Dollar General Corp. Shares Drop After Q4 Sales Miss Expectations Despite Market Share Gains

February 25, 2023

Trending News 🌧️

DOLLAR ($NYSE:DG): The U.S. Justice Department is reportedly taking steps to block Adobe’s planned acquisition of Figma, a cloud-based web platform developer, for $20 billion. This move comes as part of an antitrust investigation looking into the potential effects the merger would have on competition in the software industry. The proposed acquisition, which would be one of the largest ever within the software space, has raised concerns about the potential for the newly merged company to create a monopoly in certain areas. The Justice Department is expected to file a lawsuit arguing that the merger could harm market competition and lead to higher prices for consumers. If the lawsuit is successful in blocking the acquisition, it could cause long-term damage to Adobe’s plans for expansion and growth.

At the same time, Adobe might be able to find other targets for acquisition if the deal with Figma is blocked. The ruling on the Adobe-Figma acquisition will be watched closely by other major companies in the software space. It could have wide-ranging implications for other potential mergers and acquisitions, and will likely set a precedent for future antitrust lawsuits. In any case, the Justice Department’s decision could have a significant impact on the future of Adobe, Figma, and the industry as a whole.

Stock Price

On Thursday, the US Justice Department announced that it would be prohibiting Adobe’s planned $20B acquisition of Figma, a startup software company. The news sent immediate reverberations throughout the stock market, with Adobe Inc’s stock opening at $350.4 and closing at $347.0, down by 0.5% from its prior closing price of 348.7. This is a major setback for the company, which had planned to use the acquisition as a way to capitalize on Figma’s successful web based design platform and expand their own software suite. With the Justice Department blocking this merger, Adobe will have to look for another way to stay competitive in the software market and add new features in the near future. Live Quote…

About the Company

Income Snapshot

Below shows the total revenue, net income and net margin for Dollar General. More…

| Total Revenues | Net Income | Net Margin |

| 36.29k | 2.35k | 6.5% |

Cash Flow Snapshot

Below shows the cash from operations, investing and financing for Dollar General. More…

| Operations | Investing | Financing |

| 1.89k | -1.37k | -647.27 |

Balance Sheet Snapshot

Below shows the total assets, liabilities and book value per share for Dollar General. More…

| Total Assets | Total Liabilities | Book Value Per Share |

| 29.01k | 22.91k | 27.26 |

Key Ratios Snapshot

Some of the financial key ratios for Dollar General are shown below. More…

| 3Y Rev Growth | 3Y Operating Profit Growth | Operating Margin |

| 10.0% | 12.9% | 8.8% |

| FCF Margin | ROE | ROA |

| 1.4% | 32.5% | 6.9% |

Analysis

At GoodWhale, we recently conducted an analysis of ADOBE INC’s financials. Our proprietary Valuation Line model suggested that the fair value of ADOBE INC share should be around $563.3. However, the current market price is only $347.0, which means the stock is trading at a discount of 38.4% from its fair value. This presents an excellent opportunity for investors looking to capitalize on potential upside potential in ADOBE INC stock. We believe that this discrepancy between the fair value and the current market price could be indicative of an attractive entry point for investors to get into the stock. More…

Summary

Adobe Inc. (ADBE) is an American multinational computer software company that has recently been in the news for its planned $20 billion acquisition of Figma. Despite the high price tag, analysts believe that the acquisition would be beneficial to Adobe’s operations in the long-term. Adobe’s subscription-based cloud services are projected to increase in value, and the company is expected to benefit from the added features, cost savings, and increased customer base that the Figma acquisition could provide. Other reports point to Adobe’s potential market share increase and further adoption of its software solutions as potential benefits to its investments.

Analysts are optimistic about Adobe’s competitive positioning post-Figma acquisition and anticipate increases in profit margins and returns on equity. In general, investors continue to view Adobe as a strong and reliable long-term investment opportunity.

Trending News 🌧️

This analysis seeks to compare the GPU performance of AMD against its competitors Intel and Nvidia in different generations of desktop and notebook computers. To do this, we will use GPU benchmark scores as a measure. By looking at the benchmark scores from different generations of AMD’s GPUs, we will be able to determine if AMD has an edge over its rivals. We can expect to see improved performance as we look at newer GPU generations from all three companies, however, the goal of this analysis is to uncover whether one manufacturer outperforms the other in terms of performance and how the performance changes over time. In particular, we will focus on how AMD’s GPUs perform when compared to Intel and Nvidia in different generations of desktop and notebook computers.

We will also be looking at how AMD’s GPUs compare to the offerings from Intel and Nvidia in terms of features such as memory size, number of cores, and clock speeds. The results of this analysis should provide us with valuable insight into the competitive landscape surrounding GPUs and GPU products. By doing a comprehensive comparison of AMD to Intel and Nvidia, we should be able to determine if there is an advantage that AMD has in any particular market or if it is comparable to its competitors in all areas. Ultimately, this analysis should provide a clear picture of the GPU performance levels that each company is capable of providing across multiple generations of products.

Share Price

Recent media coverage of ADVANCED MICRO DEVICES (AMD) reveals positive sentiment around their competitive advantage when it comes to graphics processing unit (GPU) performance compared to Intel and Nvidia. On Thursday, AMD stock opened at $80.6 and closed at $79.8, up by 4.1% from the last closing price of 76.6. This increase can be attributed to the positive news regarding AMD’s performance in both desktop and notebook generations. The company has made significant strides in the GPU market, and analysts agree that AMD is outperforming Intel and Nvidia in terms of graphics performance. This performance has given AMD an edge over its competitors, which has translated into greater investor confidence.

AMD has also recently released its new Ryxen series of GPUs that are expected to provide further gains in performance. In conclusion, recent analyses of AMD’s GPU competition with Intel and Nvidia have been overwhelmingly positive and have clearly been reflected in the stock’s performance. This indicates that investors are largely confident in AMD’s ability to provide superior graphics performance in both desktop and notebook generations, and this trend is expected to continue as the company releases new products. Live Quote…

