Dillard’s Reports Q3 Earnings: Here’s What Investors Need to Know

November 13, 2024

🌥️Trending News

Dillard’s ($NYSE:DDS), a well-known department store chain, recently released its third quarter earnings report. This report is highly anticipated by investors as it gives insight into the company’s financial performance and potential future growth. Due to the pandemic, Dillard’s had to temporarily close some of its stores and face reduced consumer spending. This may be seen as a positive sign for investors, as the company was able to mitigate some of the negative impacts of the pandemic. Another important aspect of Dillard’s earnings report is their inventory levels.

Looking ahead, Dillard’s remains cautious about their future performance due to the uncertainty caused by the pandemic. They stated that they are focused on controlling expenses and managing inventory levels to navigate through these challenging times. In conclusion, while Dillard’s reported a decrease in earnings for the third quarter, their ability to beat analyst expectations and effectively manage inventory may be seen as positive signs for investors during these uncertain times. As the company continues to navigate through the pandemic, it will be important to closely monitor their financial performance and future growth potential.

Earnings

Dillard’s, a popular department store chain in the United States, recently released its earnings report for the third quarter of fiscal year 2024. The report, which covers the period of January 31, 2022, reveals that the company generated a total revenue of 2153.4M USD. This is a slight decrease of 0.4% compared to the previous year.

However, the company’s net income saw a significant increase of 11.1%, reaching 321.2M USD. It is worth noting that Dillard’s has been consistently generating strong revenues in the past few years. In fact, the company’s total revenue has increased from 2153.4M USD to 2158.9M USD in the last three years. This steady growth indicates the company’s strong position in the retail market. Despite the slight decline in total revenue, Dillard’s has managed to increase its net income significantly. This can be attributed to the company’s efficient cost management strategies and strong sales performance. The increase in net income is a positive sign for investors, as it reflects the company’s ability to generate profits even in a challenging retail landscape. Investors should also take note of Dillard’s strong financial position.

Additionally, Dillard’s has a debt-free balance sheet, which gives it a competitive advantage over its debt-ridden competitors in the retail industry. In conclusion, Dillard’s earnings report for Q3 of FY2024 showcases its strong performance and financial stability. While the slight decrease in total revenue may be concerning, the significant increase in net income and steady revenue growth over the years demonstrate the company’s resilience and potential for long-term success. As such, investors should pay close attention to Dillard’s and its future performance in the retail market.

About the Company

Income Snapshot

Below shows the total revenue, net income and net margin for Dillard’s. More…

| Total Revenues | Net Income | Net Margin |

| 6.87k | 738.8 | 10.7% |

Cash Flow Snapshot

Below shows the cash from operations, investing and financing for Dillard’s. More…

| Operations | Investing | Financing |

| 883.6 | -115.6 | -620 |

Balance Sheet Snapshot

Below shows the total assets, liabilities and book value per share for Dillard’s. More…

| Total Assets | Total Liabilities | Book Value Per Share |

| 3.45k | 1.75k | 111.8 |

Key Ratios Snapshot

Some of the financial key ratios for Dillard’s are shown below. More…

| 3Y Rev Growth | 3Y Operating Profit Growth | Operating Margin |

| 15.7% | 88.8% | 13.5% |

| FCF Margin | ROE | ROA |

| 10.9% | 31.9% | 16.8% |

Share Price

Dillard’s, one of the leading fashion and home goods retailers in the United States, recently reported its third quarter earnings for the fiscal year. On Friday, the company’s stock opened at $398.47 and closed at $402.68, representing a 0.68% increase from its previous closing price of $399.96. One of the key factors contributing to Dillard’s positive performance in Q3 was its strong digital sales growth. This is a testament to Dillard’s efforts to boost its e-commerce business and provide customers with a seamless online shopping experience. The company also saw a 3% increase in beauty and wellness sales, while apparel and accessories sales were down by 4%.

