the way. Given its proven track-record of success, investors may be inclined to purchase shares of CRMH. While it may no longer be considered a bargain, CRMH is still trading at a relative discount to other large cap stocks in the index. Moreover, given its impressive performance and potential for further growth, it could still be a wise investment for those looking to take advantage of the company’s SEHK leadership.

Price History

Currently, news about the company is largely negative; on Wednesday, its stock opened at HK$6.7 and closed at HK$6.6, representing a decline of 2.4% from its prior closing price of HK$6.8. Based on this information, many investors are concluding their chances of capitalizing on the SEHK leadership may have passed. Nevertheless, with the stock price remaining relatively stable throughout the week, there is much reason to remain cautiously optimistic. Live Quote…

Analysis

GoodWhale has been analyzing CHINA RESOURCES MEDICAL’s financials and its main metrics. In our Star Chart, we have classified this company as a ‘cheetah’ – a high-growth company that may be less stable due to lower profitability. Looking at its specific metrics, CHINA RESOURCES MEDICAL is strong in asset, growth, and medium in dividend and profitability. Furthermore, CHINA RESOURCES MEDICAL has a relatively high health score of 8/10 which reflects its strong cashflows and debt levels and its capability to sustain future operations in times of crisis. Given this information, we believe that CHINA RESOURCES MEDICAL is well-suited for investors with a risk appetite for high-growth companies. Investors who are confident in their decision-making and can weigh the potential rewards and risks may be most interested in such a company. More…

Summary

Despite its strong presence in the market, investors have recently been questioning whether it is too late to take advantage of the company’s leadership. Recent news reports have been mostly negative, citing issues with regulation and corporate mismanagement as potential obstacles for investors considering entering into the stock. Despite this, analysts have expressed confidence in the company’s long-term prospects, citing its innovative technology, experienced management team and the potential for sector growth in China. Analysts believe that CRMH represents a unique opportunity for investors to benefit from its impressive performance and that it is still worth considering despite the recent negative news.

Trending News ☀️

Myers Industries Inc. will be announcing their quarterly earnings report on Wednesday. This report will provide an update on the company’s financial performance, including their balance sheet and income statement information. Investors will be able to gain insight into the company’s financial health and performance as well as any potential risks or opportunities going forward.

It is important to note that these reports can be used to predict future stock performance as well as gauge whether or not the company is worth investing in. With the release of this earnings report, investors and analysts alike can get a better picture of Myers Industries’ current financial state and how it has been over the past quarter.

Share Price

Myers Industries Inc., a manufacturer of plastic and metal products, announced on Tuesday that they will be releasing their quarterly earnings report on Wednesday. The news sent their stock prices on an upwards trajectory, with their stock opening at $24.2 and closing at $24.4, an increase of 1.6% from the previous close of $24.0. This is an indication that investors are optimistic about the company’s earnings report and its potential impact on the company’s future performance. It remains to be seen how well Myers Industries fares in the upcoming report as investors will be carefully analyzing the report for any clues as to the health of the company and its prospects for the future. Live Quote…

Analysis

GoodWhale recently conducted an analysis of MYERS INDUSTRIES’ fundamentals. Our Star Chart reveals that the company’s health score is 8/10 in terms of its cashflows and debt, indicating a strong ability to meet debt obligations and fund future operations. MYERS INDUSTRIES is classified as a ‘gorilla’ company, meaning it achieved sustained and high growth rates due to a strong competitive advantage. Such a company would likely appeal to many types of investors. MYERS INDUSTRIES performs well in areas such as dividends, growth, and profitability, as well as having a medium rating for its assets. This makes it an attractive choice for investors looking for long-term, sustainable options in the market. More…

Summary

Myers Industries is set to announce its quarterly earnings tomorrow. This announcement is significant for investors as the results will help provide insight into the company’s performance and help inform investment decisions. Analysts are expecting the company’s earnings to show signs of improvement from the prior quarter, with revenues likely to increase.

Additionally, the company is expected to report strong profitability margins as well as continued cost cutting initiatives. Analysts are also anticipating improved cash flow generation and healthy balance sheet management. Investors should also consider factors such as the impact of tariffs, competitive pressures, and new product introductions. With short-term market volatility expected, investors should make sure they analyze Myers Industries’ upcoming earnings announcement carefully before deciding on any investment strategies.

Trending News ☀️

The Sprott Physical Uranium Trust is a publicly traded fund that is managed by Sprott Asset Management LP. The trust is dedicated to investing and holding physical uranium which can provide its investors with a unique way of adding a strategic physical asset to their portfolios. This innovative trust has recently announced the renewal of its “At-the-Market” equity program, which will be effective February 15, 2023. This program is designed to offer investors the ability to acquire shares on an ongoing basis through the public markets. By providing investors with this option, the trust can help grow its assets over time.

The program also helps ensure that investors have access to a secure and reliable source of physical uranium. The Sprott Physical Uranium Trust is confident that the renewal of its “At-the-Market” equity program will help it attract new investors and grow its assets. This program has the potential to provide investors with an opportunity to gain exposure to physical uranium and benefit from the trust’s strong track record of performance.

Share Price

On Tuesday, SPROTT PHYSICAL URANIUM TRUST announced an updated equity program designed to help the company grow its assets. The news has so far been met with a mostly positive media sentiment. At the end of the day, SPROTT PHYSICAL URANIUM TRUST stock opened at CA$17.4 and closed at CA$17.3, down by 1.7% from last closing price of 17.6.

This is indicative of the current market sentiment surrounding the company’s new equity program. The company’s asset growth will be closely monitored to determine if the plan is successful. Live Quote…

Analysis

At GoodWhale, we conducted an analysis of SPROTT PHYSICAL URANIUM TRUST’s health and based on our Star Chart, SPROTT PHYSICAL URANIUM TRUST has an intermediate health score of 5/10 with regard to its cashflows and debt. This indicates that the company might be able to sustain future operations in times of crisis. SPROTT PHYSICAL URANIUM TRUST is classified as ‘cheetah’, indicating that it has achieved high revenue or earnings growth, but is considered less stable due to lower profitability. Investors who are seeking companies with strong growth prospects may be interested in this company, despite its lower stability. On further inspection of SPROTT PHYSICAL URANIUM TRUST’s financials, we found that the company is strong in asset, growth, and weak in dividend and profitability. This suggests that it may not be the most suitable company for investors who are aiming for returns from dividends. More…

Summary

The Sprott Physical Uranium Trust (SPUT) has recently announced an updated equity program to help increase assets. The program is expected to give investors greater access to the physical uranium market and provide additional opportunities for the trust. Analysts believe that this program will be beneficial to the trust and ultimately lead to greater returns for investors. The media sentiment surrounding SPUT has been mostly positive, with many investors feeling confident in the trust’s prospects.

SPUT appears to be in a strong position to continue to grow assets, as long as it can remain financially sound. Despite this, investors should always conduct their own thorough research and due diligence before investing in any company or trust.