Analysis

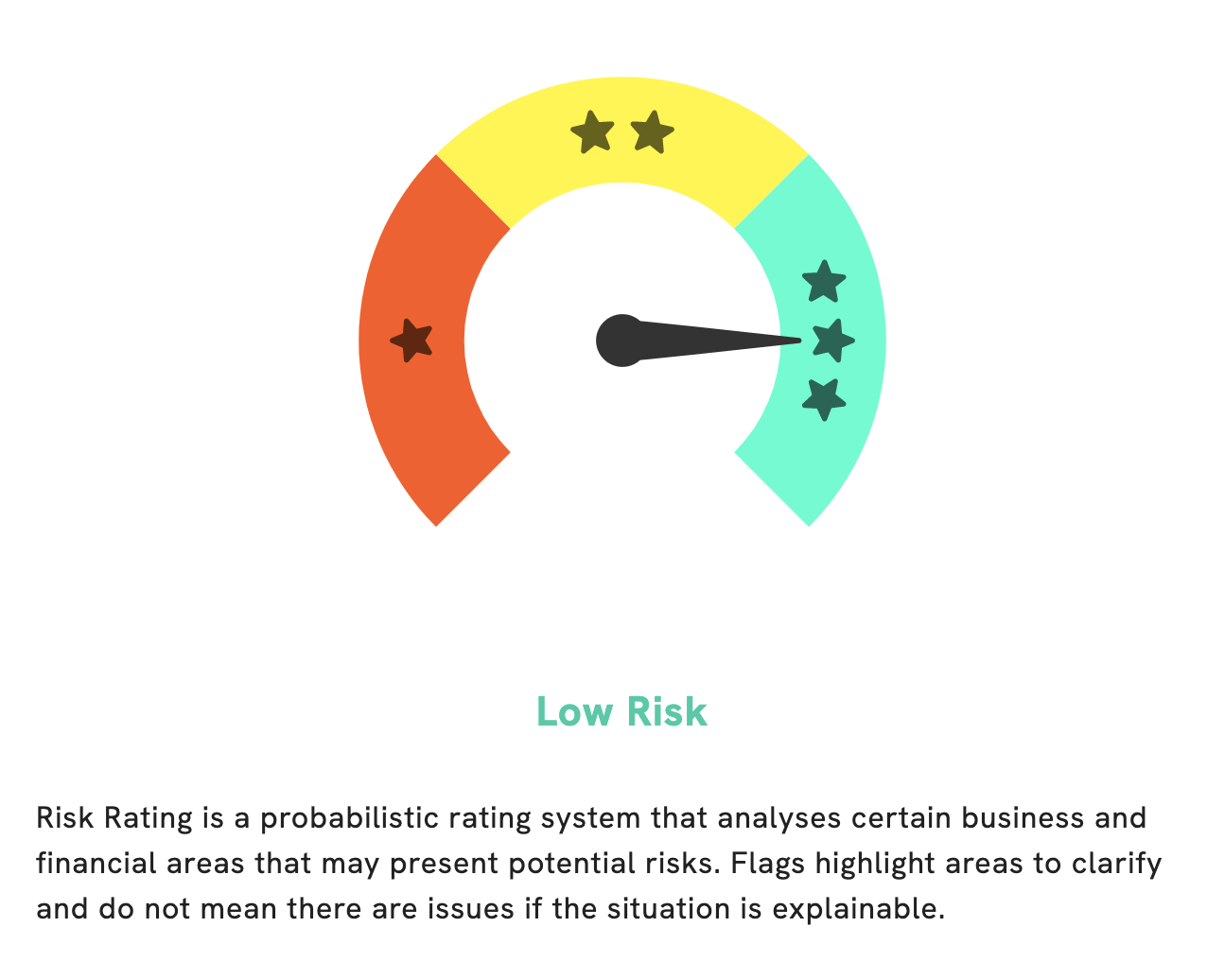

GoodWhale makes it easy to analyze ADVANCED MICRO DEVICES’s fundamentals. Our Risk Rating gives you an overview of their financial and business risk, and we give it the highest rating of “High”. Furthermore, we have detected 2 risk warnings in ADVANCED MICRO DEVICES’s income sheet and balance sheet. To get all the details on these points, register on GoodWhale.com and take a look for yourself. It’s free and easy to use. More…

Summary

Advanced Micro Devices (AMD) has recently gained media attention for its competitive advantage in GPU performance across desktop and notebook generations compared to Intel and Nvidia. This has been accompanied by a rise in AMD’s stock price on the same day, indicating that the market has responded positively to the news. AMD is becoming an increasingly attractive investment opportunity as it continues to innovate and provide consumers with better options for enhancing graphic performance. With a focus on developing powerful technology, AMD is sure to remain a leading force in this space.

Trending News 🌧️

Netflix is embracing a new strategy to grow its subscriber base by reducing prices in certain markets. In some countries, the cost of a Netflix subscription has been cut by as much as 50%, giving these markets access to a wealth of entertainment at a fraction of the usual price. This follows an industry-wide trend of streaming services, including Peacock, raising prices in order to make direct-to-consumer offerings more viable. According to the Wall Street Journal, countries in the Middle East, sub-Saharan Africa (Kenya, for example), Europe (Croatia and Slovenia), Latin America (Nicaragua, Ecuador, Venezuela), and parts of Asia (Malaysia, Indonesia, Thailand, Philippines) are amongst those affected by this price reduction.

Netflix’s move to slash prices comes at a time when more and more streaming services are vying for consumer attention. As the streaming landscape becomes increasingly competitive, offering cheaper than average subscription rates could prove a powerful tool to attract new subscribers and retain existing ones. It remains to be seen how this latest effort will fare in helping Netflix maintain its position as one of the leading streaming platforms worldwide.

Stock Price

Netflix has recently made news by slashing their prices in different countries, presumably in an effort to boost subscriber growth in the face of increasing streaming competition. This news has been mostly met with neutral response, although the company’s stock did take a hit on Thursday. At the opening of the trading session, Netflix shares were priced at $331.2, before closing later that day at $323.6, which was 3.4% lower than the previous closing price of $334.9. Despite this, analyst still remain optimistic that this price cut could lead to long-term growth for the streaming giant. Live Quote…

Analysis

At GoodWhale, we have analyzed NETFLIX’s fundamentals and found them to be of intermediate health, scoring 5/10. This suggests that the company should be able to ride out any crisis without the risk of bankruptcy. We have classified NETFLIX as a ‘rhino’, which is a company that has achieved moderate revenue or earnings growth. Such companies are typically of interest to growth investors, as well as those who value high profitability. When it comes to NETFLIX’s fundamentals, they are strong in growth and profitability, but weak in asset and dividend. Investing in NETFLIX may thus be suitable for those who are looking for high growth potential but are willing to forego dividends. More…

Summary

Netflix is a streaming service provider that has recently slashed prices in markets around the world in an effort to boost its subscriber growth. The decision comes amid increasing competition in the streaming industry, particularly from tech giants such as Disney and Apple. In response to the news coverage, which has been mostly neutral, the stock price of Netflix has fallen on the same day.

For investors considering investing in the company, it is important to take into account its current positioning in the streaming market and the potential for future growth. Moreover, Netflix’s recent price cuts should be considered when evaluating its potential future prospects.

Trending News 🌧️

Block disappointed investors in their fourth quarter of 2023 with a non-GAAP earnings per share (EPS) of $0.22 that fell short of expectations by $0.08. This miss of expectations caused a significant dip in the stocks of Block directly following the announcement. Analysts are still trying to figure out the exact cause of this failure, with some pointing to a higher cost structure in the quarter. Many investors had already expected that the earnings would not reach their goal due to the economic downturn and increasing competition. Regardless of the cause, it is clear that Block has failed to meet its forecast for this quarter and has consequences for investors.

It is yet to be seen what the long-term result of this earnings miss will be, as stock prices have already dropped due to investor confidence being shaken. Analysts are expecting more positive news in the upcoming quarters as Block works on reducing costs and improving their operations. Until then, investors will have to wait and see if Block can bounce back and deliver the results they had initially anticipated.

Price History

On Thursday, BLOCK opened at $74.3 and closed at $74.2, up by 1.7% from its previous closing price at 72.9. This suggests that investors are still relatively optimistic about the company’s prospects moving forward despite the earnings results. Live Quote…

Analysis

GoodWhale has conducted an analysis of BLOCK’s financials and the results show that it has been classified as a ‘gorilla’ in our Star Chart. This means the company has achieved strong and stable revenue or earning growth due to its competitive advantage. Investors interested in such companies may be looking for growth, profitability and medium asset investments, while they may not be as interested in dividend investments. BLOCK also scored highly in terms of cashflows and debt with a health score of 8/10. This indicates that the company is capable of sustaining future operations even in times of crisis, which makes it an attractive option for investors. More…

Summary

Investing analysis on Block provides a mixed outlook. As of Q4 2023, the company reported a Non-GAAP EPS of $0.22, which missed expectations by $0.08. Overall, the market response has been negative.

Therefore, investors should exercise caution when deciding whether or not to bring Block into their portfolios. It may be wise to wait and see how future performance of the company unfolds in the upcoming quarters before investing.

Trending News 🌧️

Despite Grab’s ongoing losses in pursuit of market share, the company has made notable efforts to increase its profitability. As a result, Grab’s profit margins have seen improvements in recent periods. These efforts have included multiple measures, such as cutting costs, integrating services and assessing customer needs more effectively. The past few years have seen Grab apply a notably different strategy compared to the past, focusing more on profitability rather than market share. This has seen the company refocus its business on core products and services, while at the same time consolidating its market presence in the South East Asian region.

As a result, Grab has been able to maintain a strong financial position despite its losses, allowing it to continue to focus on expanding its services. Overall, Grab Holdings has been able to improve its profit margins despite ongoing losses in pursuit of market share. By refocusing its strategy and cutting costs, the company has been able to improve its financial performance and remain competitive on the market. Although Grab still endures net losses overall, the company remains well-positioned for continued success in the future.

