Analyst Lowers Q2 EPS Estimate for Warrior Met Coal, Amidst Uncertain Market Conditions

November 7, 2024

🌧️Trending News

Warrior Met Coal ($NYSE:HCC), Inc. is a leading producer and exporter of premium metallurgical coal for the global steel industry. The company operates two underground coal mines in Alabama and has a strong track record of consistently delivering high-quality coal products to its customers.

However, recent market conditions have posed challenges for Warrior Met Coal, Inc. Amidst the uncertain economic climate, the company’s stock prices have fluctuated, and analysts have been closely monitoring its performance. The Q2 EPS estimate is a measure of a company’s expected earnings per share for the second quarter of the fiscal year. This estimate is an important indicator of a company’s financial health and can significantly impact its stock prices. The fact that an analyst has lowered their estimate for Warrior Met Coal, Inc. suggests that they anticipate a decrease in the company’s profitability in the upcoming quarter. The reason for this decrease in estimated earnings can be attributed to the current market conditions. The ongoing trade tensions between the United States and China have led to a decline in global steel demand, which directly affects the demand for metallurgical coal. Despite these challenges, Warrior Met Coal, Inc. has taken steps to adapt to the changing market conditions and mitigate the impact on its operations. The company has implemented cost-cutting measures and adjusted its production levels to align with market demand. It has also maintained a strong financial position, with a low debt-to-equity ratio, which provides stability during uncertain times. The recent decrease in the Q2 EPS estimate by an analyst serves as a reminder of the potential impact of external factors on a company’s performance. However, the company’s strong track record and proactive measures to address the current challenges position it well for the future. Investors should carefully monitor the company’s performance and its ability to adapt to changing market conditions.

Earnings

In a recent update, an analyst has lowered their estimated earnings per share (EPS) for Warrior Met Coal, Inc. for the second quarter of the fiscal year. This decision was made amidst uncertain market conditions, which have impacted the company’s financial performance in the past. According to the earning report for the fourth quarter of fiscal year 2023, which ended on December 31, 2021, Warrior Met Coal saw a total revenue of 415.54 million USD and a net income of 138.49 million USD. This represents a significant increase of 20.5% in total revenue and 39.0% in net income compared to the previous year.

However, despite this growth, the company’s total revenue has seen a decline from 415.54 million USD to 363.8 million USD in the past three years. With uncertainty in the market and potential challenges ahead, the analyst has adjusted their EPS estimate for the company’s second quarter. This decision highlights the need for Warrior Met Coal to adapt to changing market conditions and develop strategies to sustain its growth in the long term. Overall, while Warrior Met Coal has shown strong financial performance in recent years, it will need to navigate through uncertain market conditions and make strategic decisions to maintain its growth trajectory. The lowered EPS estimate serves as a reminder for the company to continuously evaluate and adjust its strategies to remain competitive in the ever-changing market landscape.

About the Company

Income Snapshot

Below shows the total revenue, net income and net margin for HCC. More…

| Total Revenues | Net Income | Net Margin |

| 1.68k | 478.63 | 29.6% |

Cash Flow Snapshot

Below shows the cash from operations, investing and financing for HCC. More…

| Operations | Investing | Financing |

| 701.11 | -527.21 | -265.18 |

Balance Sheet Snapshot

Below shows the total assets, liabilities and book value per share for HCC. More…

| Total Assets | Total Liabilities | Book Value Per Share |

| 2.36k | 482.61 | 36.03 |

Key Ratios Snapshot

Some of the financial key ratios for HCC are shown below. More…

| 3Y Rev Growth | 3Y Operating Profit Growth | Operating Margin |

| 28.9% | 29.7% | 34.0% |

| FCF Margin | ROE | ROA |

| 12.5% | 19.7% | 15.1% |

Market Price

On Monday, the stock of Warrior Met Coal, Inc. opened at $64.63 and closed at $65.56, showing an increase of 1.42% from its last closing price of $64.64.

However, despite this positive movement in the stock price, an analyst has lowered the Q2 earnings per share (EPS) estimate for the company amidst uncertain market conditions. The lowered Q2 EPS estimate by the analyst suggests that Warrior Met Coal may not meet its earnings expectations for the second quarter of 2021. This could be due to a decline in demand for coal or increased production costs due to disruptions caused by the pandemic.

