Dollar General Stock Fair Value Calculation – Can Dollar General Rebound from Recent Struggles? A Look at What’s Gone Wrong and How to Revitalize the Company

January 4, 2024

🌧️Trending News

Dollar General ($NYSE:DG) has long been a mainstay in the US discount retail market, but in recent years the company has been struggling to remain competitive. The main issues plaguing the company are a lack of innovation, over-reliance on bargain-basement prices, and failure to keep up with the changing retail landscape. All of these issues have created an environment where it is difficult for Dollar General to compete with other discount retailers. One potential solution is to focus on creating an improved shopping experience. This includes modernizing the store layout, adding more appealing displays, and introducing new products and services.

Additionally, Dollar General should consider implementing a loyalty program and providing rewards for frequent shoppers. This could help to drive more traffic to their stores and increase customer loyalty. The company should also look for ways to expand beyond simply selling discount items. They could look to partner with other companies and incorporate their products into their stores, or offer services such as banking or delivery. This could help to diversify their income streams, while increasing their appeal to a wider range of customers. This includes optimizing its website for mobile devices, improving customer service through online chat options, and creating a more comprehensive store locator. Doing so could help Dollar General leverage digital marketing strategies to increase its visibility and gain more customers. By taking action on these fronts, Dollar General can make strides in rebounding from its recent struggles. By implementing these suggestions, the company can look to create an improved shopping experience for customers, expand its customer base, and become more competitive in the discount retail market.

Stock Price

Tuesday marked a small victory for DOLLAR GENERAL, with the stock price opening at $136.8 and closing at $140.4, up by 3.3% from the prior closing price of 136.0.

However, this does not mask the struggles that DOLLAR GENERAL has faced in recent times. DOLLAR GENERAL’s struggles can be attributed to an increase in competition from larger retailers such as Walmart and Target, and the emergence of online shopping. These larger retailers have been able to offer lower prices, making it difficult for DOLLAR GENERAL to remain competitive.

Additionally, DOLLAR GENERAL has experienced a decrease in foot traffic due to the ever-increasing shift to online shopping. The company should focus on increasing their online presence by looking into more avenues for online shopping, such as via their website or through online marketplaces like Amazon or eBay. Additionally, they should look into building strong relationships with other large retailers in order to create a more multi-faceted approach to shopping. This will help bring in new customers and ensure that existing customers stay loyal. Lastly, DOLLAR GENERAL should focus on providing quality service and products to its customers. They should focus on customer experience, as well as ensuring that they have competitive prices and a wide selection of products for customers to choose from. Doing so will help them remain competitive and ensure that customers continue to shop at DOLLAR GENERAL. To rebound from this and revitalize the company, DOLLAR GENERAL should focus on increasing both their online presence, by looking into more avenues such as their own website or online marketplaces, as well as increasing their physical retail presence by building strong relationships with other retailers. Additionally, they should focus on providing quality service and products to customers to ensure that they remain competitive and customers stay loyal. Live Quote…

About the Company

Income Snapshot

Below shows the total revenue, net income and net margin for Dollar General. More…

| Total Revenues | Net Income | Net Margin |

| 39.04k | 1.92k | 4.9% |

Cash Flow Snapshot

Below shows the cash from operations, investing and financing for Dollar General. More…

| Operations | Investing | Financing |

| 2.18k | -1.72k | -460.6 |

Balance Sheet Snapshot

Below shows the total assets, liabilities and book value per share for Dollar General. More…