Stock Price

Despite ongoing losses as Grab Holdings pursues market share, the company was able to improve their profit margin and has seen mostly positive media exposure. On Thursday, the opening price of GRAB HOLDINGS was $3.6, however by the closing at 4PM, the stock had dropped 8.3% from the prior closing price of 3.5, closing at $3.2. Live Quote…

Analysis

GoodWhale has conducted a wellbeing analysis of GRAB HOLDINGS, and the results indicate that the company is strong in asset and growth, but weak in dividend and profitability. On the Star Chart, GRAB HOLDINGS has an intermediate health score of 6/10 with regard to its cashflows and debt, indicating that it is likely to safely ride out any crisis without the risk of bankruptcy. Therefore, GRAB HOLDINGS has been classified as a ‘cheetah’ company. This means that it has achieved high revenue or earnings growth, but is considered less stable due to lower profitability. Investors who value potential for high growth more than stability may be interested in GRAB HOLDINGS. For example, venture capitalists or mutual fund companies with a risk-taking attitude might be drawn to investing in GRAB HOLDINGS due to its high potential for growth. Other investors who prefer more stable investments may wish to steer clear of GRAB HOLDINGS due to the higher risk associated with its financial position. More…

Summary

Grab Holdings, the Southeast Asian ride-hailing and food delivery company, recently reported a significant improvement in their profit margins even though they still made a net loss. While their media exposure has been mostly positive, the stock price dropped on the same day. Consequently, investors should conduct further research to get a better understanding of the company’s financials and prospects. They should look at Grab’s financial performance over the last several quarters, analyze their market share in comparison with competitors, and assess their overall competitive advantage.

Additionally, investors should look at recent events and news that may have a bearing on the stock price. Finally, they should consider the expected returns from investing in Grab Holdings and the potential risk factors.

Trending News 🌧️

Despite some recent turmoil that has surrounded Salesforce, Goldman Sachs analyst Kash Rangan believes that investors should not be discouraged from buying the company’s shares. In a research report released on Thursday, Rangan raised his price target to $310 per share, citing the potential for Salesforce to join the ranks of premier, highly valued technology companies. Although the company is currently dealing with activist investors and its plans to lay off 10% of its employees, Rangan remains optimistic and believes these issues should not be enough to dissuade potential investors. Despite these short-term events, Rangan is confident that Salesforce has a bright future. He cites the company’s continued commitment to Artificial Intelligence and cloud computing as evidence that Salesforce can still provide “competitive gains in the long run.”

He also believes that Salesforce’s customer base will remain largely loyal, allowing the company to continue to realize strong growth in the years ahead. In conclusion, although some may be deterred by the current turmoil surrounding Salesforce, Goldman Sachs analyst Kash Rangan advise investors to remain confident in the company’s long-term prospects. He believes that there is still plenty of money to be made in Salesforce stock and that people should not be discouraged from buying shares in the company.

Share Price

Despite media sentiment largely being negative, Goldman Sachs analysts assert that investors should not flee from Salesforce.com stock. On Thursday, the company’s stock opened at $165.3 and closed at $164.1, up by 0.5% from its last closing price of 163.4. This was a positive sign considering the turbulent period the company is currently undergoing in terms of earnings and market conditions. Based on the analyst’s positive opinion, investors should not be deterred from investing in Salesforce in spite of the current challenges the company is facing. Live Quote…

Analysis

At GoodWhale, we recently conducted an analysis of SALESFORCE.COM’s well-being. Our Risk Rating has classified SALESFORCE.COM as a high risk investment in terms of financial and business aspects. When reviewing their income sheet, balance sheet, cashflow statement, and other non financial information, we found four risk warnings. To learn more about these risks, please visit our website goodwhale.com. Here you can review our financial reports, analysis and warnings about SALESFORCE.COM. We hope this helps you to make an informed decision when investing in SALESFORCE.COM. More…

Summary

Despite the current turmoil in Salesforce, a recent Goldman Sachs analysis suggests that investors should not panic and should remain confident in the company. According to the analyst, Salesforce still has significant growth potential with its cloud-based services and products. Despite the negative media sentiment surrounding the company, the firm’s strategy of focusing on customers, products, and employees is likely to capture more long-term value.

Furthermore, the analyst highlighted that Salesforce has a consistent track record of strong revenue growth, declining operating margins, and solid cash generation. Ultimately, the analyst believes that Salesforce is well-positioned for success in the long run in the cloud-based industry.

Trending News 🌧️

On Thursday, Guggenheim downgraded Veeva Systems shares due to concerns that the estimates for fiscal 2024 are too high. The downgrade caused the stock to fall more than 1% in premarket trading. The decision to downgrade the stock was made due to the fact that Guggenheim analysts determined that the estimates for fiscal 2024 may be overly optimistic. They determined that Veeva System’s shares could be overvalued and that any potential upside is likely to be limited in the near term. The downgrade comes as Veeva Systems has seen tremendous growth in recent years and is one of the leading players in the cloud computing and enterprise software markets. The company has gained significant market share and has emerged as a cloud computing powerhouse.

Despite this, Guggenheim’s analysts feel there is a risk of overvaluation. They are concerned that the current estimates for fiscal 2024 may be too high and could leave investors in a difficult position. As a result, investors may want to reevaluate their positions with Veeva Systems. While this downgrade can be seen as a negative, it is also an opportunity for investors to reassess and make sure they are comfortable with their investments. Furthermore, the downgrade is a reminder that it is important to do your own research and analysis when investing in any company.

Price History

On Thursday, Guggenheim downgraded Veeva Systems’ stock rating to ‘Sell’ from ‘Neutral’, citing concerns that fiscal 2024 estimates were too high. The media exposure surrounding the downgrade has been predominantly negative and this has had a negative impact on Veeva Systems’ stock price. The stock opened at $171.0 and closed at $170.5, down 0.3% from the previous closing price. This marks a continuation of downward trends that Veeva Systems have seen in recent days following the downgrade and heightened media focus. Live Quote…

Analysis

At GoodWhale, we have conducted an extensive analysis of VEEVA SYSTEMS’s financials. After careful consideration, our proprietary Valuation Line has calculated that the intrinsic value of VEEVA SYSTEMS stock is around $292.8. As of now, VEEVA SYSTEMS shares are being traded at $170.5, representing a 41.8% discount from the valuation line. This suggests that from an investment standpoint, VEEVA SYSTEMS’s current price represents an attractive opportunity for potential investors. More…

Summary

Veeva Systems has recently experienced a downgrade of its shares by Guggenheim due to their concern that the company’s fiscal 2024 estimates may be too high. This has resulted in mostly negative media coverage of the stock. Investors should conduct thorough research into Veeva Systems before making any investing decisions. Analysts recommend taking a closer look at the company’s financials and potential market opportunities, as well as any potential risks that may be associated with the stock, before investing.

Additionally, investors should also look into the company’s management team and overall strategy for growth. Overall, due diligence and careful analysis is necessary for any investor considering Veeva Systems stock.

Trending News 🌧️

Revolve Group, a leading global fashion and lifestyle brand, recently reported its Q4 2023 GAAP earnings per share of $0.11, which exceeded analyst expectations by $0.01. This marks the eighth consecutive quarter on record that Revolve Group has beaten its quarterly earnings expectations, demonstrating the company’s commitment to consistently deliver profitable results. Revolve Group’s success can also be attributed to its market-leading position in the growing digital-first fashion and lifestyle space. With its strong focus on innovative technologies, sophisticated segmentation, and strategic partnerships with key influencers, Revolve Group has been able to effectively reach and engage new customers around the world.

Overall, Revolve Group’s Q4 2023 GAAP EPS beat expectations by $0.01 and proves the company’s capability to remain competitive in the ever-changing fashion and lifestyle space. With its impressive growth in the fourth quarter of 2023 and its ongoing commitment to delivering profitable results, Revolve Group is well-positioned to continue its success story in the years ahead.

Share Price

On Thursday, REVOLVE GROUP announced an impressive Q4 2023 GAAP EPS of $0.01 more than the expected amount. This announcement caused the company’s stock price to open at $25.5 and close at $24.7, a drop of 2.9% from its prior closing price. The performance suggests that investors remain confident in the company’s ability to deliver healthy profits and continue its upward trend in the next quarter. The news was met with success from analysts, citing the company’s resurgent efficiency and improving confidence from its shareholders. Live Quote…

Analysis

As GoodWhale, I have been analyzing the financials of REVOLVE GROUP and reviewing its performance. Through our Star Chart, we have classified REVOLVE GROUP as a ‘gorilla’ – a type of company with stable, high revenue or earning growth due to a strong competitive advantage. Investors who are interested in REVOLVE GROUP will appreciate its high health score of 10/10 with regard to its cashflows and debt, showing its ability to pay off debt and fund future operations. Additionally, REVOLVE GROUP is strong in some areas such as asset, growth, and profitability, while weak in areas such as dividend. This makes it an attractive option for investors who are looking for potential long-term growth opportunities. More…

Summary

Revolve Group’s stock price saw an increase of 4.1% following the Q4 2023 earnings release, and investors appear to be encouraged by the better-than-expected results. The strong financials and robust growth demonstrate that Revolve Group has the potential to offer strong returns for long-term investors.