Additionally, Warrior Met Coal operates in a highly cyclical industry, making it particularly vulnerable to changes in market conditions. The company’s performance is heavily dependent on factors such as global economic growth, energy consumption patterns, and environmental regulations. Furthermore, the company has faced challenges in recent years due to a decline in coal demand and pricing. This has been driven by a shift towards cleaner energy sources and stricter environmental regulations. Although Warrior Met Coal has been able to maintain profitability, any further adverse changes in market conditions could have a significant impact on its financial performance. In conclusion, while Warrior Met Coal’s stock may have shown some positive movement, the lowered Q2 EPS estimate by an analyst highlights the uncertain market conditions that the company is currently facing. Investors should closely monitor any developments in the global economy and energy sector, as they can significantly influence Warrior Met Coal’s financial performance. Live Quote…

Analysis

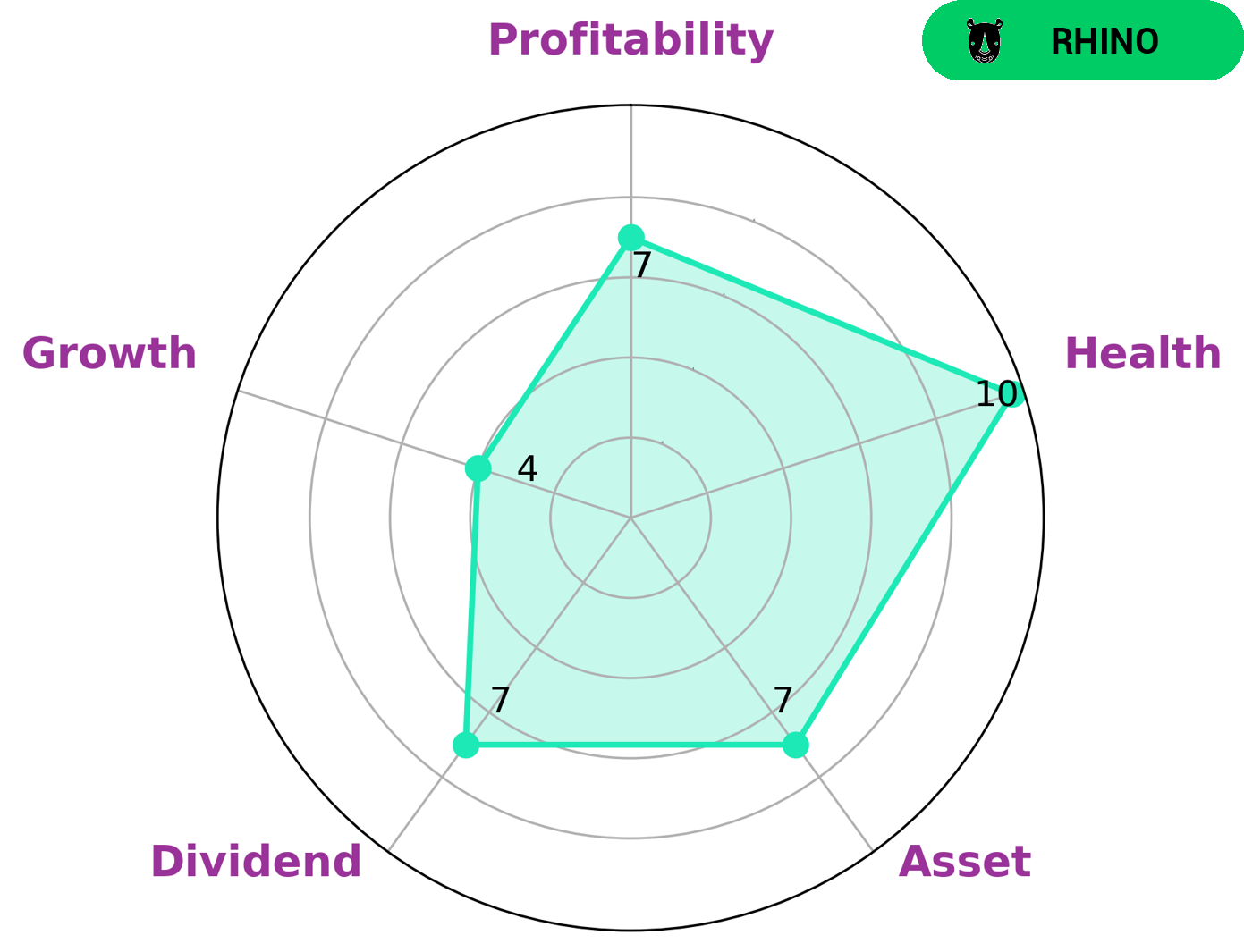

After carefully analyzing WARRIOR MET COAL’s fundamentals, I can confidently say that this company has a strong financial standing. The Star Chart, which assesses a company’s health based on its cashflows and debt, gives WARRIOR MET COAL a perfect score of 10/10. This indicates that the company has a stable cash flow and is capable of paying off its debt while also being able to fund its future operations. In terms of its overall performance, WARRIOR MET COAL excels in several areas. It has a strong asset base, which is reflected in its high health score. Additionally, the company offers a dividend to its shareholders, indicating its profitability and ability to generate returns for investors. Speaking of profitability, WARRIOR MET COAL also has a good track record in this aspect, further solidifying its position as a financially sound company. While WARRIOR MET COAL may not be classified as a high-growth company, it is still considered a ‘rhino’ based on our assessment. This means that the company has achieved moderate revenue and earnings growth, making it a stable and reliable investment option. Based on the above factors, I believe that WARRIOR MET COAL would be appealing to investors who prioritize stability and consistent returns. This may include conservative investors who are looking for low-risk options or income investors who are seeking reliable dividend-paying stocks. Additionally, due to its strong financial standing, WARRIOR MET COAL may also attract value investors who are looking for undervalued stocks with potential for growth. More…