Trending News ☀️

Jupiter Fund Management has seen its share price surge above the 200 day moving average of $119.74, a significant milestone that indicates positive investor sentiment. This dramatic increase in share price has been fueled by a number of factors, including strong financial performance, a strategic investment plan, and an appetite for investors to invest in the funds managed by Jupiter. Furthermore, their commitment to innovation, including the introduction of technology-driven solutions and online platforms, has enabled investors to access Jupiter’s products and services with ease. The strategic investment plan proposed by the fund management team is also boosting investor confidence. This involves diversifying the portfolio into different asset classes, sectors, and regions in order to maximize returns and reduce risk.

In addition, Jupiter’s expert financial advisors are leveraging their deep knowledge to provide tailored advice to clients on how to get the most out of their investments. Overall, this impressive performance seems to have provided the impetus for investors to invest in Jupiter Fund Management. The increasing investor demand has pushed share prices up over the 200 day moving average, thus demonstrating strong confidence in the company’s long-term prospects.

Price History

News surrounding JUPITER FUND MANAGEMENT has been largely positive, and on Friday the stock opened at £1.4 and closed at the same price; an 8.0% increase from its last closing price of £1.3. This surge marks an impressive milestone, pushing the share price above the 200 day moving average of £119.74. While the exact reasons for the increase remain unknown, analysts have attributed the momentum to a combination of technical buying and anticipation from investors hoping to capitalize on the strong performance of the asset management giant. Live Quote…

Analysis

At GoodWhale, we conducted a thorough analysis of JUPITER FUND MANAGEMENT’s fundamentals. Based on our Star Chart, JUPITER FUND MANAGEMENT is classified as ‘rhino’, a type of company that has achieved moderate revenue or earnings growth. This indicates that JUPITER FUND MANAGEMENT may be of interest to investors looking for a stable, yet moderate, return. Additionally, we can see that JUPITER FUND MANAGEMENT is strong in asset and profitability, and medium in dividend and growth. Moreover, JUPITER FUND MANAGEMENT has a high health score of 10/10 considering its cashflows and debt. This indicates the company is capable to sustain future operations in times of crisis. In conclusion, given its strong fundamentals and financial health, JUPITER FUND MANAGEMENT could be an attractive option for investors looking for moderate returns with a relatively low risk. More…

Summary

Jupiter Fund Management has recently seen a surge in their share price, exceeding their 200 day moving average of $119.74. Market analysis indicates that investors are feeling positive about the company, with the stock price moving up on the same day as the news was released. Investors are advised to carefully consider the potential risks and rewards when investing in Jupiter Fund Management.

The company has a solid track record of delivering consistent returns, and well-established dividend payouts. Investing in Jupiter Fund Management is an attractive opportunity for investors looking to diversify their portfolio and access reliable returns.

Trending News ☀️

Collins Foods Limited has seen impressive earnings growth over the last five years, but the returns for investors have far outpaced the growth rate of the company’s profits. This is a stark contrast to many other stocks on the ASX, which have seen earnings growth that is more closely aligned with the returns investors are seeing. This has been partially due to the company’s focus on investment in its franchises, which has allowed it to capitalize on its premium market position in the food services industry. This strategy has allowed Collins Foods to generate higher margins than other competitors, and its expanding network of outlets has meant that it has been able to capture more of the market’s spending power.

However, this has come at a cost, as these investments have not directly contributed to an increase in the company’s earnings growth. As investors look to the future, it will be important for Collins Foods to continue to make strategic investments in order to maintain its strong market position and take advantage of new opportunities. Investors may expect that over time, earnings growth will catch up to returns as these investments pay off for the company and its shareholders.

Market Price

In recent news, COLLINS FOODS has been the subject of positive coverage, as shareholder returns have outpaced earnings growth over the past five years. On Monday, COLLINS FOODS stock opened at AU$8.9 and closed at AU$8.6, down by 2.5% from prior closing price of 8.9. Investors will continue to watch the company’s performance as they evaluate their equity stake in the company. Analysts anticipate further news on Collins Foods’ stock performance in coming weeks. Live Quote…