Trending News 🌧️

This outperformance was mainly due to the weak macroeconomic environment in China, which led to weaker performance for NetEase’s core gaming business. NetEase also experienced margin compression and an increase in SG&A expenses, which further impacted its Q4 2023 EPS. These additional costs had a negative effect on the company’s earnings for the quarter and led to an underperformance when compared to the market’s expectations. The company expressed positive expectations for the future, citing increased investments in its cloud computing and advertising business as well as in pioneering new growth opportunities.

Although NetEase missed its Q4 2023 non-GAAP EPS estimates by $0.08, it was still able to post solid results with year-over-year growth in revenue and operating income. NetEase’s focus on expanding into emerging businesses will likely help the company build on this momentum going forward and enable it to drive further growth.

Stock Price

On Thursday, NETEASE revealed its Q4 2023 non-GAAP earnings per share (EPS) fell short of the estimates by $0.08. This news was met with mostly negative reviews within the news media, sending its stock downward. NETEASE opened at $88.0 and closed at $82.9, which is 3.7% below its prior closing price of $86.0. The news of the weaker-than-expected earnings result led to a decline in investor confidence, resulting in the sell-off. Live Quote…

Analysis

At GoodWhale, we performed detailed analysis on NETEASE’s wellbeing. Our proprietary Valuation Line calculation revealed an intrinsic value of NETEASE share to be around $102.3. With the current share price traded at $82.9, we believe that NETEASE stock is undervalued by 19.0%. In light of this, we advise our clients to closely monitor the stock as its current price could provide a good entry point for long-term investors. More…

Summary

NETEASE, a well-established Chinese internet technology company, recently announced their fourth quarter of 2023 non-GAAP earnings per share (EPS) results, which missed expectations by $0.08. This news was met with mostly negative coverage amongst the media, and the stock price dropped significantly on the same day. For investors, this is an important takeaway to consider when evaluating NETEASE as a potential investment opportunity. While the current outlook may not be as favorable, successful evaluation of the company’s business activity and financial performance will be key to obtaining favorable returns in the future.

Trending News 🌧️

Autodesk revealed impressive earnings for the fourth quarter of 2023, beating expectations. This beat marked the first time in a few quarters that Autodesk had delivered above the expected Non-GAAP EPS. The company performed exceptionally well in the quarter, especially when compared to previous quarters and the expected results for Q4. This beat is likely due to several recent initiatives and strategies designed to increase revenues. Autodesk recently debuted their new subscription model which has seen a great uptake by new customers.

Additionally, the company recently announced partnerships with various other organizations, which have enabled them to reach more customers and increase revenues. The beat in the fourth quarter is a positive sign that Autodesk’s strategies are paying off and the company is realizing gains from its initiatives. The beat can also be attributed to an increased focus on cost-efficiency. Autodesk has trimmed costs in some areas while still expanding its use of technology, allowing the company to deliver impressive results despite the continuing pandemic. Overall, Autodesk’s showing in the fourth quarter of 2023 is quite promising and shows potential for continued, long-term growth. The company’s strategies appear to be proving successful and if they continue to implement them effectively, Autodesk could continue to exceed expectations for future quarters.

Share Price

Autodesk had strong media exposure for their Q4 2023 financial results, with most reports being positive. On Thursday, AUTODESK stock opened at $218.1 and closed at $221.2, up by 2.1% from its previous closing price of $216.7. This was due to the company’s non-GAAP EPS expectations surpassing projections by $0.05, which was an impressive performance. The result indicated that the company is continuing to make progress and strengthening their financial position. Live Quote…

Analysis

We at GoodWhale have conducted an analysis of AUTODESK’s financials to determine the intrinsic value of the company’s stock. According to our proprietary Valuation Line, the intrinsic value of AUTODESK share is around $288.5. Interestingly, the current market price for AUTODESK stock is $221.2, which suggests that it is undervalued by 23.3%. This discrepancy between the intrinsic and current stock value provides a good opportunity for investors looking to invest in undervalued stocks. More…

Summary

Autodesk, Inc. has recently reported strong financial results in its fourth quarter of 2023, exceeding non-GAAP earnings per share expectations by $0.05. Analysts and investors are generally bullish on Autodesk, with media coverage largely focusing on the company’s positive financial results and growth prospects. Going forward, investors should keep a close eye on Autodesk’s strong innovation pipeline, as well as its recent investments into digital transformation, cloud computing, and data security. With the expected surge in software demand from businesses and consumers, Autodesk is poised to benefit from an increased market share in the coming quarters.

Trending News 🌧️

MercadoLibre, the leading e-commerce and technology platform in Latin America, announced strong fourth quarter financial results this week. The company reported a Q4 GAAP Earnings per Share of $3.25, beating market expectations by $0.93. Revenue of $3 billion exceeded market expectations by $40 million. These impressive results were mainly driven by a year-over-year increase of 80.0% in Total Payment Volume (on an FX neutral basis) and a 34.7% increase in Gross Merchandise Volume (on an FX neutral basis).

This remarkable growth in key metrics demonstrate the success of the company’s digital innovation, as well as its strategic decision to focus on e-commerce and digital payments. In addition to the strong Q4 performance, MercadoLibre also reported numerous other achievements in 2020, including the launch of its mobile marketplace and the expansion of its financial services offering. Despite the global pandemic, the company continues to experience strong momentum in its business, making for a successful end to a challenging year.

Price History

On Thursday, MERCADOLIBRE posted their fourth quarter financial results, and surpassed expectations with a total payment volume increase of 80%.

Additionally, gross merchandise volume increased by 34.7%, resulting in a 1.6% increase in share prices. The total payment volume grew by 80% compared to the same quarter last year, thanks to a strong increase in online sales from the Latin America region, as well as its increasing presence in international markets. In terms of GMV, its 34.7% increase was driven by robust growth across all its markets, specifically in Argentina and Mexico. Overall, these results show MERCADOLIBRE’s ability to capitalize on the increased demand for their products and services during the pandemic. This is reflected in their stock, which opened at $1134.9 on Thursday and closed at $1136.3, up 1.6% from its last closing price of $1118.3. Live Quote…

Analysis

GoodWhale has conducted an analysis of MERCADOLIBRE’s wellbeing and have arrived at a fair value of approximately $2076.6 for MERCADOLIBRE’s share, according to our proprietary Valuation Line. This value is dynamically calculated, taking into account potential market volatility and current corporate developments. However, the current market price of MERCADOLIBRE’s share is at $1136.3, which is significantly lower than the calculated fair value. This implies that MERCADOLIBRE’s share is currently undervalued by 45.3%. In order to make sure that investors are making informed decisions with regards to their investments in MERCADOLIBRE, GoodWhale strives to provide the latest and most accurate information about the current market price alongside our proprietary value estimates. More…

Summary

MERCADOLIBRE recently released their Q4 financial results and the numbers are impressive. Total payment volume increased by a whopping 80%, while Gross Merchandise Volume (GMV) increased by 34.7%. This marks an incredible quarter for MERCADOLIBRE, with both of these metrics smashing expectations and outperforming previous quarters. Investors should take note of the positive growth and stability of the company, as MERCADOLIBRE is well-positioned for continued success in the future.

Trending News 🌧️

American Express is a multinational financial services corporation providing credit cards and other payment service products. In 2023, the company achieved a remarkable milestone in their long history. They reported total revenues of $55.62bn for the trailing twelve months, with an EBITDA of $14.63bn. This is a new record for the company, demonstrating their resilience and ability to continue to grow despite challenging economic conditions. The success of American Express is due, in part, to their expansive product offerings, generous rewards and loyalty programs, and innovative customer service measures, such as mobile and online banking options.

In addition, they have built strong relationships with retailers, enabling them to offer exclusive deals and discounts that help drive customer loyalty. The company’s success in 2023 will only further cement their reputation as a trusted and reliable provider of financial services products. As more customers seek out American Express to meet their financial needs, the company is well-positioned for continued success in the years ahead.

