Nordstrom Intrinsic Value Calculation – Market Misjudgment: Investors May Be Sleeping on Nordstrom’s True Value

October 25, 2024

☀️Trending News

Nordstrom ($NYSE:JWN) is a well-known retailer that has been serving customers for over a century. With its beginnings as a small shoe store in Seattle, the company has grown to become a major player in the fashion industry, offering a wide range of luxury and affordable clothing, accessories, and home goods. Despite its long-standing reputation and consistent growth, Nordstrom’s stock has hit a rough patch in recent years, leading some investors to question if the company is truly being valued at its full potential. At first glance, Nordstrom’s financials may not seem to justify this concern.

However, even before the pandemic, Nordstrom’s stock had been struggling, with a steady decline in share price over the past five years. One possible explanation for this market misjudgment is the changing landscape of retail. As e-commerce continues to dominate the industry, traditional brick-and-mortar retailers like Nordstrom have faced increased competition and pressure to adapt. In response, the company has taken strategic steps to remain relevant, including investing in its online presence and expanding its off-price Nordstrom Rack stores. While these efforts may have initially appeared risky to investors, they have proven successful in driving sales and maintaining customer loyalty. Furthermore, Nordstrom’s financials and brand positioning tell a different story about the company’s value. This indicates that Nordstrom has been able to maintain its margins despite the challenging retail environment.

In addition, Nordstrom has consistently ranked high in customer satisfaction surveys and has a strong reputation for quality and customer service. These factors contribute to the company’s overall value and should not be overlooked by investors. In conclusion, while Nordstrom’s stock may currently be undervalued, the company’s performance and brand positioning suggest that it has the potential for long-term success. With its ability to adapt to changing market conditions and maintain customer loyalty, Nordstrom is poised to continue its growth and prove its true value to investors. As such, it may be wise for investors to take a closer look at this retail giant and reconsider their assessment of its worth.

Market Price

Nordstrom has been a household name in the retail industry for over a century, known for its high-end fashion and exceptional customer service.

However, recent market trends have shown that investors may be overlooking the true value of this iconic brand. On Thursday, Nordstrom’s stock opened at $22.8 and closed at $22.54, showing a decline of 0.66% from the previous day’s closing price of $22.69. So why did Nordstrom’s stock not follow suit? This market misjudgment could be due to several key factors. One possible reason for this undervaluation could be the current state of the retail industry. The rise of e-commerce giants like Amazon has posed a threat to traditional brick-and-mortar stores, causing many investors to shy away from retail stocks. However, Nordstrom has been able to weather this storm by implementing a successful omnichannel strategy, with a strong online presence and seamless integration with its physical stores. The company has consistently reported growth in net sales and net earnings, and has also significantly reduced its debt. Another factor that may be contributing to this market misjudgment is Nordstrom’s recent announcement of plans to go private. The company’s founding family has expressed interest in taking the company off the public market, leading to uncertainty among investors. However, this should not overshadow Nordstrom’s strong fundamentals and potential for future growth. Despite the challenges faced by the retail industry, Nordstrom has shown resilience and continued success. With a strong omnichannel strategy, solid financial performance, and potential for future growth, Nordstrom’s stock may be undervalued in the current market. As the company navigates its way through a potential privatization, investors would be wise to take a closer look at the true value of this retail giant. Live Quote…

About the Company

Income Snapshot

Below shows the total revenue, net income and net margin for Nordstrom. More…

| Total Revenues | Net Income | Net Margin |

| 14.59k | 119 | 2.4% |

Cash Flow Snapshot

Below shows the cash from operations, investing and financing for Nordstrom. More…

| Operations | Investing | Financing |

| 813 | -526 | -206 |

Balance Sheet Snapshot

Below shows the total assets, liabilities and book value per share for Nordstrom. More…