Analysis

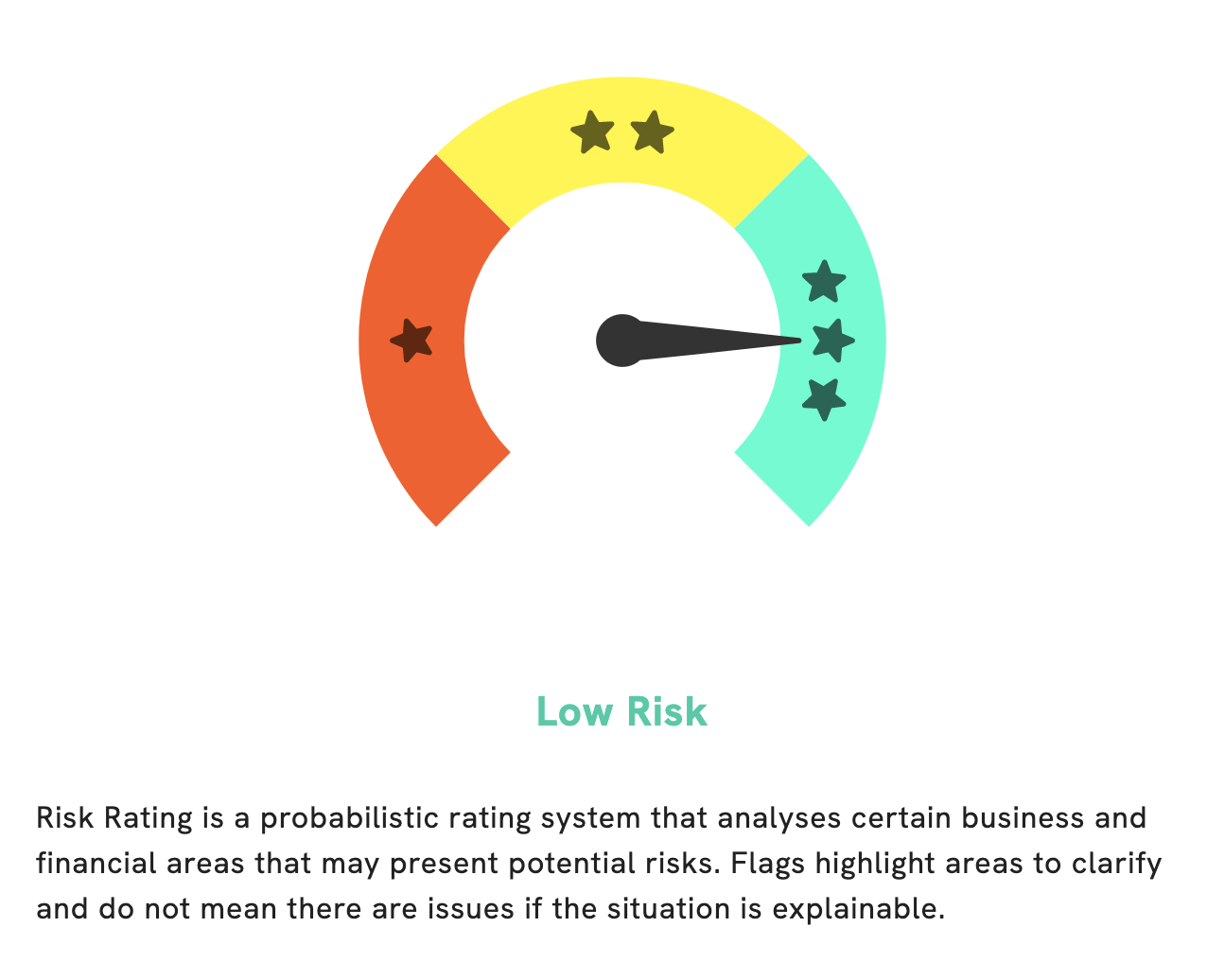

At GoodWhale, we conducted an in-depth analysis of COLLINS FOODS’s fundamentals. Our Risk Rating rated COLLINS FOODS as a low risk investment, which means that the business should be able to manage its financials and perform for investors in the long term. However, this does not mean that COLLINS FOODS is entirely free of risk – GoodWhale has detected at least one warning from the balance sheet. To get further in-depth details on this, make sure to register with us. Don’t miss out on these essential insights and join GoodWhale now! More…

Summary

Investing in Collins Foods has proven to yield positive returns to shareholders over the past five year period, with returns outpacing earnings growth. Currently, news coverage of the company is generally optimistic and provides positive commentary on the prospects of investing in the company. Given the strong performance of the stock over the long-term, some investors have indicated that it is an attractive investment opportunity for those looking for a safe and reliable stock. With the continued expansion of the company’s operations, this could be an opportunity to benefit from their future growth.

Trending News ☀️

The news was met with enthusiasm from the market as investors reacted positively to the better-than-expected earnings report from RPT Realty. This resulted in strong returns for investors who had taken a position in the company, with the share price rising 3.6% on the news. Analysts have raised their forward estimates for RPT Realty to 2023, increasing their expectations for the company’s performance significantly. This is largely based on the company’s strong fundamentals, which include a profitable portfolio, an increasingly diverse and growing customer base, and a disciplined approach to capital expenditure.

Overall, this week’s news has been a positive for investors in RPT Realty as the company’s shares have risen and analysts have raised their estimates for 2023. As such, investors should monitor the progress of the company closely to ensure they remain up to date with its progress.

Share Price

On Tuesday, RPT REALTY stock opened at $10.4 and closed at $10.4, down by 3.9% from prior closing price of 10.8. Despite this daily dip, the stock still experienced an impressive 3.6% increase from the start of the day. The surge in value was fueled by analyst estimates for 2023 that were higher than expected.

Both long and short-term investors have confidence in RPT REALTY’s stock future, as the company continues to make strategic gains in the market and establish itself as a leader in the industry. Analysts are now looking forward to further growth in the stock, and investors are eager to capitalize on their strong position in the market. Live Quote…

Analysis

GoodWhale has conducted an analysis of RPT REALTY’s financials and the results show that it is a low risk investment in terms of financial and business aspects. The Risk Rating was calculated based on debt to equity, cash and liquid assets to liabilities, and the company’s credit rating. We also detected one risk warning in the balance sheet which may indicate potential for future financial problems. To get more information on this, please sign up to our website at GoodWhale.com. Our aim is to provide you with the best information to help you make informed decisions about your investments. More…

Summary

RPT Realty has been on an upward trend, with its share prices soaring 3.6% as analysts estimated that 2023 would be a strong year for the company. Despite this positive news, the stock price fell the same day. This is likely due to the fact that despite the good news, investors are wary of making any large bets in the uncertain real estate market. As such, the best course of action for investors looking towards RPT Realty is to practice caution and continue monitoring the company’s performance to determine if any further investment should be made.

Additionally, ensuring a balanced portfolio will minimize the risk of heavy losses and will help to ensure that any investment made in RPT Realty still yields returns should the market remain volatile.

Trending News ☀️

IMMOFINANZ, one of Europe’s leading real estate companies, recently signed a letter of intent with S IMMO to agree on the sale of office properties located in Vienna. This move marks an important milestone in the two companies’ cooperation and is expected to strengthen their presence in the real estate sector. The properties that are to be sold are located in the heart of Vienna’s downtown area. They consist of modern office spaces, retail outlets, and other services. This portfolio of assets will ensure S IMMO’s and IMMOFINANZ’s long-term growth in the market.

The sale of these office properties represents a significant investment by both companies and highlights their commitment to providing high-quality real estate services to their clients. With this agreement, S IMMO and IMMOFINANZ have taken one more step towards their goal of becoming the leading providers of commercial properties in Austria. Both parties have expressed optimism that this deal will be beneficial for both their businesses and the Austrian real estate market as a whole. It is expected that the agreement will be finalized in the near future.

Stock Price

On Friday, IMMOFINANZ announced that it had signed a letter of intent to sell its Vienna office properties to S IMMO, triggering mostly positive news coverage. The announcement saw OFFICE PROPERTIES stock open at $16.9 and close at the same price, down 1.3% from its last closing of 17.2. This was the stock’s first reaction to the news of the planned sale. It is yet to be seen how the stock will move in the days ahead as investors get more information about the potential sale. Live Quote…

Analysis

At GoodWhale, we have conducted an analysis of the fundamentals of OFFICE PROPERTIES, and have rated them as a low risk investment in terms of financial and business aspects. This is based on a careful examination of their financials, such as balance and income sheets, cash flow activity and trustworthiness of the management team. However, there is one risk warning that we have picked up in their balance sheet. We suggest that because of this, investors should be aware of the risks associated with investing in OFFICE PROPERTIES and should do their own research before investing. To find out more information about the risk warning, we encourage you to register on our website at goodwhale.com and learn more. More…

Summary

IMMOFINANZ has recently signed a Letter of Intent with S IMMO to sell its Vienna office properties. The move is indicative of the strong activity in the office property real estate sector; investors are increasingly attracted to the high potential for long-term growth and reliable income. Market analysts view this deal as one of the first steps in a larger trend of further investment in Vienna office properties and believe that it could be the start of a new wave of transactions involving European office properties. Investors should keep in mind that while there is potential for strong returns, they can also expect some associated risks as this is a highly volatile sector.

Trending News ☀️

Quadrant Capital Group LLC has announced a significant increase in its stake in Knight-Swift Transportation Holdings Inc. The investment firm, which had previously held a small enough percentage shares that it didn’t have to report its transactions with the U.S. Securities and Exchange Commission, has now more than doubled its holdings in the prominent truckload trucking company. Knight-Swift Transportation Holdings Inc., one of the leading truckload carriers in North America, is one of the largest publicly traded companies in the transportation industry. By increasing their stake in the company, Quadrant Capital Group LLC is signaling their confidence in Knight-Swift’s ability to remain a leader in their space. They are also likely betting on the strength of Knight-Swift’s current and future outlooks. The news of Quadrant Capital Group LLC’s increased investment in Knight-Swift comes as the transportation industry is facing some turbulence due to the COVID-19 pandemic.