Share Price

American Express (AMEX) has exceeded expectations in 2023, as they have achieved record total TTM revenues of $55.62 billion and EBITDA of $14.63 billion. The news coverage of this monumental achievement has been overwhelmingly positive, with many praising the company’s success. On Thursday the stock of the company opened at $175.2 and closed at $175.1, showing a modest increase of 0.3% from the last closing price of $174.7. This slight increase is likely due to the large volumes of positive news coverage, as investors are keen to get in on what is sure to be a fantastic stock-pick in the coming years. Live Quote…

Analysis

At GoodWhale, we performed an analysis on the financials of AMERICAN EXPRESS. Using our proprietary Valuation Line, we determined that the intrinsic value of the company’s share is around $183.3. Currently, AMERICAN EXPRESS is trading at $175.1, which is a fair price but still undervalued by 4.5%. In other words, there is still upside potential for investors in this stock. More…

Summary

American Express reported record-breaking TTM revenues of $55.62 billion and EBITDA of $14.63 billion in 2023. This impressive financial performance has been well-received by market analysts and investors, as reflected in the company’s current market cap and share price. American Express is heavily reliant on the US consumer spending and is likely to benefit from the continued economic recovery.

Furthermore, the company’s wide array of new products and services, strong brand recognition, and well-established relationships with merchants and consumers should help the company to maintain its competitive advantage. Investors should monitor developments in American Express’ core businesses and any potential expansion plans in order to assess long-term prospects.

Trending News 🌧️

Synopsys, a leading provider of software, IP and services for chip design, verification and manufacturing, has just announced a $300M share repurchase agreement with Bank of America N.A. The rapid repurchase program allows Synopsys to buy back its own shares, making the company more resilient in the long run. This agreement is part of Synopsys’ strategy to reduce the float of its common stock, increasing the value of existing shares and returns for shareholders. With this transaction, Synopsys will purchase up to $300M of its outstanding common stock in the open market or in privately negotiated transactions. Synopsys plans to fund the share repurchase agreement from cash and cash equivalents on hand.

This repurchase plan does not obligate Synopsys to acquire any particular amount of common stock, and the company may discontinue or suspend the repurchase program at any time. The share repurchase agreement with Bank of America N.A. is a key step towards creating long-term value for Synopsys’ shareholders. The repurchase program demonstrates the company’s commitment to enhance returns and increase shareholder value.

Market Price

Synopsys, Inc. announced on Thursday that it has entered into a $300M share repurchase agreement with Bank of America N. A. The news coverage surrounding the announcement was largely positive, with many praising the move as a smart decision in light of Synopsys’ strong business performance. At the time of writing, the stock price of Synopsys had reacted positively to news of the repurchase agreement, opening on Thursday at $360.0 and closing at $365.5, up 2.9% from its previous closing price of $355.1. Investors are likely to continue closely monitoring the company’s stock for any potential changes or developments. Live Quote…

Analysis

As GoodWhale, we recently completed an analysis of the financials of SYNOPSYS. Through our Star Chart, we classify SYNOPSYS as a ‘gorilla’ – a type of company that has been able to maintain high and steady revenue or income growth due to its strong competitive advantage. Such a stable and successful business is likely to draw in interested investors from a variety of backgrounds. In addition, GoodWhale also reviews a company’s health score. According to our analysis, SYNOPSYS has a 10/10 score in terms of cashflows and debt – meaning that it is capable of sustaining future operations if conditions become difficult. Furthermore, its financials show that it is strong in growth and profitability, medium in asset, and weak in dividend. All of these factors contribute towards making SYNOPSYS an attractive opportunity for investors looking to get involved with a holding with long-term potential. More…

Summary

Synopsys recently announced a $300 million share repurchase agreement with Bank of America N.A. This is seen as a positive development by investors, as it indicates the company’s confidence in their performance and stability. This repurchase agreement reflects Synopsys’ commitment to maximizing shareholder value, which continues to make it an attractive choice for investors. Increased demand for Synopsys’ products and services has resulted in the company’s success and growing market share, which makes it an attractive option for investors looking for long-term growth.

Investors should also note that the company has a long history of innovation, making it a strong competitor within the semiconductor industry. The continued success of Synopsys gives investors confidence that their investment will provide solid returns in the years to come.

Trending News 🌧️

Link Administration, a leading financial consultancy firm, is in the midst of negotiations with the Waystone Group over the potential sale of its UK unit. According to reports, the Waystone Group is looking to purchase the unit with the intention of expanding their own operations and taking advantage of Link Administration’s expertise in the area. The negotiations between Link Administration and the Waystone Group have been ongoing for several weeks now, and a deal is expected to be reached soon. While details of the sale remain confidential, it is believed that the se will include a substantial settlement for Link Administration, as well as a detailed agreement regarding the transition of the UK unit to the Waystone Group. The negotiations have reportedly been amicable, with both parties working together towards an agreement that is mutually beneficial. Should the sale go through as expected, it will represent a major milestone for both Link Administration and the Waystone Group.

For Link Administration, it will be a significant opportunity to expand its global reach and allow it to focus more on other areas of its business. For the Waystone Group, it will provide access to the expertise of Link Administration and provide the Group with a chance to enter the lucrative UK market. As negotiations continue to progress between Link Administration and the Waystone Group, there is much anticipation as to what this potential sale could mean for both companies. It is hoped that a successful deal will be reached soon, providing both companies with an opportunity to benefit from the other’s expertise.

Share Price

Link Administration (LINK) has announced on Monday that it is negotiating with Waystone Group for the sale of its UK unit. The news pushed the stock up by 2.4%, from its previous closing price of AU$2.1, to AU$2.1 when the market closed at the end of the day. LINK is confident that the sale will generate positive economic benefits for both companies and assist in the growth and expansion of the business.

Additionally, it is expected that the proceeds from the sale will be reinvested into other strategic opportunities, creating a stronger platform for LINK’s future. The deal is yet to be finalized, however LINK expressed optimism about the potential terms of the agreement and believes that it can be beneficial for both parties. The negotiation process will be carefully managed to ensure that all stakeholders are taken into consideration. Since the announcement, investors have responded positively to LINK’s decision to pursue the sale, with their stock rising on Monday. All eyes are now on LINK and Waystone Group as they move towards sealing the deal, which is expected to be agreed within the next few weeks. Live Quote…

Analysis

As GoodWhale, we conducted an analysis of LINK ADMINISTRATION’s fundamentals. After carefully assessing the company’s financial and business aspects, we determined that LINK ADMINISTRATION is a medium risk investment. During our examination, we detected 3 risk warnings in the income sheet, balance sheet, and cashflow statement. For further details regarding our research and findings, we invite you to become a registered user and check them out. More…

Summary

Link Administration has recently entered into an agreement with Waystone Group to sell their UK unit. This move is likely to prove beneficial for Link Administration as it will help them streamline their operations and increase their focus in the areas that are more profitable. The sale of the UK unit is expected to provide Link Administration with cash, reduce their overall cost base and potentially expand their presence in other markets. It is likely that Link Administration will be able to use the proceeds to further their growth strategy in the future.

This transaction could provide investors with an opportunity to gain exposure to Link Administration at a suitable price. Investors should consider the potential upside as well as any risks associated with this investment before making a decision.

Trending News 🌧️

MaxLinear and Airgain have joined forces to develop a revolutionary massive MIMO reference design to improve radio performance. By combining their respective high performance technologies – Airgain’s 64T64R antenna array and MaxLinear’s MXL1550 8T8R transceiver – they are now able to provide improved spectrum reuse and greater radio performance. This combined technology is powered by innovative AI/ML-powered beamforming algorithms, which allow for the analysis of large amounts of data in order to find the most suitable transmission path for each user. This approach enables more efficient use of the available spectrum and makes for a more reliable connection. The reference design created by MaxLinear and Airgain is designed to meet the demands of modern wireless networks, giving users better performance than ever before.

With its AI-driven beamforming technology, users can experience improved network capacity, lower latency, more reliable connections and more efficient use of the spectrum. MaxLinear and Airgain’s collaboration brings together expertise in both radio frequency and machine learning to create a reference design with unrivaled potential for enhancing wireless performance. This powerful combination of advanced technologies can bring an unparalleled level of radio performance to wireless networks.