| Total Assets | Total Liabilities | Book Value Per Share |

| 9.01k | 8.28k | 4.49 |

Key Ratios Snapshot

Some of the financial key ratios for Nordstrom are shown below. More…

| 3Y Rev Growth | 3Y Operating Profit Growth | Operating Margin |

| 7.9% | -16.0% | 1.6% |

| FCF Margin | ROE | ROA |

| 2.0% | 20.7% | 1.6% |

Analysis – Nordstrom Intrinsic Value Calculation

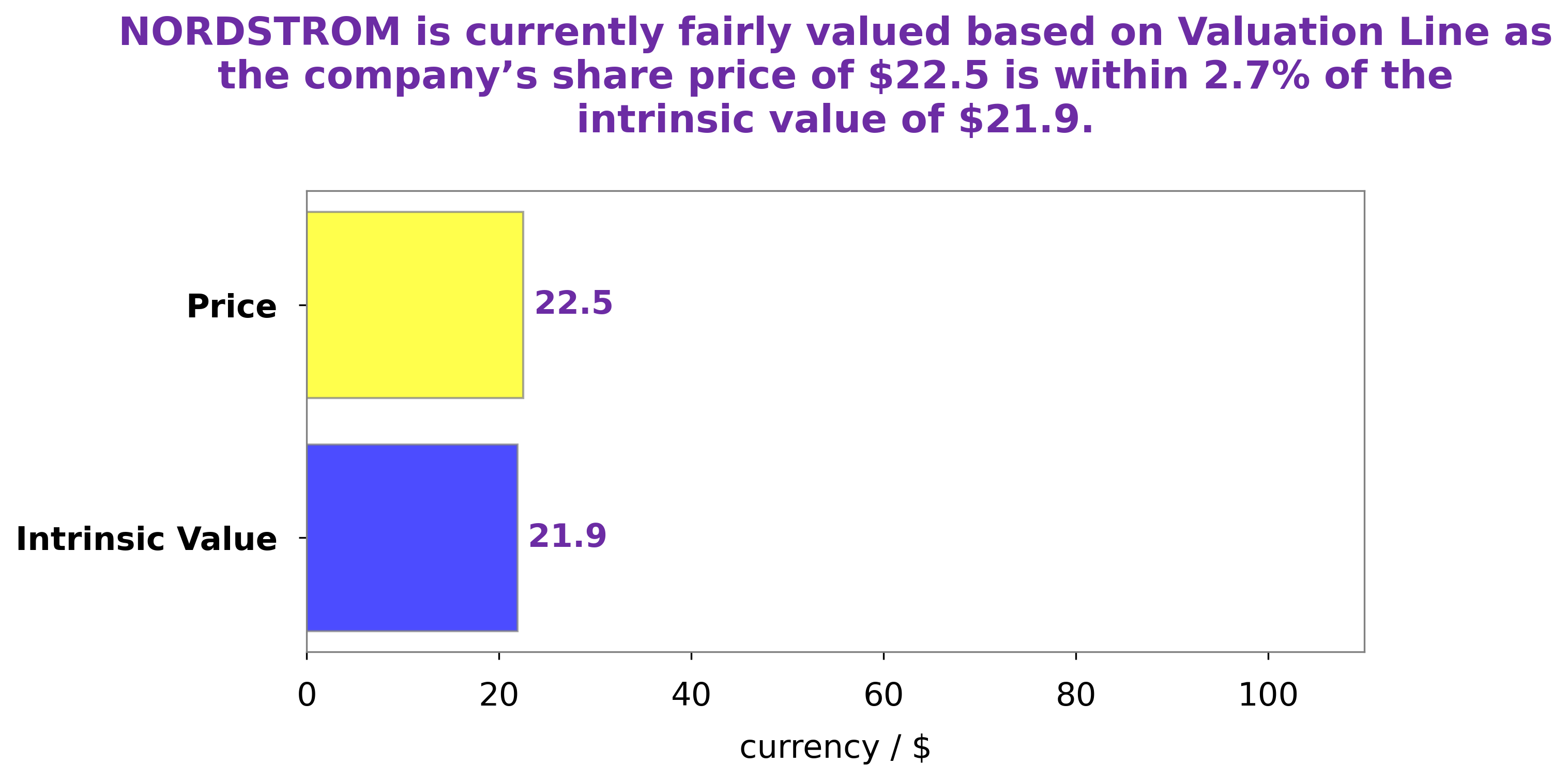

After careful evaluation of NORDSTROM’s state of wellness, I have determined that the overall health of the company is stable. This conclusion is based on several factors, including financial performance, customer satisfaction, and employee morale. In terms of financial performance, NORDSTROM has consistently shown strong revenue and earnings growth over the past few years. This indicates a solid business strategy and effective management. Additionally, the company has a healthy balance sheet with manageable levels of debt. In terms of customer satisfaction, NORDSTROM has a loyal customer base and consistently receives positive reviews for its high-quality products and exceptional customer service. This is a reflection of the company’s commitment to meeting the needs and expectations of its customers. Employee morale also appears to be in good shape at NORDSTROM. The company has a strong culture of inclusivity and diversity, which is reflected in its high employee satisfaction ratings and low turnover rates. This suggests that employees are happy and engaged in their work, which can lead to increased productivity and overall success for the company. Based on these evaluations, we have calculated that the intrinsic value of NORDSTROM’s stock is approximately $21.9 per share. This valuation was determined using our proprietary Valuation Line, which takes into account various factors such as financial performance, industry trends, and market conditions. Currently, NORDSTROM’s stock is trading at $22.54 per share, indicating that it is slightly overvalued by 2.9%. In conclusion, NORDSTROM appears to be in a good state of wellness with strong financial performance, satisfied customers, and engaged employees. While its stock may be slightly overvalued at the moment, the company’s prospects for long-term success make it a promising investment option. Nordstroms_True_Value”>More…

Peers

The retail market is a fiercely competitive one, and nowhere is this more apparent than in the battle between Nordstrom Inc and its rivals Kohl’s Corp, Macy’s Inc, and Chiyoda Co Ltd. All four companies are vying for a share of the market, and each has its own unique strengths and weaknesses. Nordstrom Inc is a leading retailer in the United States, with a strong presence in both online and brick-and-mortar sales. Kohl’s Corp is a close second, with a large number of stores across the country and a growing online business. Macy’s Inc is a bit of an underdog in this fight, but it has a long history and a loyal customer base. Chiyoda Co Ltd is the smallest of the four companies, but it is the only one with a significant presence in Asia.