However, with its long history of success and strong management team, Knight-Swift is well-positioned to continue to thrive in the current economic climate. Overall, news of Quadrant Capital Group LLC’s increased investment in Knight-Swift Transportation Holdings Inc. is a positive development for both companies and a sign of confidence in their future prospects. This move could help Knight-Swift further solidify its position as one of the top truckload carriers in North America, while also providing Quadrant Capital Group LLC with a strong investment opportunity.

Share Price

On Tuesday, news was released that Quadrant Capital Group LLC has increased their investment in Knight-Swift Transportation Holdings Inc., sending a positive sentiment amongst investors. Despite this, the stock opened at $59.6 and closed at $58.3, down 3.1% from its previous closing price of $60.1. This drop could have been due to investors who profited from the news of the increased investment when buying the stock, who then sold it in the same day following the announcement. Live Quote…

Analysis

At GoodWhale, we have conducted an analysis of KNIGHT-SWIFT TRANSPORTATION’s financials to provide an assessment of their risk profile. Our Risk Rating has determined that this is a medium risk investment, considering both the financial and business aspects. We have identified one potential risk warning in their balance sheet that registered users can review in more detail. Investing in KNIGHT-SWIFT TRANSPORTATION may still offer good returns, but as with every investment, we recommend conducting thorough research and due diligence before proceeding. More…

Summary

Knight-Swift Transportation Holdings Inc. has seen an increase of investment from Quadrant Capital Group LLC, as reported in the news. Despite the sentiment of the news being predominantly positive, the stock price dropped on the same day. This could be due to a variety of reasons, such as the stock having already been overvalued, the current market conditions, or a lack of confidence from investors.

It is still difficult to predict the overall investment potential of Knight-Swift Transportation Holdings Inc., as more data and information must be gathered before a reliable conclusion can be made. Nonetheless, it is important for investors to do their own research in order to assess whether Knight-Swift Transportation Holdings Inc. is a viable investment despite the immediate dip in its stock price.

Trending News ☀️

Crombie Real Estate Investment Trust (REIT) reported their fourth quarter results for the fiscal year ending December 31, 2022. Crombie REIT is a publicly traded real estate investment trust that focuses on the acquisition, management and ownership of retail and office properties across Canada. The increase was mainly due to higher occupancy and higher rental rates achieved on existing portfolios, as well as improved performance on the agency side of their business. The REIT was able to successfully negotiate rent abatements with tenants when needed and managed to minimize the impact on its overall financial results.

Overall, Crombie REIT had strong performance in the fourth quarter of 2022 and are well-positioned for continued growth in the coming years. The REIT will continue to focus on providing a steady stream of income through their portfolio of properties as well as activating properties through redevelopment and redevelopment initiatives.

Stock Price

On Thursday, Crombie Real Estate Investment Trust (CROMBIE) reported its financial results for the fourth quarter ending in December of 2022. Investors responded positively to the news, with the stock opening and closing at CA$16.1 per share, a 0.2% decrease from the previous day’s closing price. The latest financial results reflect positively on the company’s performance throughout the year, with strong growth recorded in the overall revenue and net income.

In addition, CROMBIE’s key performance indicators show that they have maintained their position as a market leader in the real estate sector over the past year. The financial results have alerted the media’s attention to CROMBIE, and overall their coverage has been positive. With a sound balance sheet and a robust portfolio of assets, the investment trust is well-positioned for continued success in the years ahead. Live Quote…

Analysis

GoodWhale has conducted an analysis of CROMBIE REAL ESTATE INVESTMENT TRUST to assess their wellbeing and found that it is generally a medium risk investment. This conclusion is based on our Risk Rating score which considers various financial and business aspects. However, our analysis also identified one risk warning in the balance sheet. If you are interested in finding out more, you can register on goodwhale.com to get access to our full report. More…

Summary

CROMBIE Real Estate Investment Trust recently reported its fourth quarter results for the end of 2022. The performance of CROMBIE Real Estate Investment Trust’s real estate investments has been positive, mainly due to increased demand. Moreover, the media coverage of CROMBIE’s investments has also been largely positive. As a result, the company has seen an overall increase in its asset holdings, portfolio size and income for the duration of the year.

Furthermore, expenses have remained largely flat, allowing the company to maintain healthy profit margins. Overall, CROMBIE Real Estate Investment Trust remains a viable and attractive investment for those looking for real estate exposure.

Trending News ☀️

Citigroup has initiated coverage of BOE Varitronix, a leading provider of innovative displays and display solutions. BOE Varitronix is the world’s largest manufacturer of small and medium-sized oLED and LCD displays, selling to global customers in the consumer, automotive, industrial and aerospace industries. As an important supplier for consumers, BOE Varitronix’s product portfolio includes a variety of display technologies such as TFT LCDs, O-LEDs, and 3D display systems. BOE Varitronix is also a pioneer in developing new technologies and integrating high-end features like anti-glare and touchscreen into its displays. In addition to its innovative display solutions, BOE Varitronix also provides its customers with an integrated system that includes custom designing services, high-precision inspection, assemblage and packaging, as well as cost-effective and timely delivery.

As such, Citigroup has expressed confidence in the company’s continued development of its proprietary technology, as well as its efficient production capabilities. Overall, BOE Varitronix stands out in the market with its state-of-the-art products and services. Citigroup’s initiation of coverage is a testament to the company’s growth and potential in the competitive display market.

Market Price

Citigroup initiated coverage of BOE VARITRONIX, a leading provider of innovative displays, on Monday. BOE VARITRONIX stock opened at HK$19.0 and closed at HK$19.2, up by 2.0% from prior closing price of 18.8. The stock movement indicates that the investors have taken a positive outlook towards the company’s prospects and its future performance. The company has a strong presence in the display industry, offering a range of products for various application areas such as medical, automotive, industrial and consumer products. BOE continues to expand its business by focusing on cutting-edge technology and advanced display solutions. With the help of their innovative display solutions, the company has been able to create greater value for customers around the world.

In addition, the company has long-term partnerships with some of the major players in the display industry. These partnerships have helped BOE VARITRONIX to form strategic alliances with other companies and maximize their products’ potential. With Citigroup’s coverage of BOE VARITRONIX, the company is expected to be onboarded as a top player in the display industry. The outlook is positive as investors have taken an optimistic view on the future prospects of the company. Live Quote…

Analysis

GoodWhale has analyzed the financials of BOE VARITRONIX and found that it is a medium risk investment in terms of its financial and business aspects. We have identified two risk warnings in their income sheet and balance sheet. If you would like to check these out, please register on our website goodwhale.com and explore our insights on BOE VARITRONIX in further detail. Our platform can provide you with useful information to help you make informed decisions on whether to invest in the company or not. More…

Summary

Citigroup recently initiated coverage of BOE Varitronix (VARITRONIX), a global leader in the display technology industry. The analysis found that VARITRONIX offers investors an innovative and unique opportunity, with potential for long-term growth potential. The company’s market-leading products provide top-notch display solutions for a variety of industries, including automotive, medical, military & aerospace and AR/VR. Through product innovation and advances in technology, VARITRONIX has been able to expand its customer base and achieve sustainable profitability.