Price History

On Thursday, MAXLINEAR, a leading developer and marketer of radio frequency (RF) semiconductor solutions, and Airgain, Inc., a leading provider of advanced antenna technologies, announced a new partnership to develop a revolutionary massive MIMO reference design. This development is expected to revolutionize RF radio performance and improve both cellular and Wi-Fi wireless connectivity. The news of the MAXLINEAR and Airgain partnership has been met with a largely positive response in the media.

Upon the announcement, MAXLINEAR’s stocks stood at $35.0 before closing at $34.8 in the stock market, a gain of 2.6% from its last closing price of $33.9. Analysts predict this development could make MAXLINEAR a leader in the wireless semiconductor industry while allowing Airgain to become a major player in the tech market. Live Quote…

Analysis

As GoodWhale, I have conducted an analysis of MAXLINEAR’s fundamentals. According to the Star Chart, MAXLINEAR is classified as a ‘gorilla’ – a type of company that has achieved stable and high revenue or earning growth due to its strong competitive advantage. Investors who are looking for such companies may be interested in MAXLINEAR. MAXLINEAR has a high health score of 10/10 with regard to its cashflows and debt, which indicates that the company is capable to ride out any crises without the risk of bankruptcy. In addition, MAXLINEAR is strong in growth, profitability and medium in asset, whereas it is weak in dividend. Therefore, investors who are looking for long-term growth and are not particularly interested in dividend yields may be interested in MAXLINEAR. More…

Summary

MaxLinear and Airgain recently announced the joint development of a revolutionary massive MIMO reference design to improve the performance of radio signals. This cutting-edge technology has been favorably received by investors, and is seen as a major development in the field of radio technology. As a result, MAXLINEAR’s stock has climbed as investors look forward to further advances from the partnership that could be exploited to benefit their portfolios. Analysts with a favorable outlook on the stock believe that investing in MAXLINEAR could be highly beneficial for investors in the long run.

Trending News 🌧️

MaxLinear and Airgain recently announced their partnership to create a new reference design for enhanced spectrum reuse with massive MIMO radio units. This reference design combines the high performance technologies of both companies, including Airgain’s 64T64R antenna array and MaxLinear’s MXL1550 8T8R transceiver, to achieve improved spectrum reuse. The reference design is also powered by AI/ML-powered beamforming algorithms, enabling operators to leverage advanced technology to ensure superior network performance and efficient spectrum utilization.

In addition, the design helps operators boost wireless capacity while simplifying their investments in wireless infrastructure. This move is expected to significantly benefit operators as they can now leverage existing spectrum to support larger numbers of users while leveraging ongoing advances in antenna technologies. With this technology, operators can optimize their deployments and take advantage of the latest advances in artificial intelligence and machine learning to provide a superior user experience. Furthermore, the reference design is optimized for 5G NR and other advanced networks, allowing operators to make the most of their network investment and gain the highest return on it. The combined technologies of MaxLinear and Airgain offer a one-stop solution for operators looking to maximize their spectrum reuse with massive MIMO radio units. The reference design should help operators quickly deploy their networks with minimum cost and effort, while also receiving the benefits of enhanced spectrum reuse and AI-powered beamforming algorithms.

Stock Price

MaxLinear Inc.(MAXLINEAR) recently partnered with Airgain to create a reference design for enhanced spectrum reuse with massive multiple-input multiple-output (MIMO) radio units. This news has been met with mostly positive sentiment, as investors and analysts view this as a step forward in expanding MaxLinear’s portfolio of connectivity solutions. On Thursday, MAXLINEAR stock opened at $35.0 and closed at $34.8, a 2.6% increase from the prior closing price of 33.9. This indicates a bullish sentiment towards the company and the new reference design. Live Quote…

Analysis

At GoodWhale, we performed an analysis of MAXLINEAR’s wellbeing and found that the fair value of MAXLINEAR share is around $56.3 as determined by our proprietary Valuation Line. Currently, MAXLINEAR stock is being traded at $34.8, which is a 38.2% discount from its fair value. This presents a significant investment opportunity for those seeking to buy the stock at a significant discount. More…

Summary

MAXLINEAR, a provider of radio-frequency (RF) and mixed-signal semiconductor solutions, has recently partnered with Airgain, a provider of advanced antenna technologies, to create a reference design for enhanced spectrum reuse with massive MIMO radio units. This new design combines MAXLINEAR’s power-efficient RF transceiver and Airgain’s antenna technology to provide an improved signal range and spectrum efficiency. The design will also enable MAXLINEAR to deliver high-performance, low-cost solutions for next-generation wireless applications.

Investment analysts have praised the new joint effort, leaving investors optimistic about the future prospects for MAXLINEAR’s share price. With its leading technology, strong partnerships and growing demand for large-scale network deployments, MAXLINEAR is positioned to benefit from the expanding market for radio frequency solutions.

Trending News 🌧️

China BlueChemical has achieved remarkable success in recent years, with its total shareholder returns far outpacing the growth in its earnings. This steady growth in shareholder returns can be attributed to the company’s strong management, strategic investments, and expanding market share. China BlueChemical has been undertaking a number of strategic acquisitions that have aided its success and have resulted in increased shareholder returns. These acquisitions have included the purchase of a stake in a leading specialty chemicals distributor, and expansion into the petrochemical industry.

Additionally, the company has managed to improve its efficiency and productivity, allowing it to extract significant returns from its investments. The company’s efforts to broaden its customer base have also contributed to the impressive growth in shareholder returns. China BlueChemical has reached out to new markets, having established a presence in countries such as India and the United States. Additionally, the company has invested heavily in research and development, creating innovative products that are being well-received by customers. Due to the success of its investments, China BlueChemical’s shareholder returns have been outperforming its earnings growth over the last three years. The company’s impressive growth is a testament to its dedication to prudent business management and strategic decision-making. As it continues to pursue further expansions, investors can expect to see even greater returns from China BlueChemical in the future.

Share Price

China BlueChemical’s shareholder returns have been soaring, far outstripping the growth in earnings. As of the time of writing, media sentiment has been mostly positive with investors buying into the potential of the chemical giant. Tuesday saw CHINA BLUECHEMICAL stock open at HK$1.9 and close at HK$1.9, down by 0.5% from its previous closing price.

However, the company’s long-term performance remains highly impressive. Over the last five years, China BlueChemical’s returns have quintupled, averaging an impressive 26% annually in the past three years. Live Quote…

Analysis

At GoodWhale, we have carefully analyzed the financials of CHINA BLUECHEMICAL. Based on our proprietary Valuation Line, we have calculated that the fair value of their share is around HK$2.2. However, the current trading price is HK$1.9, which is a fair price that is undervalued by 12.6%. Therefore, it is beneficial to buy the stock at its current price as it is a great deal. More…

Summary

China BlueChemical Ltd. has seen stellar shareholder returns in recent months, outpacing its earnings growth. Analysts consider this trend to be a promising indicator of the company’s future performance, as investors flocking to the stock are likely betting on the firm’s long-term potential. China BlueChemical has seen its share price increase significantly amid positive news coverage and market sentiment, making it an attractive option for investors. Analysts believe that the company is well-positioned to benefit from the current market environment and capitalize on potential growth opportunities in the long-term.

Trending News 🌧️

QuantumScape Corporation has experienced a pullback in their stock price, reflecting a mixed long-term outlook. Investors should take into account both the risks and benefits associated with the company before making any decisions. The company has a Hold investment rating, as current market conditions are not as favorable as those of some of its competitors.

However, the stock price has been adjusted to account for these differences, so investors should still be able to find value in QuantumScape Corporation’s stock. QuantumScape Corporation’s focus on developing and commercializing solid-state batteries provides potential benefits for investors. These batteries are positioned to increase the range and safety of electric vehicles, which will be attractive to the growing consumer demand for green transportation. This emphasis on innovation could lead to long-term growth for the company, if successful. On the other hand, the development of this technology is still in its early stages and there is no guarantee that it will be successful.