Looking ahead, Dillard’s remains cautiously optimistic about the upcoming holiday season. The company has already begun its Black Friday promotions and is offering extended return policies and contactless pickup options to cater to customers’ changing needs during these uncertain times. In conclusion, while Dillard’s saw a decline in overall revenue, its strong digital sales growth and improved net income indicate that the company is adapting well to the challenges posed by the pandemic. With its strategic initiatives and customer-centric approach, Dillard’s is well-positioned to weather the storm and continue to deliver value to its investors. Live Quote…

Analysis

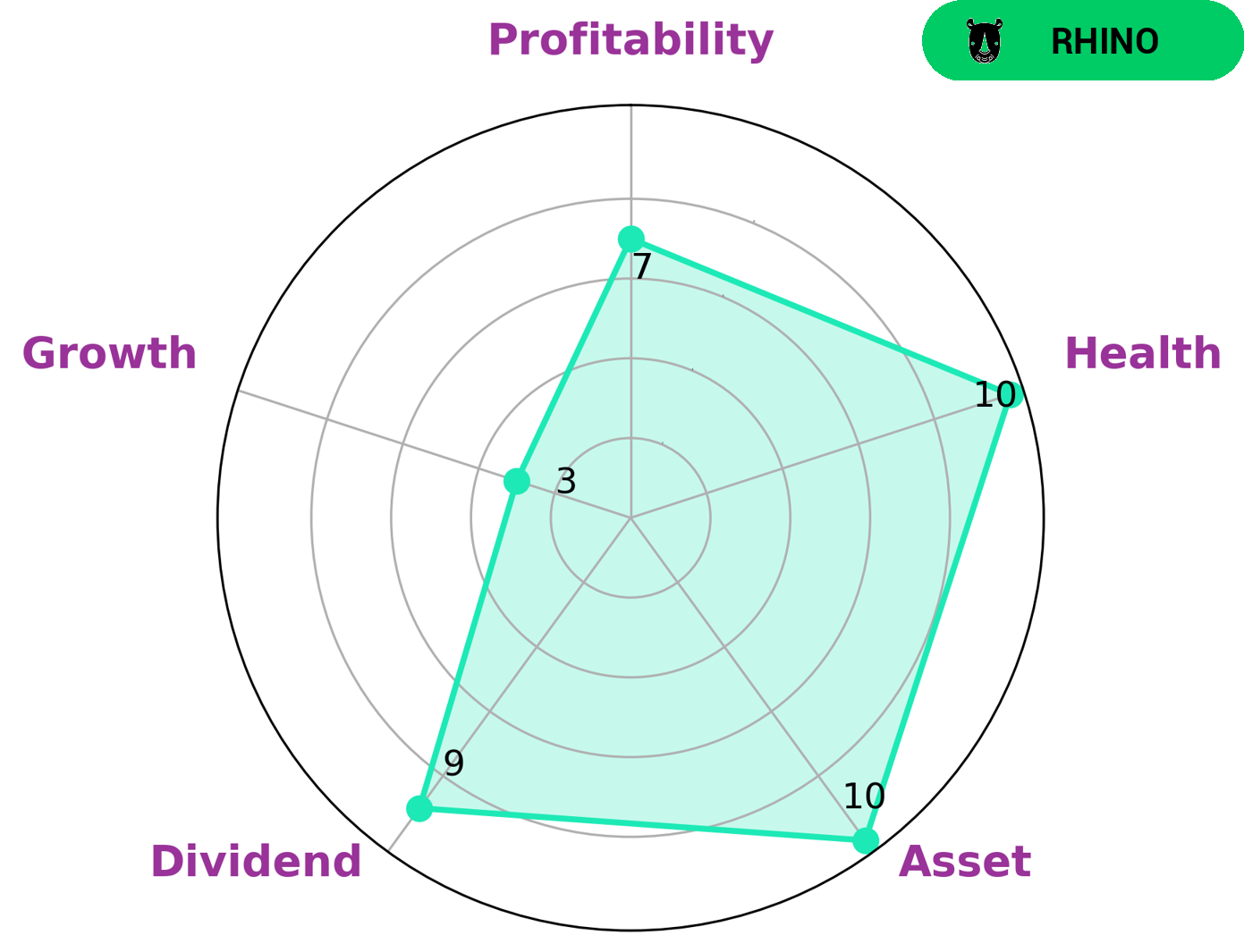

As a fundamental analyst, I closely examined the financials of DILLARD’S and found that it has strong assets, profitability, and dividend. It also has a weak growth potential, which means that it may not see significant revenue or earnings growth in the future. Based on these factors, I would classify DILLARD’S as a ‘rhino’ company, which is a type of company that has achieved moderate revenue or earnings growth. Additionally, its dividend yield may also be attractive to investors looking for regular income from their investments. However, investors seeking high-growth opportunities may not find DILLARD’S as appealing due to its weak growth potential. In terms of financial health, DILLARD’S has a high score of 10/10. This means that the company has strong cash flows and is capable of paying off its debt and funding future operations. This should provide reassurance to investors about the company’s ability to weather any potential financial challenges. Overall, while DILLARD’S may not be a high-growth company, it has strong fundamentals and a solid financial standing. This could make it an attractive investment for investors looking for stability and consistent returns. However, each investor should carefully consider their own investment goals and risk tolerance before making any investment decisions. More…

Peers

Dillard’s Inc, Macy’s Inc, Nordstrom Inc, and Kohl’s Corp are all in competition with each other. They are all trying to get the customer’s money by offering different products and services.

– Macy’s Inc ($NYSE:M)