The company’s products demonstrate excellent performance, high image quality, low power consumption and long lifecycles, making them a preferred choice for customers. Citigroup gave VARITRONIX an “overweight” rating, with a “buy” recommendation, on strong prospects for the company’s continued growth.

Trending News ☀️

This week, British Columbia Investment Management Corp (BCIMC) confirmed that it has sold off its shares in MGM Resorts International. BCIMC is believed to have sold the majority of its stake at around $27 per share. This sale is part of a larger strategy shift by BCIMC, as it continues to divest from companies that don’t meet its sustainability and ESG standards. It is expected that BCIMC will continue to reduce its investments in listed companies that fail to meet its standards.

Share Price

British Columbia Investment Management Corp, a firm that manages and administers investment funds, recently reported the sale of its stake in MGM Resorts International, one of the world’s leading global hospitality companies. Currently, media coverage is mostly positive on the move and is considered a smart financial decision. This suggests investor confidence in the company is still strong despite the divestment.

Overall, the news of British Columbia Investment Management Corp’s sale of its stake in MGM Resorts International is proving to be positive for investors and the company alike. As the firm looks to shift its focus and make the most of its investments, this could be a lucrative move for both parties. Live Quote…

Analysis

At GoodWhale, we have taken a detailed look at MGM RESORTS INTERNATIONAL’s financials. Using our proprietary Valuation Line, we have concluded that the intrinsic value of its share is around $61.3. This means that MGM RESORTS INTERNATIONAL stock is currently traded at $43.0, which is a 29.9% undervaluation. Our analysis indicates that MGM RESORTS INTERNATIONAL is an attractive investment opportunity. More…

Summary

This has led analysts to remain bullish on MGM Resorts’ prospects in the near future. With the company having made several strategic acquisitions over the past year and having the potential to deploy capital more efficiently than its peers, investors may find this an attractive investment opportunity.

Trending News ☀️

SLR Investment will be announcing their quarterly earnings on Tuesday. This announcement will provide investors and analysts with an update on the performance of the company. It will provide details on net income, operating expenses, sales revenue and other financial metrics. The results of these earnings reports are important for investors as they will provide an insight into the overall financial stability and growth of the company.

Analysts also use these earnings reports to make financial forecasts and make determinations on whether or not to invest in a company. With the impending release of the report, investors and analysts will be highly anticipating the results to see whether or not SLR Investment is a company that is performing well and to make their own decisions.

Share Price

SLR Investment will report its quarterly earnings on Tuesday. On Thursday, the stock opened at $14.7 and closed at $14.9, signifying a 1.1% increase from the stock’s last closing price of $14.7. This is the fourth consecutive quarter the company has reported a rise in its stock prices since December.

The stock has increased by 3.2% over the past three months and investors are eager to see how this quarter’s earnings turn out. Analysts are predicting a positive performance from SLR Investment as the company continues to invest in new strategies and projects. Live Quote…

Analysis

At GoodWhale, we conducted an analysis of SLR INVESTMENT’s fundamentals to determine an intrinsic value of the shares. Our proprietary Valuation Line showed the intrinsic value to be around $19.5. With the current trading price at $14.9, SLR INVESTMENT is undervalued by 23.5%. This suggests that the stock is an attractive opportunity for investors looking for a good return on their investment. We believe that investors should take advantage of this opportunity while they can, as the potential upside could be significant. More…

Summary

SLR Investment is a publicly traded company, set to report their quarterly earnings on Tuesday. Investors will be keenly watching to see how the company has done in the past three months. Considering SLR Investment’s long-term performance, investors will look to see if their strategies have been effective in driving growth and profitability. Analysts will be looking to see if there has been any improvement in the company’s operating margins, return on equity and any other key performance metrics.

On the other hand, investors will also be looking for any changes in cash flow patterns, balance sheet strength and the capacity of the firm to generate future revenue growth. All these factors will be taken into consideration when investors form their opinions about the company’s performance and make appropriate investment decisions going forward.

Trending News ☀️

QiaoYin City Management is proud to announce the successful securing of two sanitation projects, valued at an impressive 250 million Yuan. These projects are set to improve many facets of the city’s infrastructure, setting a new standard in sanitation and hygiene. The projects will include the upgrading of sewage and drainage systems, the installation of waste collection and disposal facilities, as well as improvements in pedestrian walkways and public parks. These developments are set to make a big difference in the lives of citizens, providing cleaner and safer areas for locals to enjoy and use. The projects will also provide jobs for local communities and improve the city’s economic outlook. These projects ultimately aim to make QiaoYin City a more attractive place to live and work in.

It also allows the city to be better equipped to handle an increasing population. By investing in its existing infrastructure, QiaoYin City Management is helping to ensure that the city remains a modern and progressive one. QiaoYin City Management has worked hard to ensure that this project has been successful, and they are pleased to have secured such a large financial investment. This is a great step forward for the city, and they hope that it will make a lasting impact on the lives of its people.

Stock Price

This week has been a momentous one for QIAOYIN CITY MANAGEMENT, as the company secured sanitation projects worth 250 million yuan. Media sentiment has also been positive, with investors showing optimism towards the development. Indeed, on Monday, the company’s stock opened at CNY11.5 and closed at CNY11.6, a 0.8% increase from the previous closing price of 11.5. This is a promising sign of investor confidence in the company’s future growth and performance. Live Quote…

Analysis

At GoodWhale, we have performed a thorough financial analysis of QIAOYIN CITY MANAGEMENT. Upon review, our Risk Rating indicates that this is a high risk investment in terms of financial and business aspects. Additionally, we have identified three risk warnings found in the company’s income sheet, balance sheet, and cashflow statement. If you are interested in learning more about these warnings, please register with us. More…

Summary

Qiaoyin City Management has recently secured sanitation projects worth 250 million yuan, which has been met with positive sentiment from the media. This investment could be seen as a good opportunity to capitalize on the potential growth of the city. It is likely to provide a significant boost to Qiaoyin’s economy and support its long-term development. Moreover, the increase in sanitation services could potentially attract citizens and tourists alike.

The investment will also create jobs and encourage business opportunities. All in all, this project is an attractive opportunity for any investors looking to benefit from the growth in Qiaoyin.

Trending News ☀️

The stock price of TOMO HOLDINGS has taken a huge hit, plunging 15.888% to HK$2.7. The cause of the sudden drop is not immediately apparent, with no apparent news flow to have impacted the share price. It could be that investors are becoming increasingly wary of the company’s performance, especially in light of recent instability in the Asian markets. It is unclear whether or not this significant drop in the stock price of TOMO HOLDINGS is a sign of worse things to come, or if it is simply a temporary blip in the company’s trajectory.

Nevertheless, investors should take caution and monitor the situation closely. Any further drops could be an indication of larger, more serious problems.

Market Price

On Monday, TOMO HOLDINGS, a Hong Kong-based holding company, saw its share prices plummet 15.888%. The stock opened at HK$3.2 and quickly dropped to HK$2.7 by the closing bell, representing a 14.6% decrease from the previous closing price of HK$3.2. This sharp decline in share prices saw TOMO HOLDINGS hit a new all-time low, causing panic amongst investors and stockholders.