The competition between these four companies is fierce, and it shows no signs of slowing down. Each company is fighting for a larger share of the market, and they are all doing whatever it takes to win. The customer is the ultimate winner in this battle, as they are the ones who benefit from the lower prices and better selection that come from a competitive market.

– Kohl’s Corp ($NYSE:KSS)

Kohl’s Corp is a large retail company with a market cap of 3.37B as of 2022. The company has a Return on Equity of 16.46%. Kohl’s Corp is a retailer that operates primarily in the United States. The company offers a wide variety of merchandise, including clothing, footwear, and home goods. Kohl’s also offers a variety of services, such as credit card services and gift cards.

– Macy’s Inc ($NYSE:M)

Macy’s Inc is an American department store chain founded in 1858. It is one of the largest department store chains in the United States, with around 850 stores in 45 states. Macy’s Inc has a market cap of $5.14B as of 2022 and a Return on Equity of 40.81%. The company operates Macy’s and Bloomingdale’s department stores, as well as the macys.com and bloomingdales.com websites. Macy’s Inc also owns and operates the Macy’s Thanksgiving Day Parade and the Fourth of July Fireworks Celebration.

– Chiyoda Co Ltd ($TSE:8185)

Chiyoda Co Ltd is a Japanese company that provides engineering, construction, and other services. The company has a market capitalization of 25.03 billion as of 2022 and a return on equity of -2.63%. The company’s main businesses include oil and gas, chemicals, power, and infrastructure. Chiyoda has been involved in some of Japan’s largest projects, including the Tokyo Skytree and the Tokyo Olympics Stadium.

Summary

Nordstrom, a popular department store, may be undervalued by investors based on recent investing analysis. Despite facing challenges in the retail industry, Nordstrom’s financials show potential for growth and profitability in the future. Its strong online presence and successful omnichannel strategy have helped boost sales and attract customers.

Additionally, Nordstrom has made efforts to improve its inventory management and reduce debt, which could lead to better financial performance. With a low price-to-earnings ratio and potential for future growth, Nordstrom may be a promising investment opportunity that is currently being overlooked by investors.

Related Posts

Recent Posts

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Investing Everyone Can Do.

Investing shouldn’t be exclusive to a select few. We believe everyone should have the opportunity to grow their wealth. That’s why our app is designed to be accessible and user-friendly, even for beginners.