Macy’s Inc is an American department store chain founded in 1858. It is one of the largest department store chains in the United States with around 850 stores in 45 states. Macy’s Inc has a market cap of 5.04B as of 2022 and a Return on Equity of 40.81%. The company operates in the Retail industry and its headquarters is in Cincinnati, Ohio.

– Nordstrom Inc ($NYSE:JWN)

Nordstrom is an American luxury fashion retailer founded in 1901. It has a market cap of $3.09B as of 2022 and a Return on Equity of 70.09%. Nordstrom operates in over 38 countries and has over 350 stores across the globe. The company offers a wide range of products and services, including apparel, shoes, handbags, jewelry, and beauty products. Nordstrom also has an e-commerce platform that offers free shipping and returns.

– Kohl’s Corp ($NYSE:KSS)

Kohl’s is a leading retailer that operates more than 1,100 department stores across the United States. The company offers a wide variety of merchandise, including apparel, shoes, and accessories for men, women, and children, as well as home products. Kohl’s also provides exclusive lines from top brands such as Nike, Adidas, and Under Armour. In addition to its retail stores, Kohl’s operates an e-commerce site and a mobile app.

Kohl’s has a market capitalization of 3.3 billion as of 2022 and a return on equity of 16.46%. The company has been in operation for over 50 years and has a strong reputation for providing quality merchandise at competitive prices. Kohl’s is committed to offering an enjoyable shopping experience for its customers and provides a variety of convenient shopping options, such as online and mobile shopping.

Summary

Dillard’s, a retail company, is set to release its Q3 earnings report soon. Investors are eagerly anticipating the results and analyzing the stock’s performance. The company’s expenses and inventory levels will also be closely examined.

Investors will also be looking at the company’s digital sales and omni-channel strategy, as online shopping has become increasingly important during the pandemic. The company’s ability to adapt to changing consumer behavior and its financial stability will be key factors in determining its future success and potential for investment.

Related Posts

Recent Posts

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Investing Everyone Can Do.

Investing shouldn’t be exclusive to a select few. We believe everyone should have the opportunity to grow their wealth. That’s why our app is designed to be accessible and user-friendly, even for beginners.