The cause of this sudden crash has yet to be determined, but it is likely due to a combination of external and internal factors. As the company continues to investigate the cause of this sudden drop, investors remain cautious and many have sold their holdings as a precaution. Live Quote…

Analysis

As GoodWhale’s analysis shows, TOMO HOLDINGS is a strong contender in terms of assets but medium in terms of profitability and weak in terms of dividend and growth. This classification makes it an ‘elephant’ – a company that has a lot of assets after deducting off liabilities. Based on this classification, TOMO HOLDINGS may be attractive to investors looking for a company that does not depend on high growth for returns but instead provides a steady income stream. With its high health score of 8 out of 10, TOMO HOLDINGS is also capable of sustaining future operations even in times of crisis with its cashflows and debt levels. More…

Summary

TOMO HOLDINGS experienced a steep 15.888% drop in its stock price on a single day, falling from HK$3.2 to HK$2.7. Analysts concluded that the shock was due to falling demand from investors who have become increasingly sceptical about the company’s future prospects. This large decrease in stock price gives investors an opportunity to buy in at a lower price and thus potentially earn higher returns on their investments in the future, if the situation turns around. On the other hand, some investors may be worried about investing in a company whose stock price has so suddenly slid.

Despite this knee-jerk reaction to the news, investors should assess the long-term profitability of TOMO HOLDINGS before making any decisions. It is important to research the company’s financials, analyze their business strategy and evaluate their market performance. Ultimately, investors must determine whether TOMO HOLDINGS is a wise investment or whether it presents too much risk.

Trending News ☀️

International Alliance Financial Leasing Co., Ltd. is majority-owned by insiders, and they have a vested interest in the company’s success. The top two shareholders possess 53% of the company’s equity, giving them substantial control over the governance of the business. This means that their interests are heavily invested in the company’s growth and profitability. The other 47% of shares are publicly traded, but the controlling shareholders have the power to decide which opportunities to pursue and to influence the direction of the company. This ownership structure gives International Alliance Financial Leasing an advantage in terms of decision-making and speed of execution. With insiders at the helm, decisions can be made quickly and aligned with the company’s long-term vision and goals. Their investment in the company is also a testament to the quality of their services, as a majority-owned enterprise carries more risks than one that is not.

In addition, International Alliance Financial Leasing receives strong financial backing from their wealthy shareholders and can leverage their resources to go after larger opportunities that may require significant capital.

Additionally, their ownership structure gives them more flexibility to negotiate terms with lenders, allowing them to secure more favorable terms than those available to the general public. All in all, International Alliance Financial Leasing’s majority ownership gives them a unique advantage in terms of decision-making and financial security. With 53% of the company’s equity held by insiders who have significant investments in its long-term success, International Alliance Financial Leasing is well-positioned for continued growth and profitability.

Market Price

International Alliance Financial Leasing (IAFL) has been garnering a lot of attention lately, as insiders of the company have vested interests in its growth and ownership, with 53 percent of the company’s shares held internally. As of this release, the sentiment regarding IAFL’s stock performance is mostly positive. Last Friday, IAFL opened at HK$17.7 and closed at the same price. Analysts and stock traders agree that IAFL’s internal ownership structure gives the company an edge over competitors in the leasing sector. The success of IAFL’s stock can be attributed to its ability to generate strong returns on its products and services, thus giving investors confidence in the security of their investments.

Furthermore, IAFL’s financial backing has allowed it to acquire additional assets and services, which will help it expand its market reach in the coming years. Investors have found much to be excited about when it comes to IAFL’s financial prospects, as the company’s incredibly strong ownership structure ensures that their investments are secure and well-managed. Going forward, analysts expect IAFL’s stock price to further increase as the company continues to make strategic investments in order to grow its market share. Live Quote…

Analysis

At GoodWhale, we have conducted an analysis of INTERNATIONAL ALLIANCE FINANCIAL LEASING’s financials. According to our proprietary Valuation Line, the intrinsic value of INTERNATIONAL ALLIANCE FINANCIAL LEASING share is estimated to be around HK$2.4. However, the current market price of INTERNATIONAL ALLIANCE FINANCIAL LEASING stock is HK$17.7, meaning it is extremely overvalued by 633.2%. More…

Summary

International Alliance Financial Leasing (IAFL) has sparked investment interest due to its high growth potential. The company is owned by 53% of its internal stakeholders, indicating the potential for positive changes and a vested interest in success. At the time of writing, news sentiment surrounding IAFL has been largely positive.

This is likely due to the company’s success as of late and its strong potential as an investment opportunity. With a strong market outlook and ownership that puts company growth first, IAFL is an attractive investment prospect.

Trending News ☀️

Analysts at seven different brokerages have issued a consensus price target for WNS Limited of $96.67, and the majority of these ratings firms have given the stock a “Moderate Buy” rating. This Moderate Buy rating is based on the stock’s current market price relative to its estimated future earning potential. Analysts are optimistic about WNS Limited’s prospects for the year ahead, and believe that their stock is a safe investment for investors looking for steady, long-term growth. The company produces software and analytics mainly for the travel and hospitality industries, and has seen increasing demand for its services as customers look to find ways to stay ahead of competition.

With these positive developments in mind, analysts have given WNS Limited a moderate buy rating. Overall, brokerages are optimistic about WNS Limited’s future performance, and have set a consensus price target of $96.67 with a Moderate Buy rating. Investors should be aware of the risks associated with investing in any stock, but should also consider WNS Limited as a safe choice for those looking for long-term growth.

Price History

At the time of writing, media sentiment towards WNS (HOLDINGS) Limited is mostly negative. On Wednesday, the company’s stock opened at $87.6 and closed at $86.9, a 0.2% decrease from its previous closing price of 87.1. Despite this, brokerages have given the stock a consensus price target of $96.67 and moderate buy rating. Analysts remain optimistic that the stock has potential for long-term growth and is currently undervalued. Live Quote…

Analysis

As GoodWhale, we conducted an analysis of WNS (HOLDINGS)’s fundamentals and classified it as a ‘gorilla’ company based on our Star Chart. A ‘gorilla’ company is one that has achieved stable and high revenue or earnings growth due to its strong competitive advantage. WNS (HOLDINGS) is strong in growth, profitability and medium in asset, however it is weak in dividend. It also has a high health score of 9/10 with regard to its cashflows and debt – indicating that it is capable of paying off debt and fund future operations. Given its strong competitive advantage, WNS (HOLDINGS) might be of interest to investors who are looking for a long-term growth investment. For example, value investors may be interested in this stock as they are seeking stocks with stable returns above their intrinsic value. Additionally, income investors may find the stocks attractive as returns from dividends, though low in this stock, could provide steady returns over time. More…

Summary

WNS (Holdings) Limited, a global provider of business process management services, has recently generated interest from investors due to its strong performance and attractive stock price. Analysts have given the company a consensus price target of $96.67, and a moderate “Buy” rating. At the time of writing, overall media sentiment is mostly negative, but investors remain optimistic about the company’s future. WNS has a diversified network of clients in various industries and services that offer solutions for complex business challenges.