Additionally, the company may be subject to intense competition from other established players in the industry. At this time, investors should view QuantumScape Corporation’s stock with a Hold rating. Although there are potential long-term benefits, they must be taken into consideration in light of the risks associated with the company’s developments. However, the stock price has been adjusted to reflect this and investors can still find value in QuantumScape Corporation’s shares. Ultimately, it is up to each investor to analyze the data and come to their own conclusion regarding whether or not they should invest in QuantumScape Corporation.

Share Price

The news coverage surrounding QuantumScape Corporation has been generally positive, but on Thursday the company saw its stock price pull back. The opening price for the day was $10.1 and the closing price was $9.6 which represented a 2.4% decrease from the prior day’s closing price of $9.9. This has caused investors to reassess their long-term outlook and while they may remain optimistic, they also recognize that this pullback can be seen as a sign of caution. As such, the current consensus among investors is to hold their QuantumScape Corporation investments but to monitor any further developments in the market related to the company. Live Quote…

Analysis

GoodWhale is the perfect platform for analyzing the financials of QUANTUMSCAPE CORPORATION. After taking into consideration all of their current financials, our proprietary Valuation Line gives the intrinsic value of the QUANTUMSCAPE CORPORATION share at around $23.3. This means that the current trading price of $9.6 for QUANTUMSCAPE CORPORATION stock is drastically undervalued by 58.8%. Our advice is to purchase QUANTUMSCAPE CORPORATION stock now before the price rises as more investors flock to capitalize on this great opportunity. More…

Summary

QuantumScape Corporation, a leader in solid-state battery technology, has recently seen a notable pullback in its stock price. Despite the recent decline, analysts have continued to maintain a mostly positive outlook for the company in the long-term. Most investment ratings have kept the company at a “hold” recommendation, reflecting cautious optimism for their technology.

While there is still uncertainty about QuantumScape’s future, investors believe that the company’s potential for revolutionary battery technology is still largely untapped. Despite the pullback, many analysts remain confident that QuantumScape will continue to make strides in the industry and see its stock rise over time.

Trending News 🌧️

QuantumScape Corporation has seen a pullback in its stock price, indicating that investors have assessed the risks involved in the company’s operations. Though the business model of QuantumScape is attractive, the profitability timeline and valuations do not compare to those of its peers. As such, the recent pullback in its stock price has taken these factors into account. The outlook for QuantumScape is uncertain. On one hand, its promising battery technology holds great potential for cost-effective energy storage solutions in the future.

However, the company faces challenges related to its supply chain, scalability, and patents. These risks need to be taken into consideration when assessing an investment decision. In light of these risks and potential opportunities, a Hold rating is an appropriate assessment for QuantumScape Corporation’s stock. While the company presents attractive possibilities, the associated challenges must not be ignored. Taking into account all factors, QuantumScape is a solid investment opportunity with potential for growth in the future.

Price History

The media exposure surrounding QuantumScape Corporation has been largely positive since its initial public offering. Despite the overwhelmingly favorable outlook, the company’s stock price pulled back on Thursday due to assessed risks and opportunities. The share price opened at $10.1 and closed at $9.6, a 2.4% drop from its previous closing price of $9.9.

Although the cause of the pullback remains speculative and uncertain, speculators attribute it to a careful assessment of the balance between risks and opportunities for the company’s future growth. While the market may be perceiving some risks that the company faces, it is important to note the potential opportunities that could arise from its innovative technology and ambitious goals. Live Quote…

Analysis

At GoodWhale, we recently conducted an analysis of QUANTUMSCAPE CORPORATION’s wellbeing. Based on our Risk Rating, QUANTUMSCAPE CORPORATION has been determined to be a high risk investment in terms of both financial and business aspects. From the cashflow statement, non-financial and financial journals, we were able to detect a total of three risk warnings. Our comprehensive system allows us to thoroughly comb through a company’s financial wellbeing which only registered users are eligible to access. If you’re interested in learning more, consider signing up to become a registered user today! More…

Summary

QuantumScape Corporation is an innovative electric vehicle battery company that recently saw its stock price pull back after a surge in media attention. Despite the pullback, investors have evaluated the risks and opportunities surrounding the company with mostly positive sentiment. Analysts have highlighted QuantumScape’s advanced lithium-metal technology as a key benefit, as its dense energy storage capacity is anticipated to surpass the norm in the industry.

Investing opportunities are further enhanced by other potential industry disruptions that QuantumScape could bring through its research and development. There is no guarantee of success, however, and investors must weigh the risks of investing in a relatively untested technology-based enterprise.

Trending News 🌧️

Freshpet Inc.’s stock closed at $62.45 yesterday, a decrease of -7.22% from its previous closing price of $67.31. This marks a historic low for Freshpet Inc.’s stock and gives an overall feeling of uncertainty about the company’s position in the market. With this decrease in price, investors are now facing the difficult question of whether or not it is worth investing further in Freshpet Inc.’s stock. It is likely that analysts will be monitoring Freshpet Inc.’s stock prices closely over the coming weeks in order to assess whether or not there may be a chance for the company’s stock prices to rebound.

Market Price

On Thursday, Freshpet Inc. stock closed at $62.45, which is a 7.22% decrease compared to its previous closing price. This news, however, was overshadowed by the mostly positive news surrounding the company. At the time of writing, the stock opened at $63.4 before dropping to $62.4, representing a 1.3% decrease from its last closing price of 63.2. Despite this setback, Freshpet Inc. is still making strides in the industry, with shareholders and investors remaining optimistic about its future prospects. Live Quote…

Analysis

At GoodWhale, we performed an analysis on the wellbeing of FRESHPET. After our analysis, we found that FRESHPET fell into the “Cheetah” category on our Star Chart, meaning they had achieved high revenue or earnings growth but were considered less stable due to lower profitability. In terms of what investors might be interested in FRESHPET, their health score of 7/10 considering their cashflows and debt suggests that the company is likely in its most stable yet, able to safely ride out any crisis without the risk of bankruptcy. However, we did find that FRESHPET is strong in terms of asset and growth, but is only medium in terms of profitability and weak in terms of dividend. Thus, investors looking for short-term financial gain may want to look for more stable and profitable companies. More…

Summary

Investing in Freshpet Inc. has been an unpredictable market recently, as the stock closed at $62.45 on April 8th, a 7.22% decrease over its previous closing price. Despite the slump, analysts remain optimistic about the brand’s future prospects due to the positive news currently surrounding the company. Going forward, investors should closely monitor the stock in order to gauge its inside and outside performance.

Additionally, current shareholders may choose to diversify their portfolio in other more stable markets in order to reduce risk. Investors should also be aware of significant upcoming news from the company and any potential changes to market conditions that could affect the stock’s performance. Overall, Freshpet Inc. looks to remain a potentially lucrative investment for those willing to take on the associated risks.

Trending News 🌧️

Medical Properties Trust (MPT) announced the retirement of Emmett McLean, who has been a part of the trio of founders of the REIT since 2003. McLean served as Executive Vice President, Chief Operating Officer, and Secretary of MPT for more than twenty years. During this time he was responsible for managing and directing the asset management, underwriting, human resources, and IT departments. McLean’s retirement on September 1st marks the end of an incredible tenure that has seen the company grow from its humble beginnings in 2003 to its current status as a leader in medical real estate.

His dedication, commitment to excellence, and passion have been instrumental in building MPT into the top-tier organization it is today. The leadership at MPT extends its sincere gratitude to McLean for his hard work and dedication over the years. The team wishes him the best in his future endeavors and looks forward to continuing his legacy of success in the years to come.

Share Price

On Thursday, MEDICAL PROPERTIES TRUST announced the retirement of founding member Emmett McLean after more than 20 years of service. The news received mostly positive media coverage, due to McLean’s significant contributions to the company. However, the same day saw a large drop in the stock price of Medical Properties Trust, with shares opening at $12.1, and closing at $11.1 – a decrease of 8.7% from the previous closing price of $12.2. This sharp decline may be due to investors’ reaction to the news of McLean’s retirement, although no direct connection has been made. Live Quote…

Analysis

At GoodWhale, we analyzed MEDICAL PROPERTIES TRUST’s financials and gave it a medium risk rating. This rating is based on the evaluation of the company’s financials and business aspects. However, we did detect some threats that should be taken into account. In particular, our analysis indicated two risk warnings in the balance sheet and cashflow statement. For more detailed information, please register on goodwhale.com to check the full report. It’s important to make informed decisions with your money, and at GoodWhale we are dedicated to providing reliable information to help you make the best investments for your future. More…

Summary

Medical Properties Trust (MPT) recently announced the retirement of Emmett McLean, a founding member and long-time service provider. Despite the seemingly positive media coverage of the event, MPT’s stock price fell on the same day. Investors should take this as a sign that the market may not be as optimistic about the company’s prospects going forward as it had previously been. They should further analyze potential impacts McLean’s retirement may have on the company’s financial performance and strategize accordingly.