| Total Assets | Total Liabilities | Book Value Per Share |

| 30.62k | 24.17k | 29.39 |

Key Ratios Snapshot

Some of the financial key ratios for Dollar General are shown below. More…

| 3Y Rev Growth | 3Y Operating Profit Growth | Operating Margin |

| 6.3% | -6.3% | 7.2% |

| FCF Margin | ROE | ROA |

| 1.2% | 27.5% | 5.7% |

Analysis – Dollar General Stock Fair Value Calculation

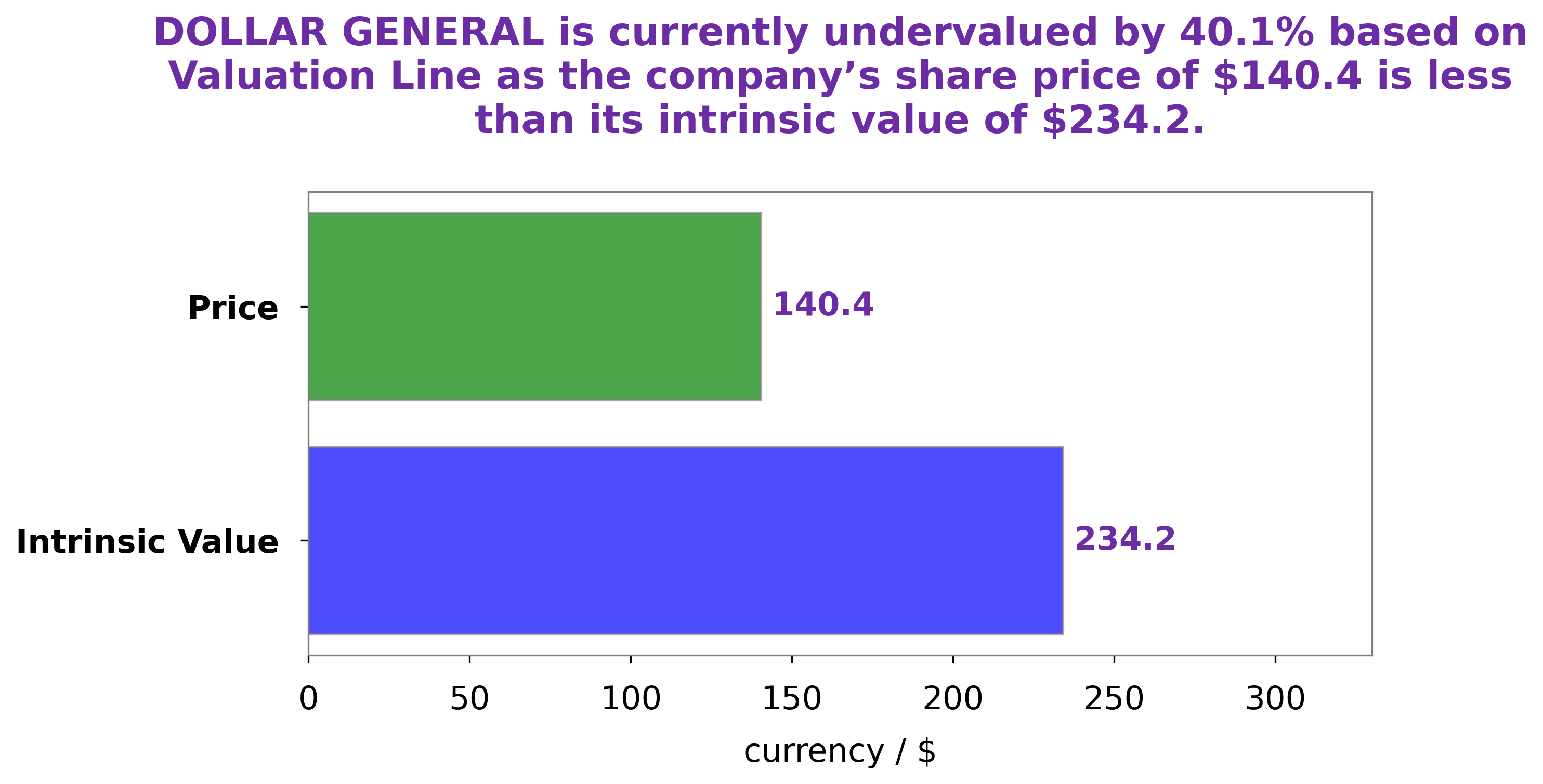

At GoodWhale, we analyzed the fundamentals of DOLLAR GENERAL stock and calculated its intrinsic value with our proprietary Valuation Line. We concluded that the intrinsic value of DOLLAR GENERAL share is around $234.2. This means that the current market price of DOLLAR GENERAL share ($140.4) is undervalued by 40.1%. We think that the current market price presents an opportunity for investors to buy the stock at a discount. More…

Peers

Dollar General Corp and its competitors, Dollar Tree Inc, Walmart Inc, Target Corp, are all vying for a share of the retail market. Dollar General has been able to stay ahead of the competition by offering a variety of products at a lower price point.

However, the other companies are not far behind and are constantly innovating to try and win over customers. It is an ongoing battle to see who can provide the best value to shoppers.

– Dollar Tree Inc ($NASDAQ:DLTR)

Dollar Tree is a company that operates at a low margin, high volume business model. The company offers a wide variety of merchandise at a low price point of $1.00. The company has a market cap of $35.49B as of 2022 and a ROE of 15.97%. The company has been able to grow its earnings at a double-digit rate over the past few years.

– Walmart Inc ($NYSE:WMT)

Walmart Inc is an American multinational retail corporation that operates a chain of hypermarkets, discount department stores, and grocery stores. Headquartered in Bentonville, Arkansas, the company was founded by Sam Walton in 1962 and incorporated on October 31, 1969. As of January 31, 2020, Walmart has 11,484 stores and clubs in 27 countries, operating under 55 different names. The company operates under the name Walmart in the United States and Canada, as Walmart de México y Centroamérica in Mexico and Central America, as Asda in the United Kingdom, as the Seiyu Group in Japan, and as Best Price in India. It has wholly owned operations in Argentina, Chile, Canada, and South Africa. Since August 2018, Walmart only holds a minority stake in Walmart Brasil, with 20% of the company’s shares, and private equity firm Advent International holding 80% ownership of the company.

– Target Corp ($NYSE:TGT)

Target Corp is a large retail company with a market cap of 75.6B as of 2022. The company has a return on equity of 34.09%. Target Corp is a retailer that sells a variety of products including clothing, electronics, and home goods. The company has over 1,800 stores in the United States and also has an online store. Target is a publicly traded company and its ticker symbol is TGT.

Summary

Dollar General‘s stock price has taken a hit over the past year, and many investors are wondering if there is any potential for a revitalization. Analysts have pointed to various factors contributing to the downturn, including slowing sales growth, increased competition from online and discount retailers, and rising costs of goods. To assess the potential of a turnaround, investors need to analyze Dollar General’s financials, as well as monitor economic conditions and competitive trends.

Additionally, investors should track the company’s initiatives to improve its operational efficiencies and expand its presence in new and existing markets. With careful analysis and insight, investors may be able to determine if Dollar General is worth investing in.

Related Posts

Recent Posts

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Investing Everyone Can Do.

Investing shouldn’t be exclusive to a select few. We believe everyone should have the opportunity to grow their wealth. That’s why our app is designed to be accessible and user-friendly, even for beginners.