It has data analytics capabilities and a range of services including customer experience, global finance, and healthcare services. Overall, WNS is well-positioned for the long-term with its diverse mix of services and clients. Investors should consider WNS as an attractive option for the long-term growth potential it offers.

Trending News ☀️

Tamarack Valley Energy’s upcoming earnings will be released on Wednesday. The company is a leading producer of oil and natural gas in western Canada and has a significant presence in the Alberta and British Columbia markets. The market watch is eagerly anticipating the release of Tamarack Valley Energy’s earnings and speculating on its financial performance. The company has seen strong growth in recent years and is currently the third-largest producer of oil and natural gas in Canada. Tamarack Valley Energy’s success has been largely due to its effective execution of its business strategy, which has included capital investments in its operational properties, prudent cost management, and commitment to innovation and best practices.

Tamarack Valley Energy’s earnings will be closely monitored to determine if it has continued to deliver on its strategy and produced impressive results. Expectations are high for Wednesday’s earnings announcement, as investors and analysts look for confirmation of the company’s strengths, and any potential weaknesses that may be revealed. Ultimately, Tamarack Valley Energy’s earnings release will be an important indicator of the health of the oil and natural gas industry in Canada.

Stock Price

Tamarack Valley Energy (TVE) is set to release its earnings report for the quarter on Wednesday, and the media exposure so far is mostly positive. On Friday, TVE’s stock opened at CA$4.1 and closed at CA$4.3, representing a 4.3% increase from the previous closing price of CA$4.2. Investors will be looking forward to seeing how these financial results compare with the estimates that have been given. Analysts are expecting this report to provide more clarity into the company’s current business operations and give an idea of how well they are performing.

Additionally, investors will want to see if TVE has been able to effectively manage its expenses and maintain a healthy profit margin. The stock’s performance over the course of the next few days will depend heavily on the accuracy of these estimates. Live Quote…

Analysis

At GoodWhale, we have thoroughly analyzed the fundamentals of TAMARACK VALLEY ENERGY and based on this analysis, we can safely conclude that it is a high risk investment. While conducting our analysis, we have noticed various warning signs, which have been identified across the income sheet, balance sheet, cashflow statement and financial journal. We recommend registering with us to have a closer look at these warnings and understand the risks associated with investing in TAMARACK VALLEY ENERGY. More…

Summary

Tamarack Valley Energy is set to release its earnings on Wednesday and at the time of writing, the media exposure has been mostly positive. Investors should pay attention to these results as the stock price has spiked in anticipation of the announcement. Analysts are expecting to see a positive impact on the company’s stock price due to the potential earnings announcement.

It is also important to note that TAMARACK VALLEY ENERGY has been on an upward trend in the past few months and this announcement could be a catalyst for further growth. Investors should review their portfolio and consider investing in TAMARACK VALLEY ENERGY to capitalize on potential upside.

Trending News ☀️

StoneX Group Inc.’s CEO Sean is set to receive an impressive US$600.0k pay packet at the Annual General Meeting on 1st of March. Such a package is undoubtedly well-earned, as Sean has been leading the company to success for many years. His hard work and dedication have been instrumental in helping StoneX Group Inc. become a leader in their sector, and the desired pay packet reflects this. It also serves to motivate Sean to continue developing the company and achieving more fantastic results in the future.

The Annual General Meeting will be an important one as there is much to discuss. Aside from Sean’s pay packet, the board will be looking at the overall performance of StoneX Group Inc. over the past year and deciding on strategies for moving forward in the future. This is all set to take place on 1st of March, with Sean’s pay package undoubtedly being a key point of discussion.

Market Price

Amidst a flurry of media coverage, StoneX Group Inc. CEO Sean is set to receive a hefty US$600.0k pay packet at the company’s Annual General Meeting on March 1st. The news has so far been embraced in a positive manner, and the company’s stock has seen only a slight decline despite the attention it has garnered. On Thursday, the stock opened at $100.7 and closed at $99.7, representing a 1.0% decrease from its prior closing price of 100.6. Live Quote…

Analysis

GoodWhale recently conducted a review of STONEX GROUP’s wellbeing and according to the Star Chart, STONEX GROUP is strong in growth, medium in asset, profitability and weak in dividend. STONEX GROUP has an intermediate health score of 5/10 with regard to its cashflows and debt and we believe that the company is likely to sustain future operations in times of crisis. Based on these results, STONEX GROUP has been classified as ‘cheetah’, a type of company that achieved high revenue or earnings growth but is considered less stable due to lower profitability. This type of company may be especially attractive to opportunistic investors, those who are willing to take more risks in pursuit of potential gains, as well as those who are looking for companies that may have more potential for growth. The higher risk associated with these types of investments may result in a higher likelihood of a higher return. More…

Summary

STONEX Group Inc. is currently experiencing a surge in investor interest ahead of its Annual General Meeting on March 1st, where its CEO Sean is set to receive a US$600.0k pay packet. Analysts suggest that this amount is deserved given the company’s strong financial performance over the past several years. Its stock has been rising steadily due to solid earnings growth and improving profitability, indicating a strong outlook for shareholders.

The company also has a healthy balance sheet with ample liquidity and low levels of debt, indicating it can handle any financial setbacks that come its way. With the market being bullish on the company, now appears to be the ideal time to invest in STONEX Group Inc.

Trending News ☀️

Neighbourly Pharmacy Inc. is celebrating another successful quarter this year. The pharmacy network has announced its excellent performance in the third quarter of 2023, solidifying its position as Canada’s largest network of independent pharmacies. The company has seen steady growth in its customer base, as well as impressive profit margins. This has been driven by the company’s commitment to offering top-notch customer service, an expansive range of products, and unbeatable prices. This has allowed Neighbourly Pharmacy Inc. to remain competitive and create greater value for its customers.

In addition, the company has invested heavily in research and development for new technologies, such as its AI-enabled back-end systems to better serve customers and increase efficiency. Overall, Neighbourly Pharmacy Inc. is thrilled with the results of its third quarter and is committed to continuing to deliver outstanding service and products for the benefit of its customers. With a strong presence in the Canadian pharmacy market, the company looks forward to what the future holds for this rapidly growing network of independent pharmacies.

Market Price

Neighbourly Pharmacy Inc. has much to celebrate as the company recently reported its successful third quarter 2023 results. At the time of writing, media exposure for the company is mostly positive as stockholders and analysts alike have noted the company’s achievements. On Tuesday, NEIGHBOURLY PHARMACY announced that their stock opened at CA$24.1 and closed at CA$23.9, down by 1.0% from prior closing price of 24.2.