Additionally, they should review the company’s dividend policy, financial health, and other key metrics before making any investment decisions.

Trending News 🌧️

Chorus Limited has announced that its shareholders will be rewarded with an increased dividend payout compared to the previous year. This move comes as part of the company’s ongoing commitment to deliver sustainable returns to its investors. A larger dividend payout has been seen as a sign of appreciation for their support and loyalty over the years. The increased dividend payout will benefit the long-term financial position of shareholders, providing them with greater returns on their investments. It is believed that the increase in dividend payout will help attract new investors and retain existing investors, helping to strengthen the company’s financial foundations.

Additionally, the increased dividend payout will help to increase shareholder confidence, providing reassurance in the form of greater returns. Overall, Chorus Limited’s decision to reward shareholders with a larger dividend payout is a positive move that will help to build trust and loyalty amongst its investors. The increased dividend will help to provide greater returns and will help bolster the company’s overall financial position.

Dividends

CHORUS LIMITED is rewarding its shareholders with an increased dividend payout. Over the last three years, CHORUS LIMITED has issued a steady annual dividend per share of 0.28 NZD. The dividend yields for the years 2022 to 2022 have remained consistent as well, yielding an average of 4.02%.

This indicates that any investor who is looking for dividend stocks may want to consider adding CHORUS LIMITED to their list of consideration. With the increased dividend payout, shareholders of CHORUS LIMITED can look forward to higher returns on their investments.

Price History

CHORUS LIMITED has recently been covered positively in the media, thanks to its increased dividend payout to shareholders. On Thursday, CHORUS LIMITED stock opened at NZ$8.0 and closed at NZ$8.1, up by 1.4% from its previous closing price of NZ$8.0. This increase clearly demonstrates that investors are responding favorably to the news of higher dividends by purchasing more stock. This new dividend payout could potentially provide investors with a greater return on their investment than previously expected. Live Quote…

Analysis

GoodWhale has looked closely at the financials of CHORUS LIMITED and our proprietary Valuation Line indicates its intrinsic value to be around NZ$7.6. However, the stock is currently trading at NZ$8.1 – making it 6.1% overvalued. We believe that CHORUS LIMITED stock is a fair price, but investors should be aware of the slight overvaluation and make an appropriate decision based on their assessment. More…

Summary

Chorus Limited (CHOR.AX) has recently announced an increased dividend payout to reward its shareholders. Analysts suggest attractive long-term prospects for the company, based on its well-diversified revenue sources, extensive share repurchase program, and healthy balance sheet. With current market sentiment being positive, investors may consider CHORUS as a good stock for accumulating in their portfolios.

Trending News 🌧️

Regeneron Pharmaceuticals recently announced that the US Food and Drug Administration (FDA) has accepted their application for priority review of their 8 mg high-dose version of the popular eye treatment, Eylea. This version is intended to treat both macular degeneration and diabetic macular edema. This approval was facilitated by Regeneron’s partnership with Bayer AG and the use of a priority review voucher. As part of the priority review process, Regeneron must supply additional information and clinical data to the FDA for review. The decision is expected to come on June 27, 2020. The acceptance of this application marks a major milestone in regeneron’s history and is likely to further elevate its standing in the pharmaceutical industry.

Regeneron maintains a strong commitment to developing drugs to improve patients’ health and quality of life. The approval of this new 8 mg version of Eylea is a testament to their dedication, and to the effectiveness of their products. The acceptance of Regeneron’s application for priority review is a major milestone for the company and a great step forward in their efforts to provide effective treatments for macular degeneration and diabetic macular edema patients. This approval could drastically improve the lives of those affected by these conditions and could be a major victory for Regeneron and their partners at Bayer AG.

Share Price

On Thursday the US Food and Drug Administration (FDA) accepted Regeneron Pharmaceuticals’ high-dose Eylea Treatment for Macular Degeneration and Diabetic Macular Edema for Priority Review, and news regarding this event has been mostly positive. This event had a visible positive effect on the stock market value of Regeneron Pharmaceuticals as their stock opened at $744.8 and closed at $759.7, representing an increase by 1.5% over the previous closing price of $748.1. The Priority Review will allow the FDA to take action faster than they usually would, which is an important step in the fight against these two conditions. This news bodes well for Regeneron Pharmaceuticals and the many sufferers of Macular Degeneration and Diabetic Macular Edema. Live Quote…

Analysis

At GoodWhale, we recently conducted an in-depth analysis of REGENERON PHARMACEUTICALS’s financial and business wellbeing. After carefully considering the company’s risk profile, we have assigned REGENERON PHARMACEUTICALS a medium risk rating. We have detected two risk warnings in their balance sheet and cashflow statement, which could be cause for concern. As such, we would encourage potential investors to take a closer look at these before making any decisions. If you would like to learn more about REGENERON PHARMACEUTICALS and their risk profile, register with us now and we’ll be more than happy to provide you with the detailed information. More…

Summary

Regeneron Pharmaceuticals’ high-dose Eylea treatment is currently undergoing US FDA Priority Review for the treatment of Macular Degeneration and Diabetic Macular Edema. The news has led to positive media coverage, making it an attractive investment opportunity. Regeneron Pharmaceuticals’ stock has already seen considerable appreciation and offers one of the best returns in the healthcare sector.

Furthermore, the drug has a very good outlook for approval given its impressive efficacy and safety profile. Investors in Regeneron Pharmaceuticals have potential for substantial returns in the coming months, but should also be mindful of the potential risks associated with investing.

Trending News 🌧️

Analysts have recently reaffirmed their positive view of Harmony Biosciences Holdings, reiterating their outperform rating and adjusting the price target range to $60 from $71. Mizuho is among the firms to maintain its buy rating on the company. Despite this recent reduction in the target price, analysts remain confident in the company’s performance and future prospects. Harmony Biosciences Holdings is a specialty pharmaceutical company that focuses on developing and commercializing treatments for underserved patient populations that are suffering from central nervous system disorders.

The company recently announced positive results from its Phase 3 trial of Wakix, its lead product, and is also developing a pipeline of novel therapies for various neurological disorders such as narcolepsy and Huntington’s disease. Given the encouraging data from the trial and the potential of its upcoming drugs, Harmony Biosciences Holdings is still viewed as an attractive investment option by many analysts. With this in mind, the company is well-positioned to provide value to both shareholders and the wider patient population.

Price History

Harmony Biosciences Holdings remains a favorable investment as the news sentiment continues to be mostly positive. On Thursday, the company’s stock opened at $46.3 and closed at $46.1, down 0.4% from the prior closing price of $46.3. Although the price target has been adjusted to $60 from $70, the overall sentiment is still optimistic. Investors should have faith in Harmony Biosciences Holdings as it continues to generate positive news sentiment. Live Quote…

Analysis

At GoodWhale, we analyze HARMONY BIOSCIENCES’s fundamentals for investors to make better decisions. Our proprietary Valuation Line shows that the fair value of HARMONY BIOSCIENCES share is around $57.3. If we look at the current market price, the stock is trading at $46.1, implying that it is undervalued by 19.5%. This gives investors an opportunity to buy the stocks below the fair value. Thus, investors can gain higher returns in the long run by investing in HARMONY BIOSCIENCES’s stocks. More…

Summary

Harmony Biosciences Holdings has recently been rated “Outperform” by analysts, with its price target adjusted from $70 to $60. So far, the sentiment amongst investors has been mostly positive, as the stock has seen a steady uptick in value. With a strong balance sheet and long-term outlook, Harmony Biosciences appears to be an attractive investment opportunity with considerable upside.

The company offers a diverse portfolio of products that should provide a healthy stream of income, and it has various strategic partnerships to further expand its product offerings. Overall, Harmony Biosciences looks to be well-positioned for future growth and success.

Trending News 🌧️