Peers

In the coal industry, Warrior Met Coal Inc faces competition from Tigers Realm Coal Ltd, Mongolian Mining Corp, and Shougang Fushan Resources Group Ltd. These companies are all major players in the industry, and each has its own strengths and weaknesses. Warrior Met Coal Inc must constantly evaluate its competitors in order to stay ahead in the market.

– Tigers Realm Coal Ltd ($ASX:TIG)

Tigers Realm Coal Ltd is a coal company with a market cap of 196M as of 2022. The company has a return on equity of 12.25%. Tigers Realm Coal Ltd is involved in the exploration, development, and production of thermal and coking coal in Russia.

– Mongolian Mining Corp ($SEHK:00975)

Mongolian Mining Corporation is a coal mining and exploration company operating in Mongolia. The company has a market cap of 1.89B as of 2022 and a Return on Equity of -3.82%. Mongolian Mining Corporation is engaged in the business of mining, processing and selling coal products in Mongolia. The company’s principal products are coking coal and thermal coal. Coking coal is used in the production of steel and is a key ingredient in the manufacturing of coke, a fuel used in blast furnaces. Thermal coal is used for power generation.

– Shougang Fushan Resources Group Ltd ($SEHK:00639)

Shougang Fushan Resources Group Ltd is a Chinese state-owned enterprise and one of the largest iron ore producers in the country. The company has a market cap of 11.97B as of 2022 and a return on equity of 21.21%. The company’s main business is the mining, beneficiation, and smelting of iron ore, as well as the production of downstream products such as steel.

Summary

A recent analysis of Warrior Met Coal, Inc. has shown a decrease in the Q2 EPS estimate by an analyst. This could indicate potential challenges or setbacks for the company in the upcoming quarter. As such, investors may want to closely monitor the company’s financial performance and consider adjusting their investment strategies accordingly.

It may also be prudent to assess any external factors, such as market conditions or industry trends, that could impact Warrior Met Coal’s future earnings. Overall, this announcement serves as a reminder of the potential risks and uncertainties involved in investing, and the importance of staying informed and adaptable in the ever-changing market.

Related Posts

Recent Posts

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Investing Everyone Can Do.

Investing shouldn’t be exclusive to a select few. We believe everyone should have the opportunity to grow their wealth. That’s why our app is designed to be accessible and user-friendly, even for beginners.