Despite the slight decrease, NEIGHBOURLY PHARMACY’s successful quarter has solidified its position as Canada’s largest network of independent pharmacies. This is an impressive accomplishment that is sure to generate further success in the future. Live Quote…

Analysis

At GoodWhale, our team has taken an in-depth look at the fundamentals of NEIGHBOURLY PHARMACY to get a better understanding of the business risk it carries. Based on our analysis, we have come to the conclusion that NEIGHBOURLY PHARMACY is a high-risk investment in terms of its financial and business aspects. GoodWhale has identified two risk warnings in the company’s income sheet and balance sheet that could negatively impact its investments. If you would like to learn more about these potential risks, you can register with us and get the full details. More…

Summary

Neighbourly Pharmacy Inc. has reported strong third quarter 2023 results, with revenue increases across its operations. The success of the quarter has solidified its position as Canada’s largest network of independent pharmacies. The company is highly regarded for its investments in cutting-edge technology, quality customer service, and operational excellence. Analysts are bullish on the stock with good potential for long term growth and stability.

The positive media coverage is an indication of the company’s success, and investors are confident in investing in its stock. All signs point to growth and more positive results yet to come.

Trending News ☀️

Construction Partners, Inc. is pleased to showcase its leading construction innovations at the Raymond James Institutional Investors Conference on March 15th, 2023. As a leading provider of comprehensive construction solutions in the Southeast, Construction Partners, Inc. is committed to providing quality services and innovate solutions. At the conference, they will be presenting their groundbreaking products and services that are customized to meet their customer’s needs. From residential to large commercial projects, Construction Partners, Inc. offers a range of unique services and solutions that can help streamline project timelines and reduce costs. From turnkey packages to individual components and services, they are offering a variety of options that can be tailored to fit any specific project needs.

At the Raymond James Institutional Investors Conference, Construction Partners, Inc. will be showcasing their advanced technologies and highly collaborative approach. With a strong emphasis on sustainability and efficiency, Construction Partners, Inc. is poised to become a leader in the industry in regards to delivering high-quality projects on time and on budget without sacrificing quality and safety. By attending the conference, Construction Partners, Inc. is looking to demonstrate the expertise that sets them apart from their competition. With an extensive background in construction engineering, project management, and finance, Construction Partners, Inc. is perfectly positioned to deliver innovative solutions that strive to exceed customer expectations.

Stock Price

Construction Partners, Inc. is set to showcase their innovations at the upcoming Raymond James Institutional Investors Conference. The news has been mostly positive for the company, with Construction Partners’ stock opening at $26.6 on Friday and closing at $27.6, marking a 1.8% increase from its previous closing price of 27.1. This overall positive sentiment has been further reflected in the upward trajectory of the stock price in the recent weeks, showcasing the confidence of the market in Construction Partners’ future prospects. The Raymond James conference is expected to further bolster this sentiment, particularly among institutional investors. Live Quote…

Analysis

At GoodWhale, we recently analyzed CONSTRUCTION PARTNERS, a construction and engineering company, to provide our financial insights and analysis. With our proprietary Valuation Line, we calculated the fair value of the CONSTRUCTION PARTNERS share at around $36.1. Currently, CONSTRUCTION PARTNERS stock is trading at $27.6, which means it is undervalued by 23.6%. We recommend that investors consider this opportunity to purchase the stock at a discounted price. GoodWhale’s analysis also suggests that there is significant potential for price appreciation in the coming months. However, these statements are not investment advice and should be crosschecked with your own research before making an investment decision. More…

Summary

Construction Partners, Inc., a provider of infrastructure construction services, will be showcasing its innovations at the upcoming Raymond James Institutional Investors Conference. Investors can look forward to learning more about the company’s capabilities and how they can benefit by investing in Construction Partners. The company has enjoyed positive news coverage so far and is expected to continue to make improvements and build upon the success of its current solutions. With an eye towards the future, the company is ready to show the world what they can do.

Trending News ☀️

Barclays has recently downgraded SM Energy’s rating from Neutral to Underweight and reduced its price target for the stock to $32. Barclays has stated that the decline was due to higher supply-chain costs, weaker natural gas prices, and continued production declines in certain areas. Furthermore, Barclays has expressed concern about the company’s diminishing free cash flow position, which could be further exacerbated by rising expenses. Despite these short-term setbacks, Barclays believes that SM Energy has the potential to experience a bullish trend in the future given its position in the Permian Basin, where production is expected to increase significantly.

Share Price

News coverage of SM Energy has been mostly positive so far, despite a downgrade by Barclays on Wednesday. Barclays downgraded the rating of SM Energy stock to “underweight” and lowered the price target to $32. The downgrade had a visible impact on the stock’s performance, which opened at $29.3 on Wednesday and closed at $29.0, a decrease of 1.8% from the previous day’s closing price of $29.5. Investors responded to the downgrade by taking a cautious approach to SM Energy’s stock, as the news could influence future pricing. Live Quote…

Analysis

GoodWhale performed an analysis of SM ENERGY’s financials, and have determined that the fair value of SM ENERGY’s share is around $30.4. This value was calculated using our proprietary Valuation Line, which combines valuation metrics such as price/earnings and enterprise value/EBITDA to determine the fair price at any given time. At present, SM ENERGY stock is being traded at $29.0, which is a fair price but undervalued by 4.5%. Therefore, investors should consider buying SM ENERGY stock right now as it is currently undervalued. More…

Summary

Investment analysts at Barclays have downgraded their rating on SM Energy to Underweight and lowered the price target to $32. Although the news coverage has been mostly positive so far, investors need to do their own due diligence before investing in SM Energy. Analysts suggest evaluating the company’s current financial health, recent management changes, the current price of oil, and the company’s future growth potential.

Other considerations include comparing the company to its competitors, reading its 10-K filings, and considering the risk associated with investments in the energy sector. Investors should also consider additional factors such as global economic trends and macroeconomic conditions.

Trending News ☀️

United Rentals Inc. is currently offering a tempting yield and the average volume for the company stands at 680.58K. The current stock price for the company is set at $461.25, making it an excellent choice for investors looking to capitalize on high yields. The company’s strong stock performance can be attributed to its wide variety of rental products and services. United Rentals Inc. offers a wide range of products and services, ranging from equipment rentals to general-purpose tools and supplies. The company also specializes in aerial lifts, lighting and power systems, and climate control solutions, allowing customers to utilize the latest technology in their rental needs. This helps attract customers who need to rent equipment for their businesses or personal needs.

In addition to their extensive product range, United Rentals Inc. also provides services such as repair, maintenance, and installation of their products. This ensures that customers receive the highest possible performance from their rented products. With the right level of service, customers can rest assured that their rental needs are taken care of. United Rentals Inc. offers an attractive yield at $461.25 with an average volume of 680.58K, making it an excellent choice for investors looking to capitalize on high yields. With its wide range of rental products and services, coupled with its commitment to providing excellent customer service, United Rentals Inc. is well-positioned to continue its strong stock performance in the future.

Share Price

United Rentals Inc. is set to offer tempting yields at $461.25 with an average volume of 680.58K. So far, media exposure towards the company has been mostly positive. On Tuesday, United Rentals stock opened at $455.0 and closed at $445.6, representing a 3.4% decline in the stock price from the previous closing price of 461.2.

This suggests that investors remained cautious of the stock despite all the positive press. Nevertheless, with an average volume, United Rentals could be set for growth and offer investors attractive yields in the future. Live Quote…

Analysis